DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

The Urban Institute has issued a study, “Credit Health During the COVID-19 Pandemic,” measuring the credit data and health of communities nationwide during the COVID-19 pandemic.

The Urban Institute has issued a study, “Credit Health During the COVID-19 Pandemic,” measuring the credit data and health of communities nationwide during the COVID-19 pandemic.

The study found that while key measures of credit health have improved since February of 2020, many U.S. families and communities still face financial challenges. The Urban Institute examined people’s credit scores, debt delinquencies, and borrowing—culled from credit bureau data in February 2020 and the following months.

“The trends since February indicate that policymakers’ and private-sector partners’ actions to help families weather the financial impacts of the pandemic have made a difference,” said the study. “However, credit indicators in October show that many families still face barriers to financial health. Additional supports are necessary to sustain improvements and help struggling families.”

Those necessary supports mentioned include the Biden Administration’s proposed $1.9 trillion economic rescue package.

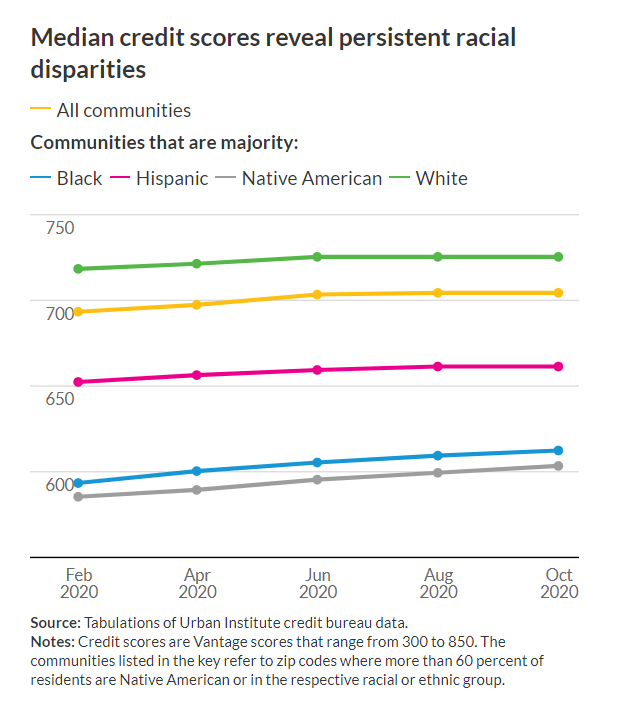

“Credit data cannot capture the experiences of about one in 10 U.S. adults who do not have a credit file, a disproportionate amount of whom are people of color,” said the report. “And although credit health appears to have improved for all groups during the pandemic, racial gaps have not narrowed.

“Credit data cannot capture the experiences of about one in 10 U.S. adults who do not have a credit file, a disproportionate amount of whom are people of color,” said the report. “And although credit health appears to have improved for all groups during the pandemic, racial gaps have not narrowed.

The study found that a majority of Black and Native-American communities have the lowest median credit scores and the highest debt in collection rates, sub-prime credit score rates, and use of high-cost payday and other Alternative Financial Services (AFS) loans. These racial disparities reflect historical inequities that reduced wealth and limited economic choices for communities of color.

The financial toll is high for the 22% of Americans in the credit system who have sub-prime credit, as they often only qualify for the high interest-rate loans, thus debt payments constitute a major share of their income. The Urban Institute cited an example where borrowers with sub-prime credit scores pay nearly $400 more in interest for a $550 emergency loan over three months, and $3,000 more in interest for a $10,000 used-car loan over four years compared with borrowers with prime credit scores.

Click here for more information on the Urban Institute’s study.