DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

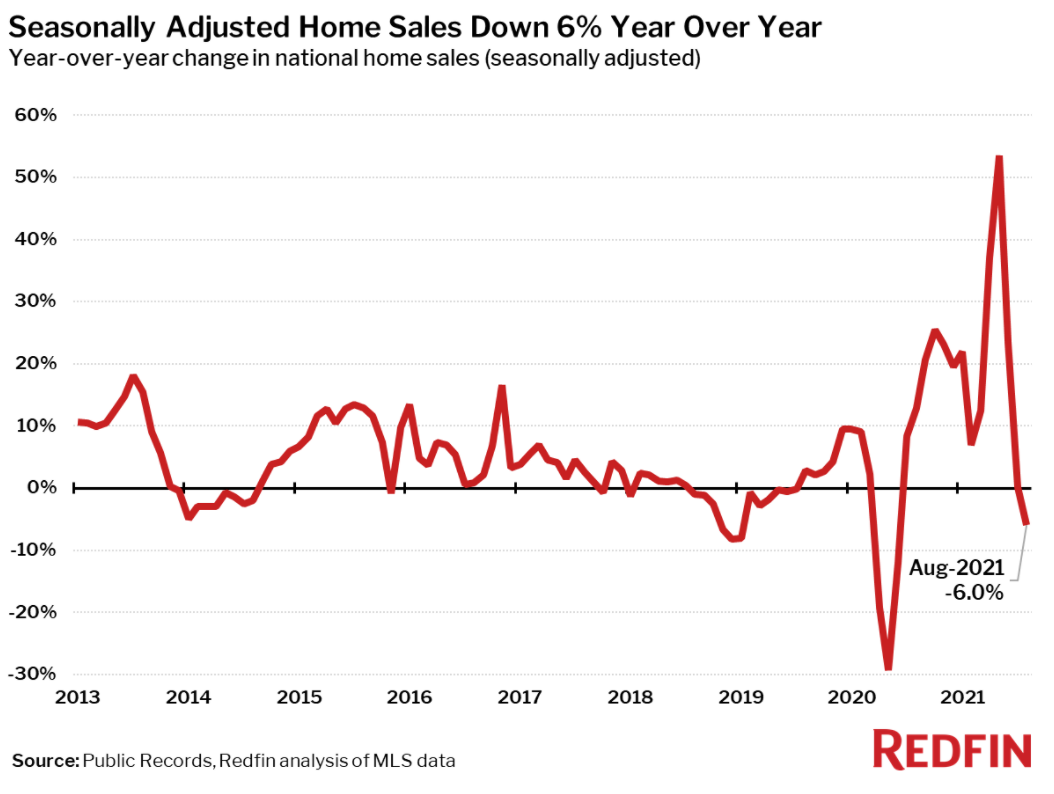

Seasonally adjusted homes sales in August dropped 6% year-over-year, the first drop in 15 months, according to a new study from Redfin. The study notes that this could be an early signal of a tightening housing market.

Seasonally adjusted homes sales in August dropped 6% year-over-year, the first drop in 15 months, according to a new study from Redfin. The study notes that this could be an early signal of a tightening housing market.

The study, authored by Redfin Analyst Tim Ellis, also found that the median home sale price has risen 16.2% to $380,300 year-over-year, while the number of units available for sale have fallen by 19.1% during that same period.

"When it comes to home prices in this market, what goes up stays up," said Redfin Chief Economist Daryl Fairweather. "That's especially true in the Sun Belt; home prices are up more than 20% from last year in Austin and Phoenix. Even with these steep increases, homes in these areas are still relatively affordable, so these and other hot migration destinations are going to continue to attract homebuyers from the coasts. As workers change jobs en masse and enhanced unemployment benefits come to an end, we could see even more households relocate for affordability in the coming months."

The areas reporting the largest declines were New Orleans, Louisiana (a 23% decline since last year); Salt Lake City, Utah (16%); and Warren, Michigan (14%). Some markets did see an increase of home sales, as sales in New York, New York increased by 65% year-over-year; Honolulu, Hawaii saw a 47% rise; and Nassau County, Long Island, New York experienced a 32% rise.

Other key findings in the report include:

- A typical home in August was on the market for 16 days—half as much as a year earlier—when a home sold in 31 days, but up by one day from the record low in June.

- 52% of homes sold above list price, down from June, but up 20 percentage points year-over-year.

- The most competitive market in August was Oakland, California, where 82.3% of homes sold above list price; followed by 78.3% in San Jose, California; 74.8% in Rochester, New York; 71.7% in San Francisco, California; and 71.0% in Worcester, Massachusetts.

- Austin, Texas had the nation’s highest price growth, rising 35.7% since last year to $475,000. Phoenix, Arizona had the second highest growth at 25.2% year-over-year price growth; followed by Salt Lake City, Utah (24.3%); Tucson, Arizona (23.5%); and North Port, Florida (21.5%).