DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

A fire can be one of the worst days of a homeowner’s life—not only could it take years to recover emotionally from losing everything you own—it can be financially devastating, even after an insurance payout.

A fire can be one of the worst days of a homeowner’s life—not only could it take years to recover emotionally from losing everything you own—it can be financially devastating, even after an insurance payout.

ValuePenguin, a data analysis company owned by LendingTree, has found that the yearly cost of home insurances after a fire rises in every single state. In some states, the price does not just rise by a meager amount—it skyrockets.

For the report, Andrew Hurst, a SEO Marketing Research Analyst at ValuePenguin, analyzed 16 years of data from the U.S. Fire Administration and found that, on average, fires do a total of $8.1 billion in damage annually, or $138 billion total from 2003-2019.

“Insurance providers cover part of the fire damage costs on behalf of their policyholders, but these expenses result in higher prices,” Hurst said. “ValuePenguin calculated that the average cost of home insurance increases 27% after a residential fire. Depending on the state, average rates could rise by as much as 42% or as little as 6%.”

In four states the cost of insurance after a fire rose by 40%: Mississippi saw rates increase by 42% to an average of $2,236; West Virginia also increased by 42% to $1,673; Idaho rose by 41% to $1,486; and Oregon rose by 40% or $1,674.

The four states with the smallest rate increases were: Florida, where rates increased by only 6% on average to $2,094; Hawaii, an 11% increase to $1,210; Louisiana, a 15% increase to $2,022; and New York; 15% to $1,732.

One outlier is Colorado—it is the most expensive state in which to have a fire, but fire damage typically results in a lower markup than the rest of the country. After a fire damage claim, Colorado residents will typically see a price increase of 21% and can expect to pay an average of $4,097 for insurance.

Hurst also poised the question “Do homeowners need special fire insurance?” to which the answer depends on your location.

“You might consider purchasing standalone fire insurance instead of traditional home insurance to insure a property that is older or that has a history of claims as a way to mitigate the high cost of insurance. Or you might add it to a secondary residence or vacation home, which can sometimes be difficult to insure,” the report said. “Additionally, you might consider adding a dwelling fire policy to supplement your existing homeowners coverage. This could be because you live in an area susceptible to forest fires, or you may have simply experienced fire loss in the past and want extra peace of mind.”

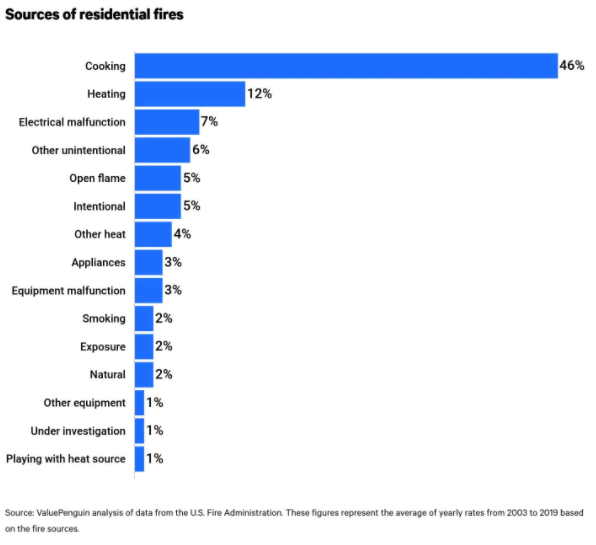

According to the available data, most residential house fires are directly caused by humans, mainly due to cooking.

“Data shows that cooking fires, stoves, ovens and other fixed sources of heat were to blame for an average of 46% of the yearly fires between 2003 and 2019. Further, between 2014 and 2019, cooking sources were the cause of at least half of residential fires, with a high point of 52% in 2017.”