DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Millennials typically forge their own path in life, bucking the trends and norms of their parents—and now that they are in the prime home-buying time of their lives, their views on home equity have also changed.

Millennials typically forge their own path in life, bucking the trends and norms of their parents—and now that they are in the prime home-buying time of their lives, their views on home equity have also changed.

According to a new survey, millennials, now in the 25-40-year-old age range, have a much different idea of what home equity should be used for than what has been seen traditionally.

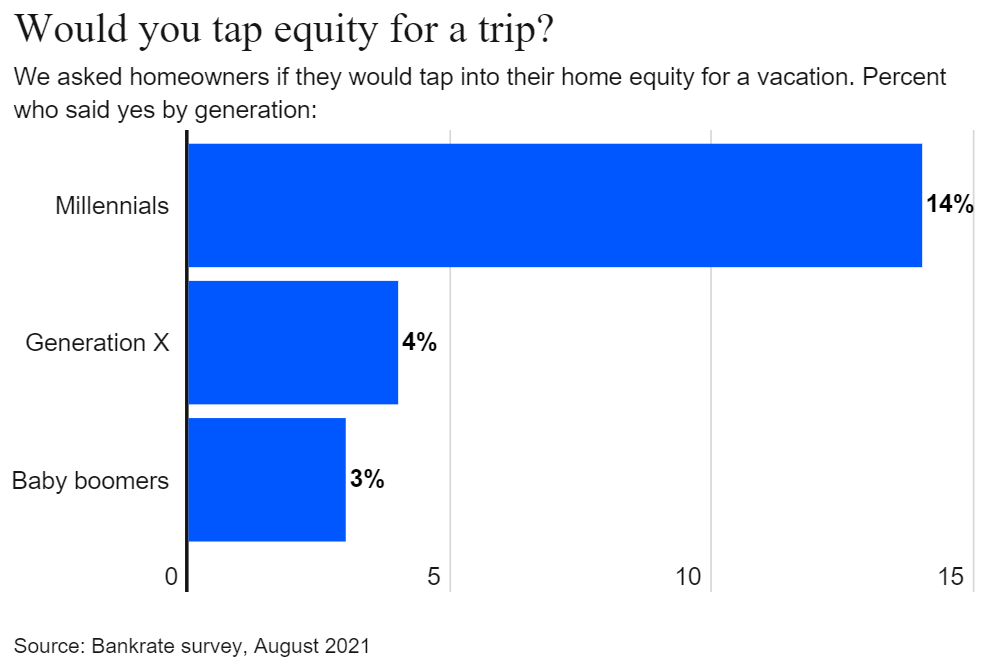

The survey, conducted by Bankrate.com, found that 14% of millennial mortgage holders say they would pull cash out of their mortgage in order to go on a vacation, compared to 4% of Generation Xers and 3% of baby boomers.

In addition, 10% of millennials would use the extra cash for non-essential luxuries, such as a boat or electronics.

When asked about using home equity for home improvements, 49% of millennials said they would use their equity on home improvements, compared with 64% of Generation Xers and 66% of boomers.

According to Michael Golden, co-founder and co-CEO of @properties in Chicago, the information isn’t much of a surprise—millennials place a higher value on their work/life balance than their older peers do.

According to Michael Golden, co-founder and co-CEO of @properties in Chicago, the information isn’t much of a surprise—millennials place a higher value on their work/life balance than their older peers do.

“They’re a little bit more balanced,” Golden says. “Life experiences are a little more important to them. They’re willing to spend money in a different way, and they’re willing to tap equity in their home in a different way.”

While traditionalists have always been wary of tapping into home equity, Credit.org President Melinda Opperman said many homeowners regretted pulling cash out of their home during the last housing boom that preceded the Great Recession.

“Building up wealth in a home is a long, deliberate process, and that wealth creation increases the longer one stays in a home,” Opperman said. “In general, we wouldn’t advise anyone cash out that equity unless they’re using it to improve the property, thereby increasing the value of the home and rebuilding equity faster.”

