The Consumer Financial Protection Bureau (CFPB) [1] has issued two reports showing that more work needs to be done to help mortgage borrowers coping with the COVID-19 pandemic and economic downturn. The first report, “Characteristics of Mortgage Borrowers During the COVID-19 Pandemic [2],” documents that Black and Hispanic mortgage borrowers are much more likely to be delinquent or in a forbearance program than white borrowers. In a second report [3], the CFPB reports that overall mortgage complaints to the CFPB have risen to their highest level in three years.

The Consumer Financial Protection Bureau (CFPB) [1] has issued two reports showing that more work needs to be done to help mortgage borrowers coping with the COVID-19 pandemic and economic downturn. The first report, “Characteristics of Mortgage Borrowers During the COVID-19 Pandemic [2],” documents that Black and Hispanic mortgage borrowers are much more likely to be delinquent or in a forbearance program than white borrowers. In a second report [3], the CFPB reports that overall mortgage complaints to the CFPB have risen to their highest level in three years.

“More borrowers are behind on their mortgage than at any time since the height of the Great Recession,” said CFPB Acting Director Dave Uejio [4]. “Communities of color have been hit hard by the pandemic, and the latest data show that many borrowers are still hurting. The CFPB will continue to seek and actively respond to developments in the market, doing everything in our power to help families stay in their homes. As we warned mortgage servicers last month, unprepared is unacceptable.”

Throughout the pandemic, the CFPB has worked hand-in-hand with American consumers to protect them from foreclosure and eviction as the nation deals with economic uncertainty.

The CFPB recently issued an interim final rule [5] in support of the Centers for Disease Control and Prevention (CDC)’s eviction moratorium, requiring debt collectors to provide written notice to tenants of their rights under the eviction moratorium, and prohibiting debt collectors from misrepresenting tenants’ eligibility for protection from eviction under the moratorium.

In order to prevent the windfall of foreclosures that may overwhelm servicers, the CFPB also proposed a number of actions [6] through its proposal, “Protections for Borrowers Affected by the COVID-19 Emergency Under the Real Estate Settlement Procedures Act (RESPA), Regulation X [7],” as the emergency federal foreclosure protections are eventually set to expire.

The CFPB is seeking comments on a proposal [8] intended to help prevent avoidable foreclosures for borrowers affected by COVID-19. That proposal, if finalized, would temporarily require servicers to enhance communications with borrowers who are delinquent or in forbearance, allow servicers to offer certain streamlined loan modification options to borrowers with COVID-19-related hardships, and require servicers to afford all borrowers a special pre-foreclosure review period. The comment period closes May 10.

The CFPB’s research brief, “Characteristics of Mortgage Borrowers During the COVID-19 Pandemic [2],” prepared by the CFPB’s Section Chief, Consumer and Household Research and Policy Erik Durbin; Research Assistant Greta Li; and Economists David Low and Judith Ricks, shows that some homeowners and communities are more at risk than others.

- Borrowers in forbearance or delinquent are disproportionately Black and Hispanic. For example, 33% of borrowers in forbearance (and 27% of delinquent borrowers) are Black or Hispanic, while only 18% of the total population of mortgage borrowers are Black or Hispanic.

- Loans in forbearance or that are delinquent are disproportionately likely to have high loan-to-value (LTV) and limited equity, leaving them vulnerable to being underwater. For example, half of all loans in forbearance have an LTV greater than 60%, compared to only 34% of current loans.

- Forbearance and delinquency are significantly more common in communities of color (defined as majority minority census tracts) and lower-income communities (defined by census tract income quartiles).

“Borrower experiences differed substantially by race,” said the study [9]. “Roughly 3.7% of White borrowers were in forbearance and 0.5% were delinquent. Black and Hispanic borrowers were much more likely to experience either of these outcomes. Black borrowers were 2.5 times more likely to end up in forbearance (9.2%) and two times more likely to end up delinquent (1.0%) compared to White borrowers. Similarly, Hispanics were 2.3 times more likely to end up in forbearance (8.4%), and about 1.5 times more likely to end up delinquent (0.7%). Other-race borrowers were also more likely to experience forbearance compared to Whites, but were less likely to end up delinquent.”

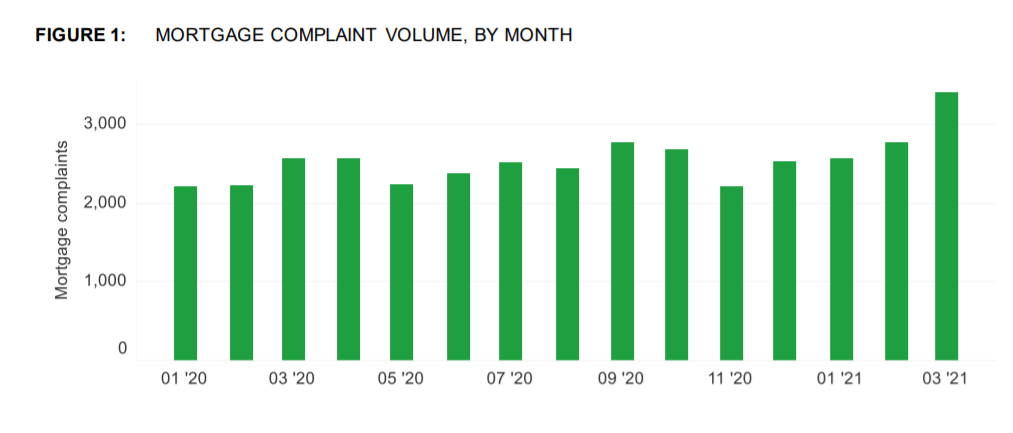

Also issued today by the CFPB was the Consumer Complaint Bulletin on Mortgage Forbearance. In March 2021, consumers submitted more mortgage complaints to the CFPB than in any month since April 2018. Mortgage complaints mentioning forbearance or related terms have also reached their highest monthly average since March and April of 2020, and the number of borrowers who report they are struggling to make their payments is also trending upward.

When submitting mortgage complaints, consumers identified from a list the issue that best described the problem they experienced. For mortgage complaints, issue options included applying for a mortgage or refinancing an existing mortgage; closing on a mortgage; problem with a credit or consumer report; struggling to pay mortgage; and trouble during the payment process. The most common issue reported since January 2020 has been trouble during the payment process.

Additional complaints included:

- Servicer communications: Many consumers complained that servicers did not provide clear and accurate information about their options. In particular, consumers reported that servicers were not providing information about loss mitigation until after the consumer’s forbearance had ended, and that the information provided about post-forbearance options was confusing and incomplete.

- Delays and denials of loan modifications: Consumers reported long delays in having their loan modified so that they could resume payments on the mortgage. In some cases, these delays were due to demands for additional documents by servicers. In other cases, consumers said servicers provided conflicting information about what options were available and the consumer’s eligibility for loan modification.