DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Hispanic homeownership has steadily grown for seven consecutive years, and it is predicted that Hispanic households will account for 70% of homeownership growth over the next 20 years. But amidst a tight housing market, potential Hispanic homebuyers —especially first-time buyers— face many challenges. As Hispanic Heritage Month is celebrated nationwide, U.S. Mortgage Insurers (USMI) have taken the opportunity to reflect on the contributions this population has had on the U.S. housing market and economy, and what housing finance industry leaders can do to further expand minority homeownership and reduce the racial gap.

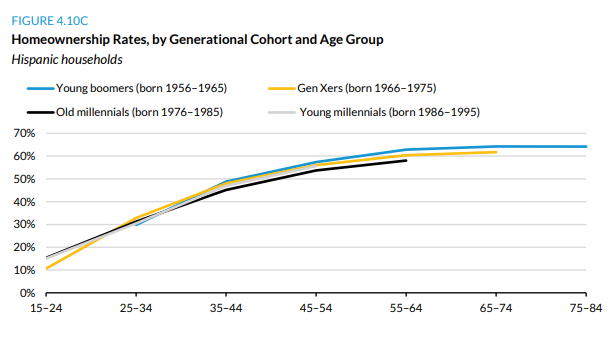

At first glance, Hispanics seem to be thriving. They accounted for over half (51%) of the nation’s growth between 2010 and 2020, and were responsible for the overwhelming majority (80.8%) of labor force growth. When it comes to homeownership, USMI predicted in 2021 that Hispanics will account for 53.1% of household formations over the next 20 years and this population seems to be well on their way. According to the National Association of Hispanic Real Estate Professional’s (NAHREP) “2021 State of Hispanic Homeownership Report,” the Hispanic homeownership rate increased to 48.4%, up from 47.5% in 2019, with an average increase of nearly one percentage point every two years—adding 657,000 Hispanic households between 2019 and 2021.

While this data is certainly encouraging, the projected future growth is not a promise. Hispanics, as with other minority groups, face a tight housing market with a historically low level of supply for affordable homes and record high home price appreciation (HPA), as well as systemic barriers such as large income gaps and lack of intergenerational wealth.

The nation’s monthly home supply dropped in 2021 to a new low in at least the last 10 years. A report by the National Association of Realtors (NAR) estimated the U.S. was short 5.24 million homes —an increase of 1.4 million homes from 2019. NAHREP noted in its report that areas of high Hispanic concentration are suffering the most severe impacts of this housing underproduction, and thus, seeing higher home prices. HPA increased 18.3% from May 2021 to May 2022, and homeownership seems even further out of reach for Hispanics when looking at the income gap. According to the U.S. Census Bureau, as of 2020, the median Hispanic household income was $55,321 while non-Hispanic white households were $74,312 —a 25.5% difference.

NAHREP writes in its report that Hispanics are the youngest of any ethnic or racial demographic in the United States: “At a median age of 30, Latinos are squarely in their prime home-buying years.” In a survey conducted by NAR in 2021, 34% of new Hispanic homeowners “purchased a home between the ages of 18 and 24, as opposed to only 17% of the general population.” Hence, young Hispanics are twice as likely to purchase a home. Moreover, the survey NAR® conducted found that “more than half of recent Latino homebuyers were first-time buyers.”

Considering the current challenges in the housing market and persistent barriers to homeownership, as well as the fact that most Hispanic homebuyers are younger, first-time buyers, what should the U.S. housing and home lending industries focus on to create an environment that is more conducive to first-time homebuyers, —especially communities of color?

Policies that seek to address them must be very specific in terms of identifying the borrowers being served, their issues and target outcomes. Further, there should be consistency in how the government and government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, approach initiatives related to access to home financing, which should aim to increase sustainable access to credit for borrowers that need assistance the most while also reducing credit risk. Additionally, the Federal Housing Administration (FHA) and Federal Housing Finance Agency (FHFA) should aim to implement policies that do not stoke additional demand in the marketplace, which have the potential of further driving up home prices and acutely impacting low- to moderate-income borrowers.

Specifically, USMI encourages the housing industry and policymakers to focus on:

- Affordable housing production;

- Financial and homeownership education and outreach; and

- A holistic review of GSE pricing, including reexamining 2008-era loan-level price adjustments (LLPAs), which disproportionately impact minority borrowers.

In the coming decades, it is minority households that will increase the rate of homeownership in America and be the driving force of the mortgage market according to UI research. As an organization representing an industry that exclusively serves homebuyers with limited access to funds for large down payments, USMI believes the issues and challenges facing these borrowers today will require significant collaboration amongst the industry stakeholders to ensure they have access to sustainable, affordable financing.

Private MI enhances the ability of minority and lower-income homebuyers to borrow in an affordable and sustainable way, enabling them to achieve housing stability and build wealth —realizing the American Dream is very much obtainable.

To read the full report, including more data and infographics, click here.