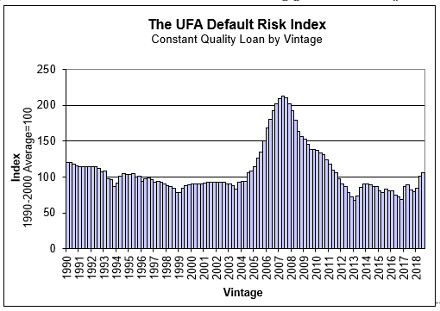

Default risk is up in Q3, according to the latest Default Risk Index from University Financial Associates (UFA) [1]. According to the Q3 2018 Index, default risk rose by five points to an index score of 106. UFA notes that one of their key findings that defaults on loans currently being originated should be expected to be six percent higher than the average of similar loans originated in the 1990s, due solely to the local and national economic environment.

Default risk is up in Q3, according to the latest Default Risk Index from University Financial Associates (UFA) [1]. According to the Q3 2018 Index, default risk rose by five points to an index score of 106. UFA notes that one of their key findings that defaults on loans currently being originated should be expected to be six percent higher than the average of similar loans originated in the 1990s, due solely to the local and national economic environment.

According to UFA, the takeaway for investors and lenders is that despite these current favorable conditions for investors and lenders, continuing political uncertainty together with increases in interest rates, could elevate mortgage risks in the near future.

University Financial Associates

“Although house price forecasts have improved slightly, we would now characterize the economy as a 'late cycle' economy where risks are elevated,” said Dennis Capozza, who is Professor Emeritus of Finance in the Ross School of Business at the University of Michigan, and a founding principal of UFA. “In some local markets, including the important California housing market, UFA's real house price forecasts turn negative within two years. Watchful waiting is appropriate at this time.”

The August 2018 S&P/Experian Consumer Credit Default Indices [2] was also up, by two basis points, but painted a more positive picture. David M. Blitzer, Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices, notes that this index rate is an indicator of a relatively stable environment.

“Recent economic reports point to continued stability in consumer credit default rates,” said Blitzer. “A review of economic statistics covering the consumer economy is favorable. Job creation continues at about 200,000 per month with the unemployment rate at just below 4 percent and wage gains are approaching a 3 percent annual rate. While jobs and incomes advance, the spending side is showing modest retail sales growth and auto and home sales are flat to down. These trends favor stable default rates in the near term.”