DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

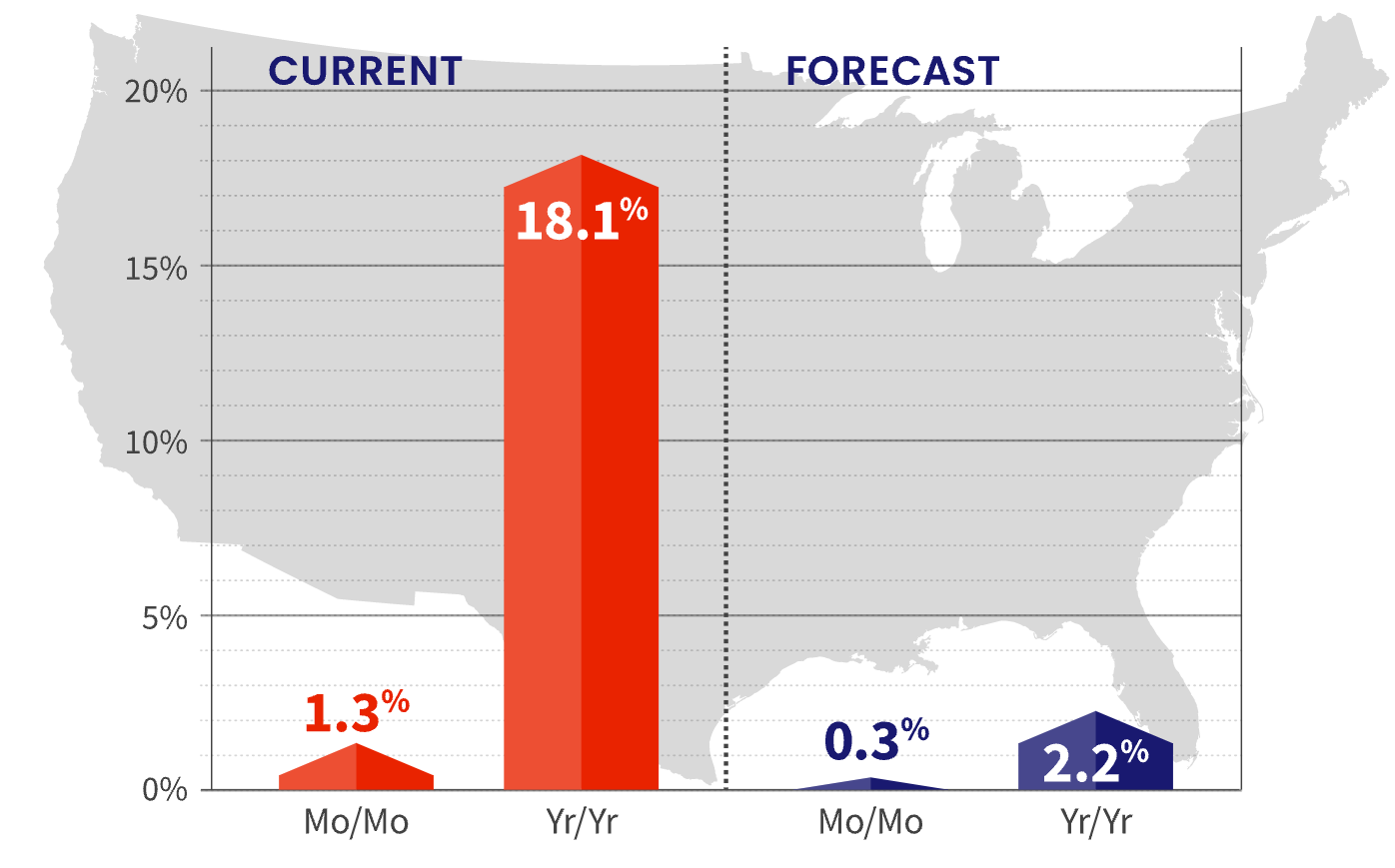

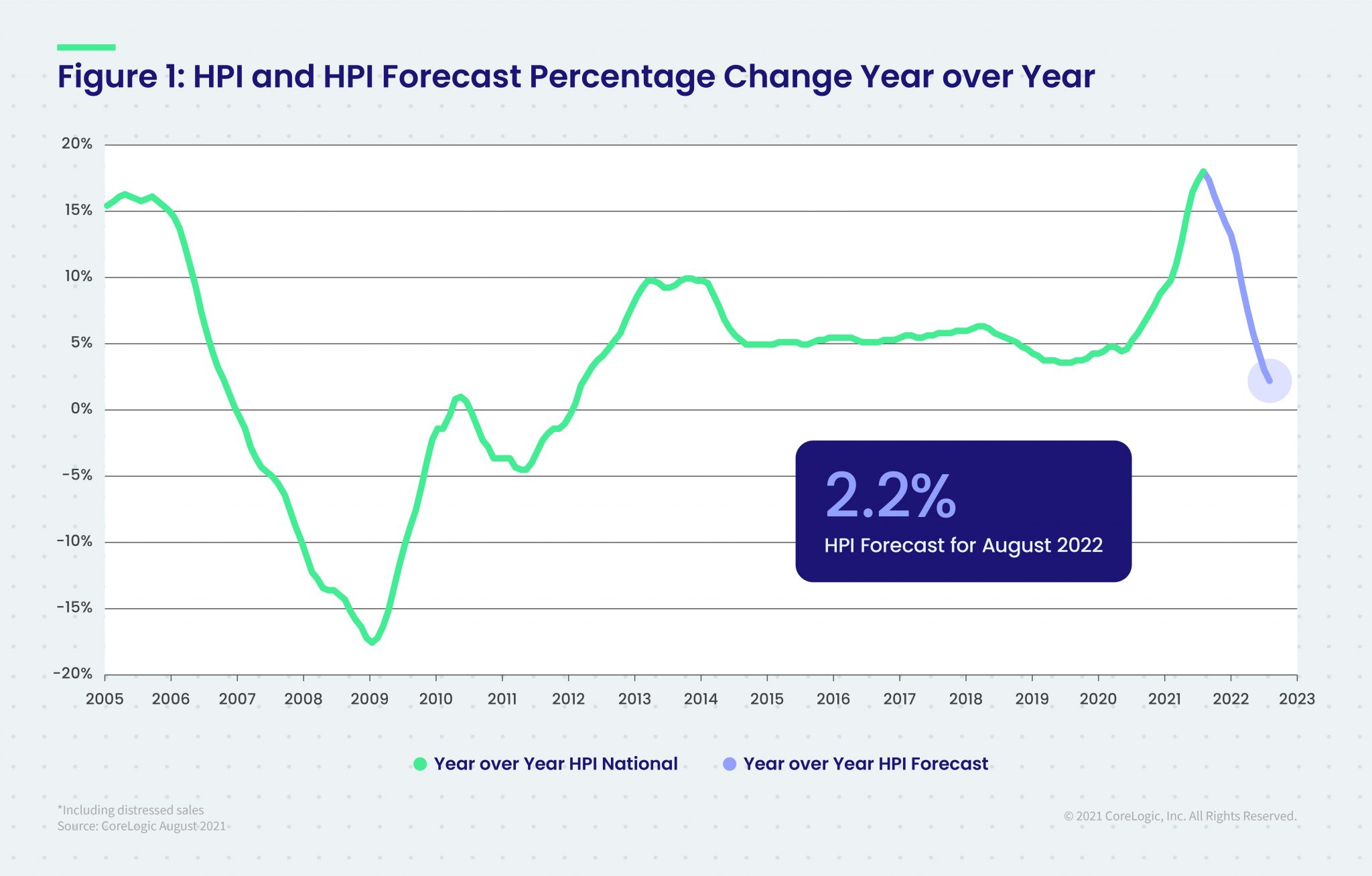

CoreLogic’s Home Price Index (HPI) and HPI Forecast for August 2021 has found that home prices rose to a fever pitch this summer, with annual price gains reaching an all-time high in August at 18.1%, compared to August 2020, marking the largest 12-month growth in the U.S. Index since the series began (January 1976–January 1977). On a month-over-month basis, home prices increased by 1.3% compared to July 2021.