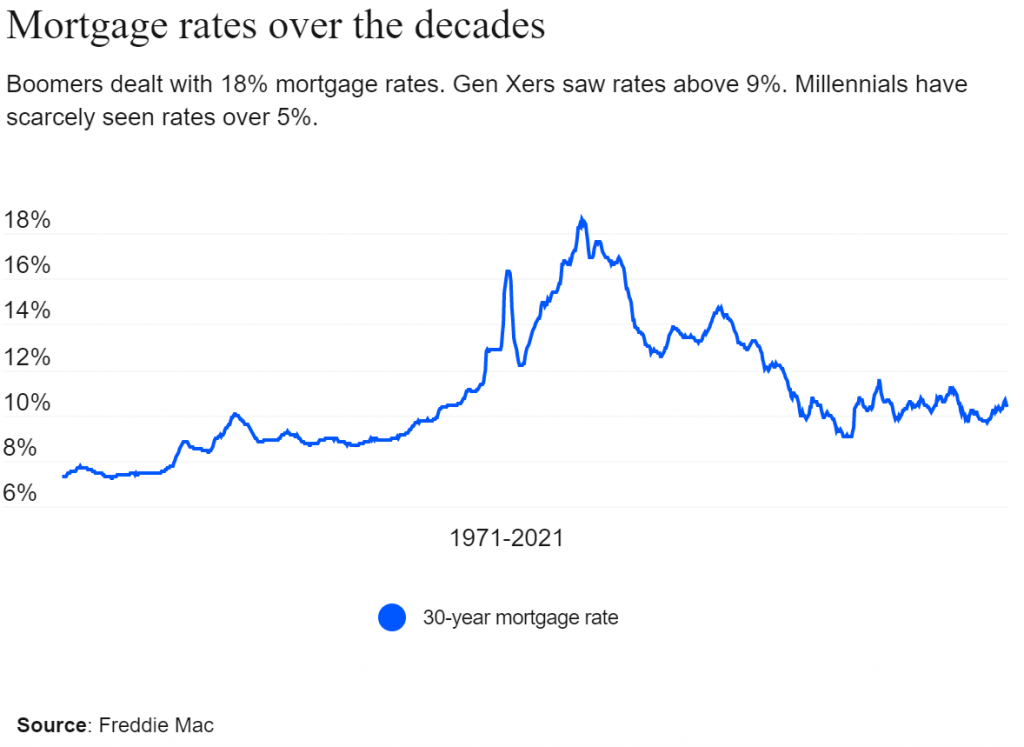

According to Jeff Ostrowski, the author of the report, millennials have been shaped by the market and the failures of the generations before them and, are hard-pressed to remember mortgage rates above 5%.

“By contrast, baby boomers lived through 30-year mortgage rates topping 18 percent in the early 1980s,” Ostrowski said. “Gen Xers experienced rates hovering at 9 percent in the 1990s. Millennials barely recollect 5% rates—from Jan. 1, 2010, to Jan. 1, 2020, the average rate on a 30-year loan was just above 4%”

“By contrast, baby boomers lived through 30-year mortgage rates topping 18 percent in the early 1980s,” Ostrowski said. “Gen Xers experienced rates hovering at 9 percent in the 1990s. Millennials barely recollect 5% rates—from Jan. 1, 2010, to Jan. 1, 2020, the average rate on a 30-year loan was just above 4%”

Then came the COVID-19 pandemic, and 30-year mortgage rates fell below 3 percent, the lowest levels ever,” Ostrowski continued. “With borrowing so cheap, old rules about avoiding debt might strike some as less relevant.”

Another factor in millennials’ equity decisions come from the recent housing boom. According to the latest S&P CoreLogic Case-Shiller report, U.S. home prices jumped a record 19.7% from July 2020 to July 2021.

“Tapping home equity is possible only if you have equity, and homeowners have it in unprecedented amounts,” the report said. “According to mortgage data firm Black Knight, Americans possessed more than $9.1 trillion in “tappable” home equity as of mid-2021.”

“Some of the attitudes toward home equity may be influenced by the recent surge in home prices,” says Greg McBride, Bankrate’s Chief Financial Analyst. “Those that recall the housing bust and how highly leveraged homeowners got squeezed are likely more reluctant to tap equity unless absolutely necessary.”