DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

A look into the value rent dollars have on the local community by RENTCafé has found that 90 cents of each dollar paid toward rent goes towards taxes, wages, maintenance and improvements, and mortgage payments, while just 10 cents of each dollar belongs to owners and investors.

A look into the value rent dollars have on the local community by RENTCafé has found that 90 cents of each dollar paid toward rent goes towards taxes, wages, maintenance and improvements, and mortgage payments, while just 10 cents of each dollar belongs to owners and investors.

Creative Writer, Editor, and Researcher Florentina Sarac took a look at a Yardi-sponsored initiative, the “COVID-19 Rental Housing Initiative,” a new resource for renters and housing operators backed by four major apartment associations (IREM, NAA, NMHC, NARPM).

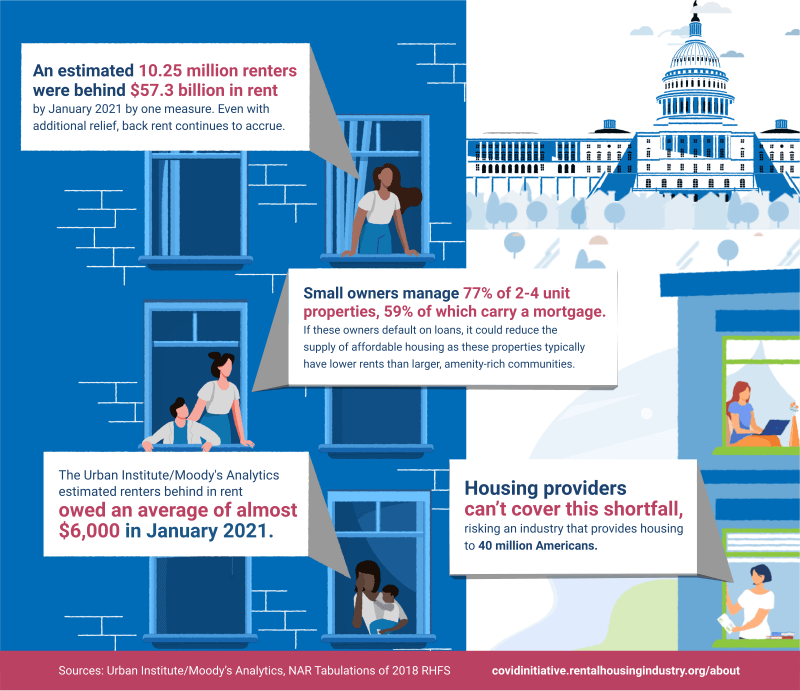

The American Rescue Plan, signed by President Joe Biden on March 11, seeks to relieve renters and housing providers due to the pandemic, offering $21.55 billion in emergency rental assistance, in addition to the $25 billion in aid received in December, bringing the total to approximately $46 billion in assistance total. Renters nationwide are estimated to be approximately $60 billion behind in payments since the outset of the pandemic.

“The largest part of every dollar of rent is used to keep rental housing operational, as 90 cents of it go towards state and local taxes, which support essential services in the community, employee wages, maintenance and improvements, and mortgage payments,” said Sarac. “Just 10 cents go to property owners and investors.”

Rent checks are reinvested in the community in the form of taxes, worker salaries and maintenance for buildings. Mortgage payments comprise the largest percentage of rental dollars, at 38 cents. The majority of small owners depend on this money, according to data from the COVID-19 Rental Housing Initiative, as 59% of them carry a mortgage, and many operate on thin margins.

“Although well-intended, the extended eviction moratoriums expiring at the end of March did nothing to address renters‘ underlying financial distress or the risk of housing insecurity,” said Sarac in the report. “Renters deeply shaken by the COVID-19 pandemic are incurring levels of debt that they may never be able to repay.”

According to data by the Urban Institute and Moody’s Analytics, the average renter behind on their rent owes $6,000 cited the report. With approximately 10.25 million renters in debt as of January 2021, back rent totals have reached an estimated $57.3 billion.

Click here for more of RENTCafé’s breakdown of rental dollars.