The mortgage delinquency rate is improving at an unprecedented rate, researchers say. That's thanks in large part to a gradually recovering labor market.

The mortgage delinquency rate is improving at an unprecedented rate, researchers say. That's thanks in large part to a gradually recovering labor market.

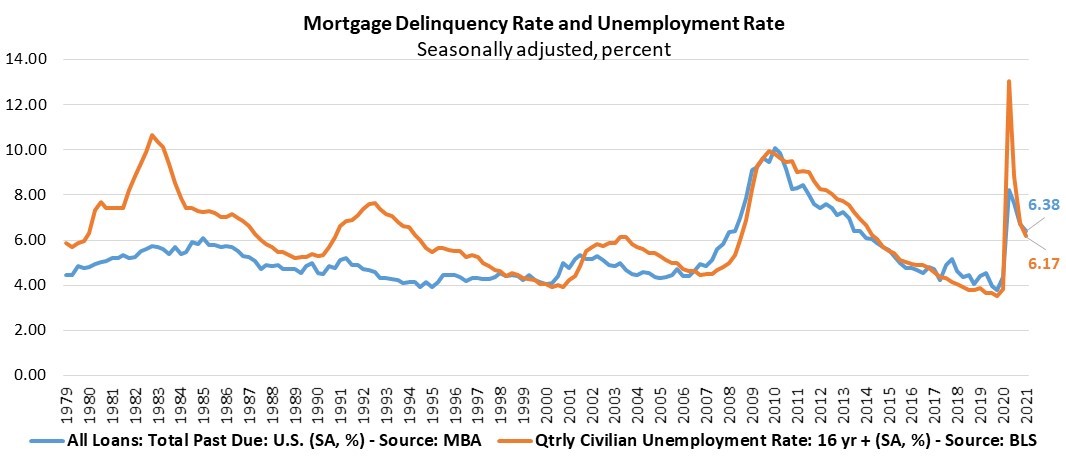

According to the Mortgage Bankers Association (MBA) Q1 report, the delinquency rate for mortgage loans on one-to-four-unit residential properties decreased to a seasonally adjusted rate of 6.38% of all loans outstanding at the end of the first quarter. The MBA includes loans in forbearance if the payment was not made based on the original terms of the mortgage. The research shows the delinquency rate dropped 35 basis points from the fourth quarter of 2020. Experts at the MBA say there has never been such a substantial decline in the delinquency rate over such a short period of time.

Marina Walsh, MBA’s VP of Industry Analysis attributes the rapid improvement to an increasingly positive employment outlook and government stimulus programs.

"Mortgage delinquency rates continued to decrease in the first quarter of 2021, as a rebounding job market and stimulus checks helped borrowers stay current on their mortgage payments," Walsh said. “Mortgage delinquencies track closely to the U.S. unemployment rate, and with unemployment dropping from last year’s spike, many households appear to be doing better."

In April’s employment statistics report, jobs gains came in at 266,000. The U.S. has now regained approximately 63% of the jobs lost at the start of the pandemic. It's still "far below consensus expectations," says First American Economist Odeta Kushi, but homeowners seem to be suffering slightly less, fiscally.

“As of the first quarter of 2021, low-earning job losses were down 7.8% year over year, while high-earning job losses were down 1.9%. This is one reason why housing has been resilient – this service sector-driven recession has disproportionally hurt younger, lower-wage workers who are less likely to be homeowners or homebuyers,” Kushi said.

That said, the mortgage delinquency rate, which peaked at 8.22% in the second quarter of 2020, has dropped by 184 basis points to 6.38% within three quarters. In addition, this quarter’s earliest stage delinquencies— the 30-day and 60-day delinquencies combined—dropped to the lowest levels since the inception of the survey in 1979, Walsh said.

"Notwithstanding the welcome improvement in mortgage delinquencies and the positive job outlook, the delinquency rate this past quarter still remains 105 basis points higher than its historical quarterly average of 5.33 percent," Walsh said. "We continue to see seriously delinquent loans—those loans that are over 90 days past due or in the process of foreclosure—at elevated levels, particularly for FHA and VA borrowers."

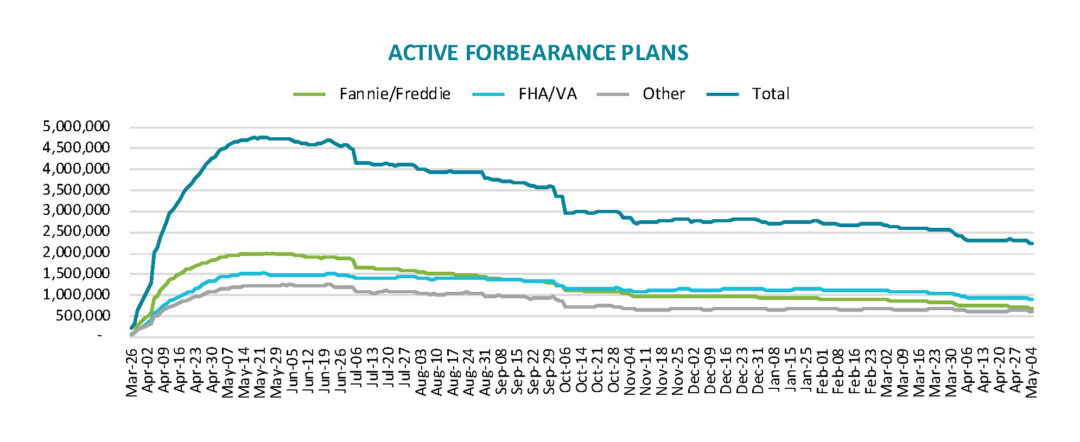

Echoing the MBA's findings, the research team at Black Knight [1] reported a strong improvement to COVID-related forbearance activity with Tuesday-to-Tuesday (May 4) volumes dipping by 105,000 or 4.5%.

As of May 4, just over 2.2 million or 4.2% of homeowners remain in COVID-19 related forbearance plans, including 2.5% of Fannie Mae and Freddie Mac-backed loans, 7.4% of Federal Housing Administration or VA-backed loans, and 4.8% of portfolio or private loans.

Black Knight's analysts report that 350,000 forbearance plans are set to be reviewed for extension or removal in May—that number climbs to nearly 900,000 in June, the final quarterly review before early forbearance entrants begin to reach their 18-month plan expirations later this year.

Walsh concluded that "upon exiting long-term forbearance, some borrowers, regardless of their improving employment prospects, may need more complex workout options, such as loan modifications, to remain in their homes."

The full MBA National Delinquency Report is available at MBA.org. [2]

Black Knight's weekly forbearance reports are available on Black Knight's blog [3].

And find Odeta Kushi's regular commentary on First American's Economic Center blog. [4]