DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

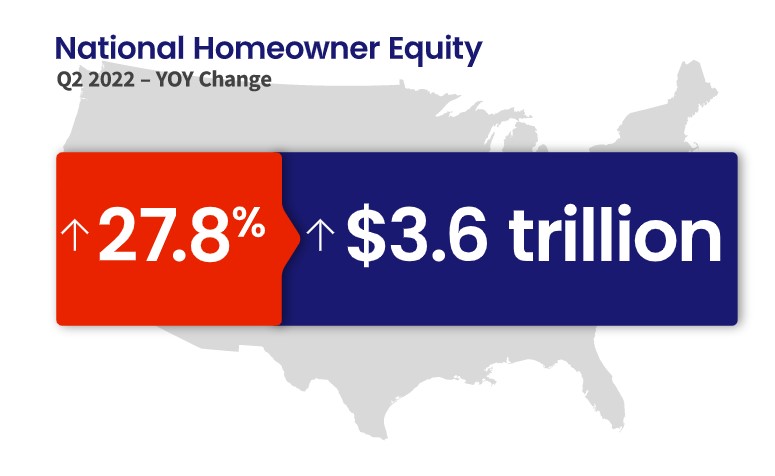

Home equity hit a new high in the second quarter according to CoreLogic, as homeowners with mortgages gained a collective $3.6 billion year-over-year over the course of a single quarter.

Home equity hit a new high in the second quarter according to CoreLogic, as homeowners with mortgages gained a collective $3.6 billion year-over-year over the course of a single quarter.

According to CoreLogic’s Homeowner Equity Report, homeowners with mortgages (which is about 63% of all properties) saw equity increase by 27.8% year-over-year, roughly representing $60,200, since the second quarter of 2021.

While home price growth slowed on an annual basis in the second quarter, it has still risen every month for the last 125 months, leading to homeowners continuing to gain near-record equity from the second quarter of 2021.

