Editor's note: This article appears in the April 2021 issue of DS News, available here [1].

With new CFPB leadership ramping up, a roughly even Democrat/Republican Senate, and COVID housing relief policies expiring in June (as of now), mortgage lenders and servicers must be prepared for anything.

They must also be able to act on real-time regulatory changes while maintaining full compliance and seamless customer care for strong and struggling borrowers. Below, we cover hot policy topics and how to navigate it all in real-time.

Latest Biden Forbearance Policy Changes

In late February, the Biden Administration announced several updates to CARES forbearance and foreclosure programs for struggling borrowers as the pandemic slows economic recovery, including:

- An additional six months of forbearance now available in two three-month increments through June 30

- Foreclosure moratorium extended through June 30

- New forbearance requests allowed through June 30

After previously extending the ban on foreclosures for homeowners with federally backed mortgages to March 31, President Biden further extended the foreclosure moratorium and expanded forbearance access. This gives homeowners more time to recover as vaccine distribution speeds up and a tiny pinprick of light at the end of the COVID tunnel becomes visible.

Policy Implications and Expectations for 2021

These updates out of the Biden Administration are nothing surprising; they are more intended to buy time than anything.

The most interesting observation to be had from this policy update is that the Biden Administration has essentially said, “We’ve got this. Struggling homeowners need help, and we don’t need Congress to get that done.”

Whether people realize it or not, it seems the Biden administration has thrown in the towel when it comes to relying on Congress to pass meaningful legislation regarding servicing requirements or new borrower protections.

We are in a post-CARES Act world where CARES set the foundation for forbearance, and now it’s up to agencies and investors to carry homeowners through the turmoil.

As for what to expect in the coming months, there have been rumblings about an extension of the foreclosure moratorium until September 30, and some expect forbearance extensions to ultimately span a 24-month period in total.

The foremost driver of the policy roadmap is, unsurprisingly, the enduring need for economic relief as the pace of vaccination distribution pushes the return to normalcy to mid to late 2021.

Other policy drivers to keep in mind:

- Slowly improving unemployment rate (6% unemployment rate in April, down from 6.7% in December)

- COVID relief bill passed in early March, which included a third round of stimulus checks for many Americans

- K-shaped recovery impacting sectors of market differently

- Tax reform on table, influenced by Senate moderates

A Shifting Regulatory Climate

On the regulatory front, the Biden Administration’s philosophy is that "personnel is policy," and Biden’s early appointees at the CFPB/HUD/OCC will be key to guiding their policy agendas.

A Democratic majority in the Senate emboldened the new administration to pursue more aggressive nominations, including the Warren-approved Rohit Chopra as CFPB Director.

However, with such a narrow majority margin, the Biden Administration will have to cater to a more moderate agenda if the goal is to pass meaningful legislation through Congress.

Lenders have been bracing for a more rigorous era of CFPB enforcement, and that may indeed be on the horizon. The CFPB is in the midst of a hiring spree, and a Chopra-headed CFPB is anticipated to ramp up requests for funding and show a strengthened capacity for fair lending enforcement, process development for initiating investigations, and collaboration with state mini-CFPBs.

On February 23, the CFPB announced that it expects to propose a rule to delay the compliance date for the new Qualified Mortgage (QM) rule to July 1, 2021 to allow lenders more time to make QM loans based on their DTI ratio or Fannie/Freddie eligibility.

The CFPB has also dropped hints that they may revisit the Seasoned QM Final Rule and, at a later date, consider whether to begin further rulemaking to reconsider other elements of the General QM Rule.

Other regulatory influences to keep in mind:

- FDCPA rule finalized in November

- Reg X/loss mitigation rule updates expected in Spring

- HUD expected to focus on affordable housing initiatives and enforcement activity around CARES Act forbearance and servicing

- OCC/Fed/FDIC emphasis on the Community Reinvestment Act

Forbearance Volume Stays Steady as Servicers Prep for Loss Mit Wave

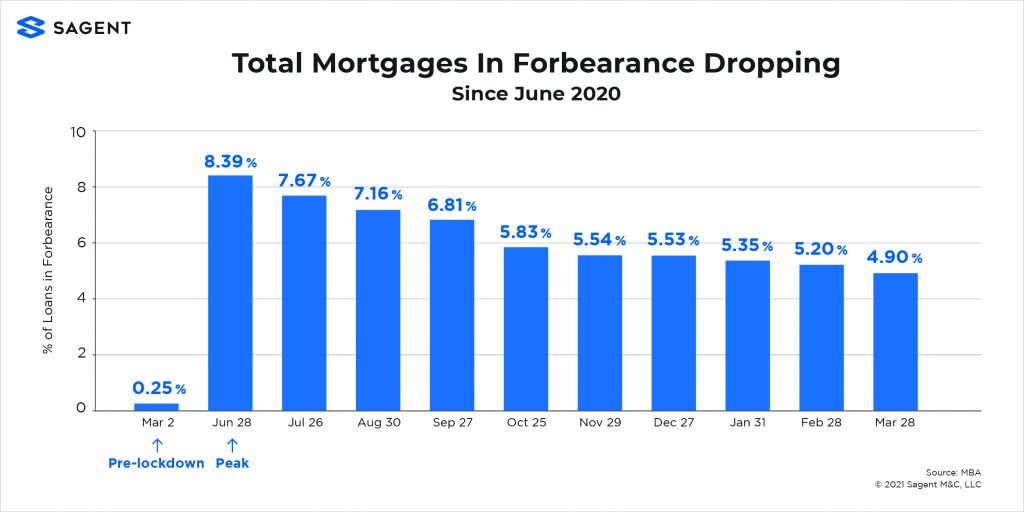

On the forbearance front, MBA forbearance volume data through March 28 shows reason for cautious optimism; forbearance volume is slowly trending downwards, with the total share of mortgages in forbearance declining each month since its peak in June 2020 (see Figure 1).

