DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

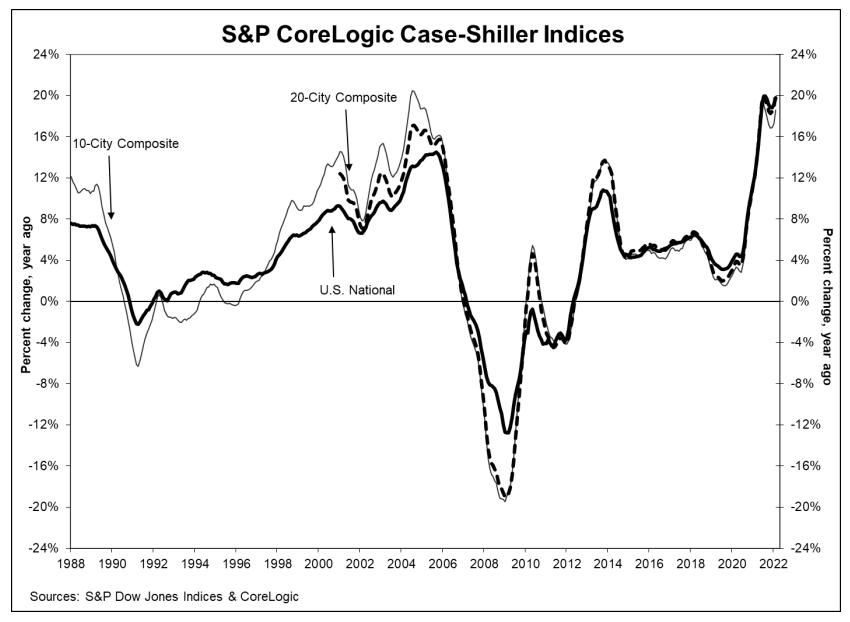

According to the latest S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, home prices continue to increase across the U.S., with a 19.8% annual gain in February 2022, up from January’s total of 19.1%.

According to the latest S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, home prices continue to increase across the U.S., with a 19.8% annual gain in February 2022, up from January’s total of 19.1%.

The study, which covers all nine U.S. census divisions, found its 10-City Composite annual increase coming in at 18.6%, up from 17.3% the previous month. The 20-City Composite posted a 20.2% year-over-year gain, up from 18.9% in the previous month.

"The National Composite's 19.8% year-over-year change for February was the third-highest reading in 35 years of history,” said Craig J. Lazzara, Managing Director at S&P DJI. “That level of price growth suggests broad strength in the housing market, which is exactly what we continue to observe. All 20 cities saw double-digit price increases for the 12 months ended in February, and price growth in all 20 cities accelerated relative to January's report. February's price increase ranked in the top quartile of historical experience for every city, and in the top decile for 18 of them.”

Nationwide, Phoenix, Tampa, and Miami reported the highest year-over-year gains among the 20 cities in February, with Phoenix leading the way with a 32.9% year-over-year price increase, followed by Tampa with a 32.6% increase, and Miami with a 29.7% increase. All 20 cities reported higher price increases in the year ending February 2022 versus the year ending January 2022.

“Price growth was robust across the country with all 20 metro areas experiencing stronger annual gains than in January,” said CoreLogic Deputy Chief Economist Selma Hepp. “The largest increases in annual gains were in the West Coast markets: Los Angeles, Seattle, San Diego and San Francisco, and also in high tier price segments.”

Lazzara added, “Prices were strongest in the South (+28.1%) and Southeast (+27.9%), but every region continued to show impressive gains.”

Before seasonal adjustment, S&P CoreLogic Case-Shiller’s U.S. National Index posted a 1.7% month-over-month increase in February, while the 10-City and 20-City Composites both posted increases of 2.4%. After seasonal adjustment, the U.S. National Index posted a month-over-month increase of 1.9%, and the 10-City and 20-City Composites both posted increases of 2.3% and 2.4%, respectively.

“Real estate markets experienced a rush of changes over the past two months, stemming from a strong labor market driving wages and inflation higher, tight inventory, supply-chain disruptions from the war in Ukraine, and interest rates rising to 11-year highs,” said George Ratiu, Manager of Economic Research for Realtor.com. “For buyers, the jumps in prices and mortgage rates translated into sticker shock. For a median-priced home financed with a 30-year loan, the monthly payment is $550 higher than a year ago, a 46% jump which dwarfs the 15% increase in housing prices, and 8.5% advance in consumer prices.”

Anticipated sticker shock was only driven higher as last week, Freddie Mac reported the 30-year fixed-rate mortgage (FRM) crossing the 5% mark, hitting 5.11%, and rising for the seventh consecutive week.

However, some buyers are simply bowing out of the market altogether due to affordability issues. And while some return to the sidelines, many sellers have been forced to reduce their asking prices.

According to a new report from Redfin, homebuyer demand has eased up over the last several weeks, due to inflationary concerns, surging mortgage rates and housing costs, as an estimated one in eight sellers cut their list prices during the four weeks ending April 17—the highest share in five months.

“For sellers, rising prices offer a welcome environment for cashing out equity,” noted Ratiu. “However, since most sellers are also buyers, they are facing a similar conundrum, as their next homes also carry higher price tags and interest rates. As we move through the spring housing market, we are seeing clear signs of cooling demand. Many buyers are deciding to take a step back and re-evaluate their budgets and timelines. The silver lining to the moderation in transactions is that markets seem to be stepping back from the overheated environment of the past year.”

Lazzara added, “The macroeconomic environment is evolving rapidly and may not support extraordinary home price growth for much longer. The post-COVID resumption of general economic activity has stoked inflation, and the Federal Reserve has begun to increase interest rates in response. We may soon begin to see the impact of increasing mortgage rates on home prices."