DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Forbearance levels are looking better across the board as volume decreases for all types of mortgage loans, according to the weekly report from Black Knight. Keeping with the strong trend of early-month improvements, overall volumes dropped by 61,000 or 2.7%.

Forbearance levels are looking better across the board as volume decreases for all types of mortgage loans, according to the weekly report from Black Knight. Keeping with the strong trend of early-month improvements, overall volumes dropped by 61,000 or 2.7%.

Forbearance volumes for Fannie Mae and Freddie Mac fell by 13,000, or -1.9%.

Federal Housing Administration (FHA) and VA plan volumes improved by 19,000, or -2.1%.

Private Label Securities (PLS) and portfolio loan forbearances decreased by 29,000 or 4.6%.

Inflow is down too—"total plan starts are down 13% month-over-month, and continue to slowly decline," report the analysts at Black Knight.

So, the current state of COVID-related forbearance plans in America as of May 11 looks like this:

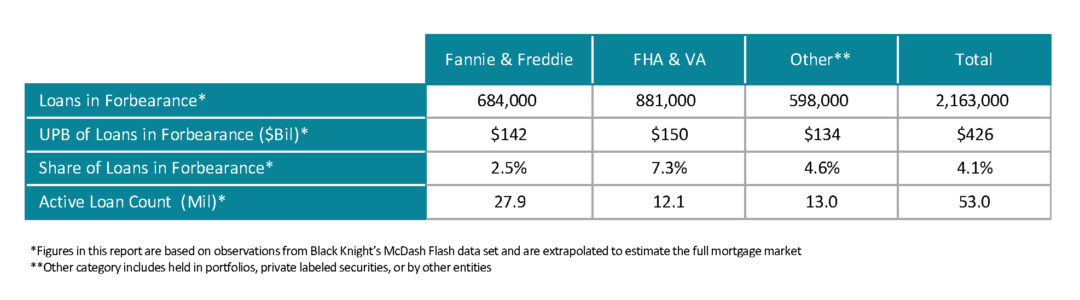

2.16 million or 4.1% of homeowners remain in pandemic-prompted forbearance plans, including 2.5% of Fannie/Freddie loans, 7.3% of FHA/VA loans, and 4.6% of portfolio and PLS loans.

Some 250,000 plans list May 2021 expiration dates, Black Knight says, which offers "a moderate opportunity for additional improvements over the next few weeks, and more acutely in June, which lists 860,000 removal-or-extension expirations. Of all loans reviewed for extension or removal over the past month, 38% have been removed from forbearance, which marks the highest removal rate since mid-February.

June marks the final quarterly review before early forbearance entrants begin to reach their 18-month plan expirations later this year.

President Joe Biden last February announced an extension of the moratorium on home foreclosures—previously set to expire March 31—through the end of June. That temporary moratorium blocks home foreclosures, allows delayed mortgage payments, and offers six months of additional mortgage forbearance for those who enroll by June 30.

Last week, when discussing the rapidly improving rate of delinquencies and forbearances, Marina Walsh, the Mortgage Bankers Association VP of Industry Analysis credited an improving jobs situation. She also issued a warning to servicers as forbearance programs expire: "Upon exiting long-term forbearance, some borrowers, regardless of their improving employment prospects, may need more complex workout options, such as loan modifications, to remain in their homes."