Unfortunately, forbearance numbers are mostly consistent since October, still sitting at 2.5 million total borrowers in forbearance.

Figure 1: Total Forbearance Volume

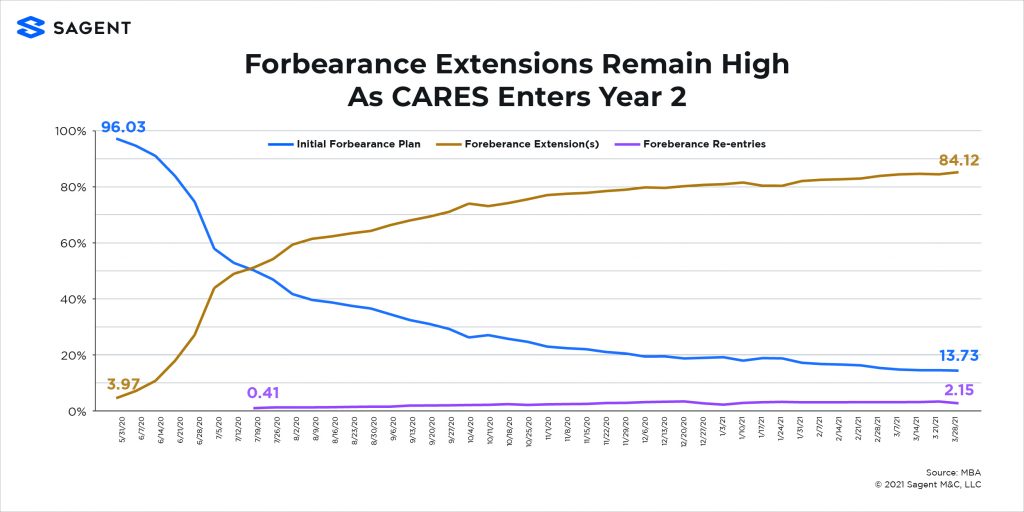

While total forbearances may be declining slightly, it is worth noting that 84.1% of borrowers in forbearance have extended their forbearances (see Figure 2), while forbearance exits have slowed to a crawl.

Figure 2: Forbearance Extensions

The good news (for servicers and borrowers) is this: we’re not hurtling towards a foreclosure crisis a la 2008.

According to the Urban Institute, borrowers this time around have a much stronger home equity buffer against foreclosure thanks to home price appreciation. Borrowers with government-secured mortgages have an average 22% equity buffer (with only 3.6% of borrowers having negative equity).

Traditionally, 20% equity is the turning point where borrowers are considered to have a strong enough financial incentive not to abandon mortgage repayment efforts.

But as forbearance volume remains steady, servicers need to shore up their loss mitigation waterfall to prepare for the wave when tides turn and forbearances finally expire for good.

Servicers need to be asking themselves, “How can I make sure our servicing system is up to date with the latest policy updates? How can we make sure we’re compliant with new policies, and how do we communicate those policy shifts to our customers? How can we ensure our loss mitigation waterfall is accurate?”

For many borrowers, the latest forbearance and foreclosure extensions from the Biden Administration have extended their runway into loss mitigation. However, policy relief can only last so long, and servicers need to be arming themselves with powerful default management technology now to scale their loss mit capabilities before things start to escalate.

Servicer Takeaways

If 2020 was characterized by a series of unfortunate events, may 2021 be characterized by our painstakingly slow, steady recovery from those events.

While things are getting better and agencies are stepping in to help, servicers still face a slew of challenges.

Here are three key takeaways for servicers as we head into Q2:

1. Brace for a New Wave of Borrower Requests

The forbearance and foreclosure extensions we saw in mid-February mean that servicers have to prepare for another wave of borrowers reaching out because they need fast forbearance extensions.

By now, this should be old hat, as servicers have been scaling their support teams throughout COVID to handle upticks in borrower queries.

2. Renewed Efforts for Borrower Educations and Outreach

We keep hearing about this ongoing problem of borrowers whose forbearances are close to expiring (or have already expired) who do not know that they have to explicitly request extensions from their servicers. This has resulted in hundreds of thousands of borrowers who are needlessly delinquent who are ignoring outreach from their servicers.

This will continue to be an issue, as there will be borrowers out there who don’t understand that they must reach out to request these two new periods of three-month forbearance extensions on top of the initial 12 months offered through the CARES Act.

Proactive borrower outreach and education campaigns will be necessary to help borrowers who are flirting with delinquency understand that they can access additional hardship support.

It’s on servicers to ensure they are adequately conveying policy updates to homeowners with expedience, distilling down the complex policies and shifting deadlines into simplified, easily digestible updates for homeowners.

3. Ensure Your Tech Stack Can Handle It All

Servicers are faced with a Herculean task: provide real-time hardship care while complying with complex rule changes.

Fannie Mae’s recent Mortgage Lender Sentiment Survey found that 45% of servicers say keeping up with policy changes from investors was their biggest or second-biggest COVID challenge.

Good servicing technology can (and should) reduce that friction.

In a tumultuous servicing climate, it will be the servicers with powerful servicing technology who will emerge from COVID with stable, happy borrowers and a competitive edge in the market.

The seamless interplay between loan servicing, default management, and customer care platforms exemplifies how servicers can adapt to each CARES rollout with modern borrower self-service and real-time configuration (rather than coding) to comply with real-time policy changes.