CoreLogic’s Home Price Index (HPI) and HPI Forecast for August 2021 has found that home prices rose to a fever pitch this summer, with annual price gains reaching an all-time high in August at 18.1%, compared to August 2020, marking the largest 12-month growth in the U.S. Index since the series began (January 1976–January 1977). On a month-over-month basis, home prices increased by 1.3% compared to July 2021.

Continued affordability challenges within the housing supply-constricted market have also been exacerbated by an influx in homebuying activity from investors. As the home purchase market continues to boom and buoy the post-pandemic economy, these market factors are unevenly affecting access for some buyers. This is reflected in a recent CoreLogic consumer survey, where 59% of consumers looking to purchase a home reported combined household earnings of at least six figures, compared to the 10% of consumers looking to purchase earning less than $50,000.

Home price gains are projected to slow to a 2.2% increase by August 2022, as ongoing affordability challenges deter some potential buyers. In August, home prices rose sharply in the Pacific Northwest with Bend, Oregon experiencing the highest year-over-year increase at 37.2%, and Twin Falls, Idaho ranked second with a year-over-year increase of 35.8%.

At the state level, Idaho and Arizona led the way with the strongest price growth at 32.2% and 29.5%, respectively.

In August, appreciation of detached properties (19.8%) was again the highest measured since the inception of the index and 7.8-percentage points higher than that of attached properties (12%).

“Single-family detached homes continue to be in high demand,” said Dr. Frank Nothaft, chief economist at CoreLogic. “These properties offer more living space and distance from neighboring homes than that of attached properties. On average, detached homes have 28% more inside space compared to single-family attached properties and about twice as much space as apartments in multifamily structures.”

Frank Martell, President and CEO of CoreLogic, said, “Home prices continue to escalate at a torrid pace as a broad spectrum of buyers drive demand for a limited supply of homes. We expect to see the trend of strong price gains continue indefinitely with large amounts of capital chasing too few assets.”

With enhanced federal unemployment benefits and the eviction moratorium recently coming to an end, some workers are returning to work only to discover that no matter how much they work, a minimum wage job cannot earn an affordable rent payment in any state, thus further causing affordability issues for some.

According to a new report authored by Jacob Channel, Senior Economic Analyst for LendingTree, owning a home is less affordable for full-time minimum wage workers than renting one. On average, an affordable payment for minimum wage workers is $1,074 less than the median monthly housing costs paid by a homeowner with a mortgage.

“Though it’s cheaper than owning a home—at least when you’re still paying off a mortgage—renting is unaffordable to minimum wage workers in every state,” Channel said. “Across the nation, the average difference between an affordable monthly housing payment and median gross rent is $533.”

Economists at Fannie Mae have revised their expectations for near-term real GDP growth downward—and outward—due to persistent supply chain disruptions and labor market tightness, according to its September 2021 commentary from the GSE's Economic and Strategic Research (ESR) Group. Those factors, they say, will affect the housing market as the economy at large. While existing home sales recently came in stronger than expected, other indicators of home sales activity, including purchase mortgage applications and pending home sales, point to near-term softening. However, the lack of inventory of homes for sale continues to be the primary impediment, with the months' supply of inventory near historical lows and the pace of new listings too low to sustain the current sales pace. Home construction is also being held back by supply problems, and as such the ESR Group downgraded its expectations for Q4 new home sales from 846,000 units to 789,000 units. The forecast for purchase mortgage originations was little changed for 2021, but the ESR Group now envisions a 6.3% increase for 2022; meanwhile, refi origination volumes are expected to decline from a 58% share of total mortgage origination activity to 40% in 2022.