DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

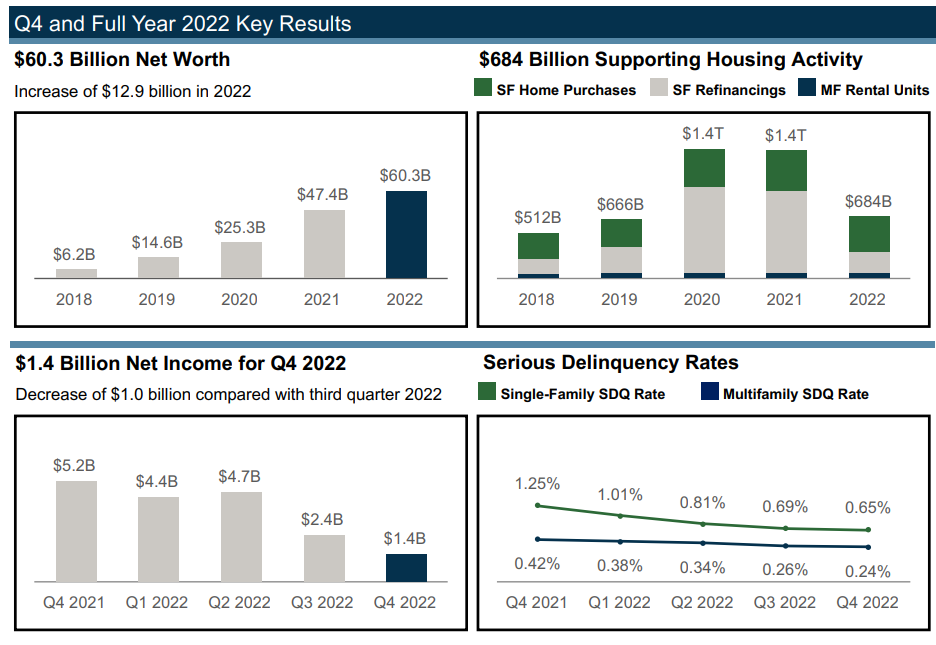

As the housing market took its twists and turns to close our 2022, Fannie Mae felt the impact of a market in flux, as the government-sponsored enterprise (GSE) reported a $12.9 billion annual net income and $1.4 billion Q4 2022 net income, with its net worth reaching $60.3 billion as of December 31, 2022.

As the housing market took its twists and turns to close our 2022, Fannie Mae felt the impact of a market in flux, as the government-sponsored enterprise (GSE) reported a $12.9 billion annual net income and $1.4 billion Q4 2022 net income, with its net worth reaching $60.3 billion as of December 31, 2022.

“Our 2022 results reflect a housing market in transition. We’re proud that Fannie Mae helped approximately 2.6 million households buy, refinance, or rent a home last year, while generating solid earnings and continuing to build our net worth,” said Priscilla Almovodar, Fannie Mae’s CEO.

Almovodar took on the role of Fannie Mae CEO at the beginning of the fourth quarter of 2022, taking over the role from Fannie Mae President David C. Benson, who was serving in the CEO role on an interim basis.

Fannie Mae’s net income decreased $9.3 billion in 2022, compared with 2021, primarily driven by a $11.4 billion shift to provision for credit losses, and a $1.6 billion shift to investment losses, partially offset by a $1.1 billion increase in fair value gains.

In a housing market where home price growth on a national basis decreased from 18.6% in 2021 to 9.2% in 2022; annual home price growth in 2022 reflected home price increases in the first half of 2022, partially offset by home price declines of 1.4% in the second half of 2022. Further exacerbating affordability was the rise in mortgage rates, as the U.S. weekly average 30-year fixed-rate mortgage (FRM) increased from 3.11% at the end of 2021, to 6.42% at the end of 2022.

In 2022, the GSE provided $684 billion in liquidity to the mortgage market in 2022, and acquired approximately 1,151,000 single-family purchase loans, of which more than 45% were for first-time homebuyers, and 886,000 single-family refinance loans.

Approximately 598,000 units of rental housing was financed by Fannie Mae in 2022, a significant majority of which were affordable to households earning at or below 120% of area median income (AMI), providing support for both workforce and affordable housing.

“We expect there will be economic headwinds in 2023 and that housing affordability will continue to remain a challenge for many homebuyers and renters,” said Almodovar. “We also know that Fannie Mae has the capabilities and dedication to help provide liquidity and stability, and to support homebuyers and renters throughout all economic cycles.”

The GSE’s multifamily business segment reported a net income of $2.2 billion and net revenues of $4.8 billion for 2022. In Q4, the segment recognized a $1.1 billion provision for credit losses, approximately $900 million of which related to the company’s seniors housing portfolio. This provision drove a $52 million net loss for the quarter. The company’s seniors housing portfolio has been disproportionately impacted by recent market conditions. As of December 31, 2022, nearly all of the seniors housing loans in the company’s guaranty book of business were current on their payments. However, a sharp rise in short-term interest rates during the latter half of 2022 put additional stress on its seniors housing portfolio that was already experiencing elevated vacancy rates compared to pre-pandemic levels and higher operating costs exacerbated by higher inflation in recent periods. As of December 31, 2022, the seniors housing portfolio had an unpaid principal balance of $16.6 billion, which constituted 4% of the company’s multifamily guaranty book of business. Approximately 40% of the seniors housing loans in the company’s multifamily guaranty book as of December 31, 2022 were adjustable-rate mortgages (ARMs).

The multifamily serious delinquency rate decreased to 0.24% as of December 31, 2022, compared with 0.42% as of December 31, 2021, primarily as a result of loans that received forbearance resolving their delinquency through completion of their repayment plans or otherwise reinstating. Multifamily seriously delinquent loans are loans that are 60 days or more past due.