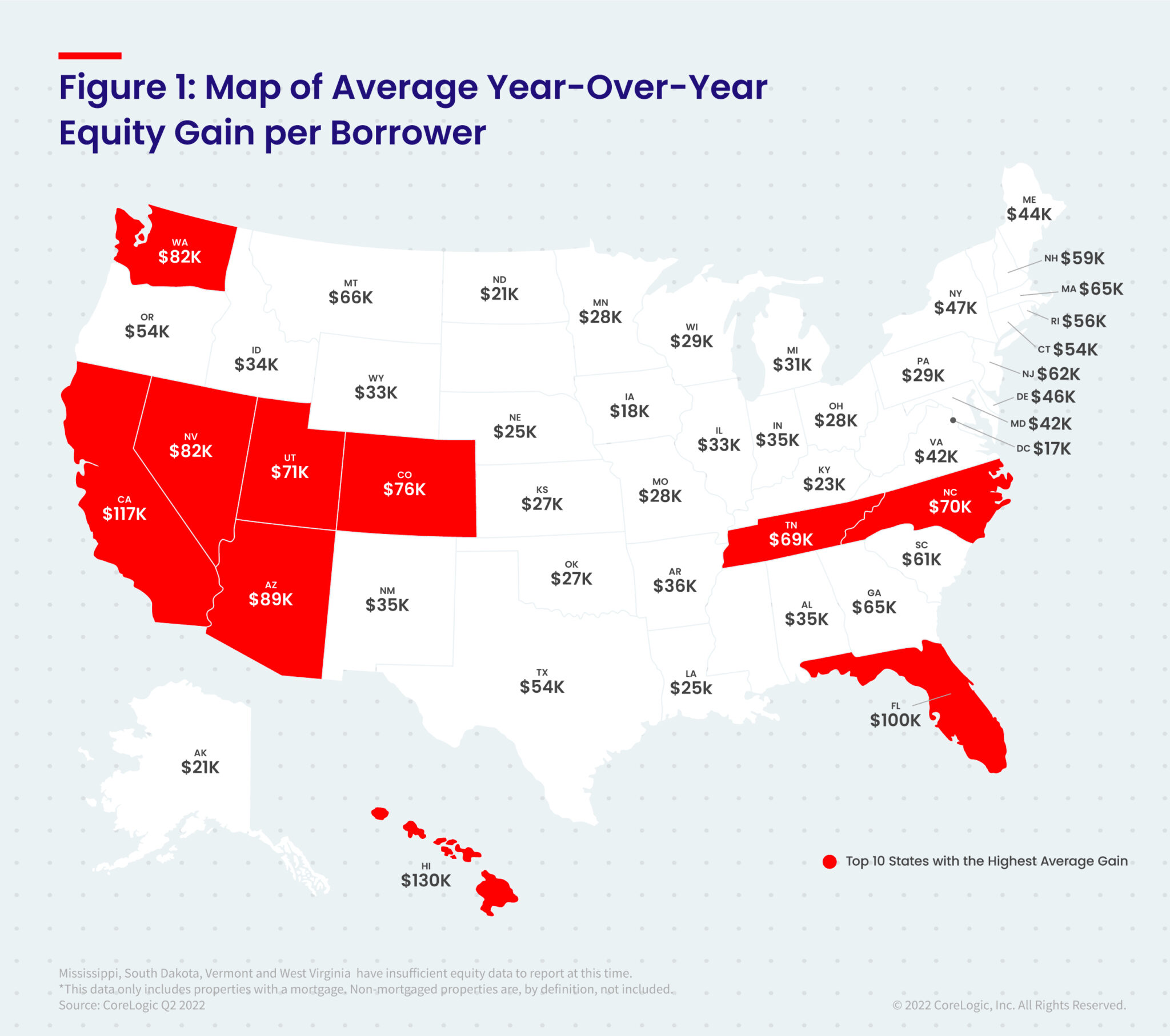

The total average equity per borrower has now reached almost $300,000, the highest in the data series. Home price growth and the refinance boom of the last two years have helped bring down the national average loan-to-value ratio to 42%, the lowest in the data series since 2010.

“For many households, home equity is the only source of wealth creation,” said Selma Hepp, Interim Lead of the Office of the Chief Economist for CoreLogic. “As a result, recent record gains in equity and record declines in loan-to-value ratios will provide many owners with a financial buffer in case economic conditions worsen. In addition, record equity continues to provide fuel for housing demand, particularly if households are relocating to more affordable areas.”

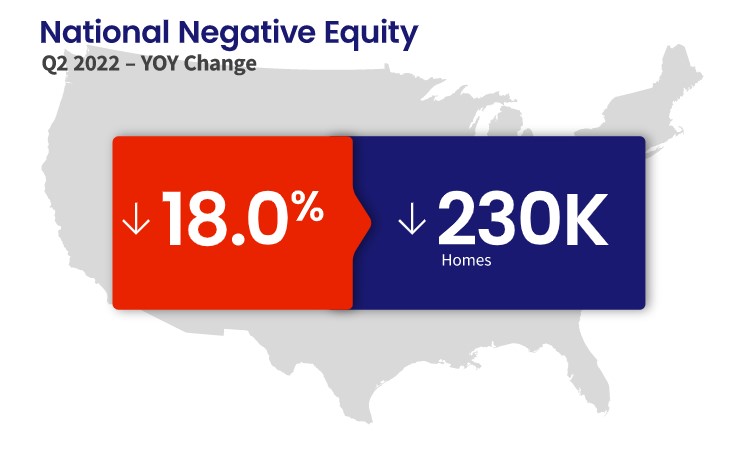

Negative equity, also referred to as underwater or upside-down mortgages, applies to borrowers who owe more on their mortgages than their homes are currently worth. As of the second quarter of 2022, the quarterly and annual changes in negative equity were:

- Quarterly change: From the first quarter of 2022 to the second quarter of 2022, the total number of mortgaged homes in negative equity decreased by 7% to 1 million homes, or 1.8% of all mortgaged properties.

- Annual change: In the second quarter of 2021, 1.3 million homes, or 2.3% of all mortgaged properties, were in negative equity. This number declined by 18% in the second quarter of 2022.

“Because home equity is affected by home price changes, borrowers with equity positions near (+/- 5%) the negative equity cutoff are most likely to move out of or into negative equity as prices change, respectively,” the report concluded. “Looking at the second quarter of 2022 book of mortgages, if home prices increase by 5%, 116,000 homes would regain equity; if home prices decline by 5%, 148,000 properties would fall underwater.”

Click here to view the report in its entirety.