DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

The latest Loan Monitoring Survey from the Mortgage Bankers Association (MBA) has found that the total number of loans now in forbearance nationwide decreased by six basis points from 0.70% of servicers’ portfolio volume in the prior month, to 0.64% as of January 31, 2023. The MBA estimates that approximately 320,000 homeowners are currently in forbearance plans.

The latest Loan Monitoring Survey from the Mortgage Bankers Association (MBA) has found that the total number of loans now in forbearance nationwide decreased by six basis points from 0.70% of servicers’ portfolio volume in the prior month, to 0.64% as of January 31, 2023. The MBA estimates that approximately 320,000 homeowners are currently in forbearance plans.

By loan type, the share of Fannie Mae and Freddie Mac loans in forbearance decreased slightly from 0.31% to 0.30%. Ginnie Mae loans in forbearance decreased eight basis points from 1.45% to 1.37%, and the forbearance share for portfolio loans and private-label securities (PLS) decreased 17 basis points from 1.00% to 0.83%.

“The forbearance rate decreased across all investor types in January, as borrowers continued to recover from pandemic-related hardships,” said Marina Walsh, CMB, MBA’s VP of Industry Analysis. “With the national emergency set to end on May 11 of this year, many borrowers will no longer have the option to initiate COVID-19-related forbearance. Mortgage forbearance in other forms–whether due to natural disasters or life events–will continue, albeit with different requirements and parameters.”

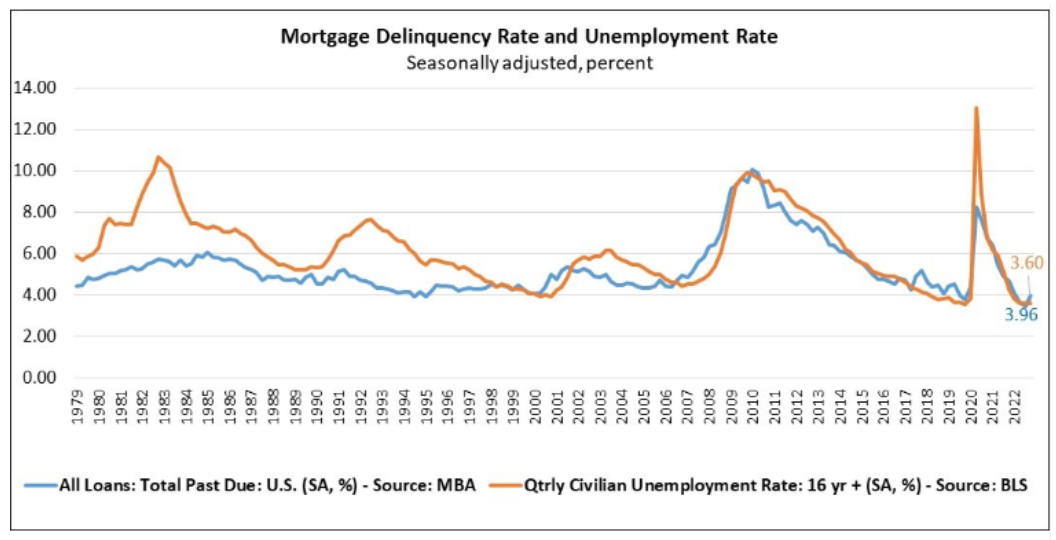

The Bureau of Labor Statistics (BLS) reported that for the month of January 2023, total nonfarm payroll employment rose by 517,000, and the unemployment rate changed little at 3.4%. Job growth was widespread, led by gains in leisure and hospitality, professional and business services, and health care. Employment also increased in government, partially reflecting the return of workers from a strike.

On the jobs front, Douglas G. Duncan, Chief Economist at Fannie Mae, noted, “In the household survey, the unemployment rate continued to trend downward in January, falling to 3.4%, the lowest reading since 1969, and the labor force participation rate ticked up to 62.4%. Average hourly earnings grew by 0.3% in January, and have grown by 4.4% over the last 12 months, a deceleration from prior months but still above pre-pandemic levels, indicating that, while gradually declining, the labor market is still exerting some inflationary pressure. Finally, we note that residential construction employment (including specialty trade contractors) grew by 5,500 in January, though we believe more employment growth will be needed here to help homebuilders fulfill their existing orders.”

By stage, 36.9% of total loans in forbearance were in an initial forbearance plan stage, while 49.9% were in a forbearance extension. The remaining 13.2% were forbearance re-entries, including re-entries with extensions.

Total completed loan workouts from 2020 and onward (repayment plans, loan deferrals/partial claims, loan modifications) that were current as a percent of total completed workouts increased to 76.03% in January from 75.92% the previous month.

Of the cumulative forbearance exits for the period from June 1, 2020, through January 31, 2023, at the time of forbearance exit:

- 29.6% resulted in a loan deferral/partial claim.

- 18.1% represented borrowers who continued to make their monthly payments during their forbearance period.

- 17.5% represented borrowers who did not make all of their monthly payments and exited forbearance without a loss mitigation plan in place yet.

- 16.1% resulted in a loan modification or trial loan modification.

- 10.9% resulted in reinstatements, in which past-due amounts are paid back when exiting forbearance.

- 6.6% resulted in loans paid off through either a refinance or by selling the home.

- The remaining 1.2% resulted in repayment plans, short sales, deed-in-lieus or other reasons.

The five states with the highest share of loans that were current as a percent of servicing portfolio included:

- Washington

- Idaho

- Colorado

- Utah

- California

The five states with the lowest share of loans that were current as a percent of servicing portfolio included:

- Louisiana

- Mississippi

- Indiana

- West Virginia

- New York