DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Editor's note: This piece originally appeared in the October issue of DS News, out now.

Editor's note continued:

Dear DS News readers,

It is not often that I am compelled to introduce a story that you are about to read. However, this month’s cover story, “FHA’s Timely IT Modernization” deserves a prelude to frame both its significance for our industry and the broader lessons that the system at large can learn.

At times, government processes are synonymous with “slow-moving” and “behind the times.” But Brian Montgomery has defined his time in the role of HUD Deputy Secretary to modernizing FHA. The execution of this bold plan most critically involved hearing from all stakeholders to determine what worked, what did not work, and what path this modernization should take.

I had the privilege of witnessing this collaboration first-hand when I took part in a meeting held at HUD offices with members of the National Mortgage Servicing Association. Time and again, I saw a true exchange of ideas and dialogue that heralded a new age in FHA—one where processes met the day-to-day challenges of real practitioners and the needs of the American homeowner.

2020 has presented our business with unprecedented challenges. But even in normal times, the viability and dynamism of our industry is one of the most critical variables that underpins our economy. The modernization of FHA will both maximize the efficiency of the market in the good times, and best prepare it for the unforeseeable challenges that lie in our future.

I hope you enjoy reading this exclusive article, as much as we enjoyed making it possible.

Sincerely,

Rachel Williams , Editor-in-Chief

FHA’s Timely IT Modernization

As the coronavirus pandemic arrived in America, it revealed many of our country’s great strengths, most notably the resilience and determination of our people to overcome adversity.

A close second has been our nation’s technological leadership and the innovative spirit of U.S. businesses to deliver goods and services in alternative, safe, and effective ways.

You can place the venerable Federal Housing Administration (FHA) in that category. Created in 1935, the FHA is the agency most responsible for expanding minority homeownership, helping to house vulnerable populations, and supporting housing markets, when needed, in times of economic stress.

Were it not for a timely investment in the modernization of FHA’s information technology (IT) systems—a generational shift in the way FHA does business—FHA might have been ill-equipped to handle the challenges of this more-fully digital age. What could have been an unfortunate tale of a government bureaucracy missing its mission has instead turned into a story of success.

Nearly two years ago, the Administration requested—and Congress listened and provided—a $20 million down payment for FHA’s IT modernization, with another $20 million the following year. That’s half of what the FHA IT team believes it needs to fully modernize its business systems.

Since then, FHA has proceeded at a relentless pace, building a platform that supports the mission and the demands of the modern real estate finance marketplace. Led by a team of professionals within HUD’s Office of the Chief Information Officer (OCIO), FHA staff, and outside contractors, FHA constructed the new system, fittingly named “FHA Catalyst,” when complete will provide a completely digital end-to-end lifecycle for FHA-insured loans.

A 21st-Century Upgrade

Prior to this effort, the 85-year old agency had been known in housing circles for outdated and obsolete, systems, cumbersome processes, and lack of agility—qualities ill-suited for the modern marketplace, and even less so when called upon to act quickly during national emergencies.

FHA’s information technology infrastructure was fragmented, cobbled together as resources allowed, and was stubbornly stuck in the past. Funding through the years was barely enough to maintain the same antiquated systems built through a patchwork of efforts over decades. What’s more, FHA’s systems and processes were woefully behind those of the government-sponsored enterprises, Fannie Mae and Freddie Mac, who had spent years and tens-of-millions reinventing their technology platforms.

In many instances, FHA lenders were forced to send large documents over email, often needing to break them up to reduce file sizes, or physically mailing CDs or thumb drives. More recently, lenders have been sharing application data and documents via secure online dropbox.

For aspects of FHA business that had been moved to seemingly more elegant digital solutions, in many cases they had to be paired with inefficient, Rube Goldberg-like processes on the backend in order to accommodate FHA’s disparate systems. The gaps were filled with manual processes or low-tech adaptations.

In short, prior to this year, lenders and servicers working with FHA faced multiple access points for a single application, with large portions of the process conducted via paper files that were shuttled between FHA’s offices and lenders.

None of these methods were efficient or reliable, introducing additional risks to the program. With 8.5 million active loans in a $1.3 trillion single family insurance portfolio, and 1 million new endorsements and tens of thousands of claims each year, the pandemic could have severely limited FHA’s capacity to serve its mission.

All of that has changed or is in the process of being changed.

A Tech Transformation

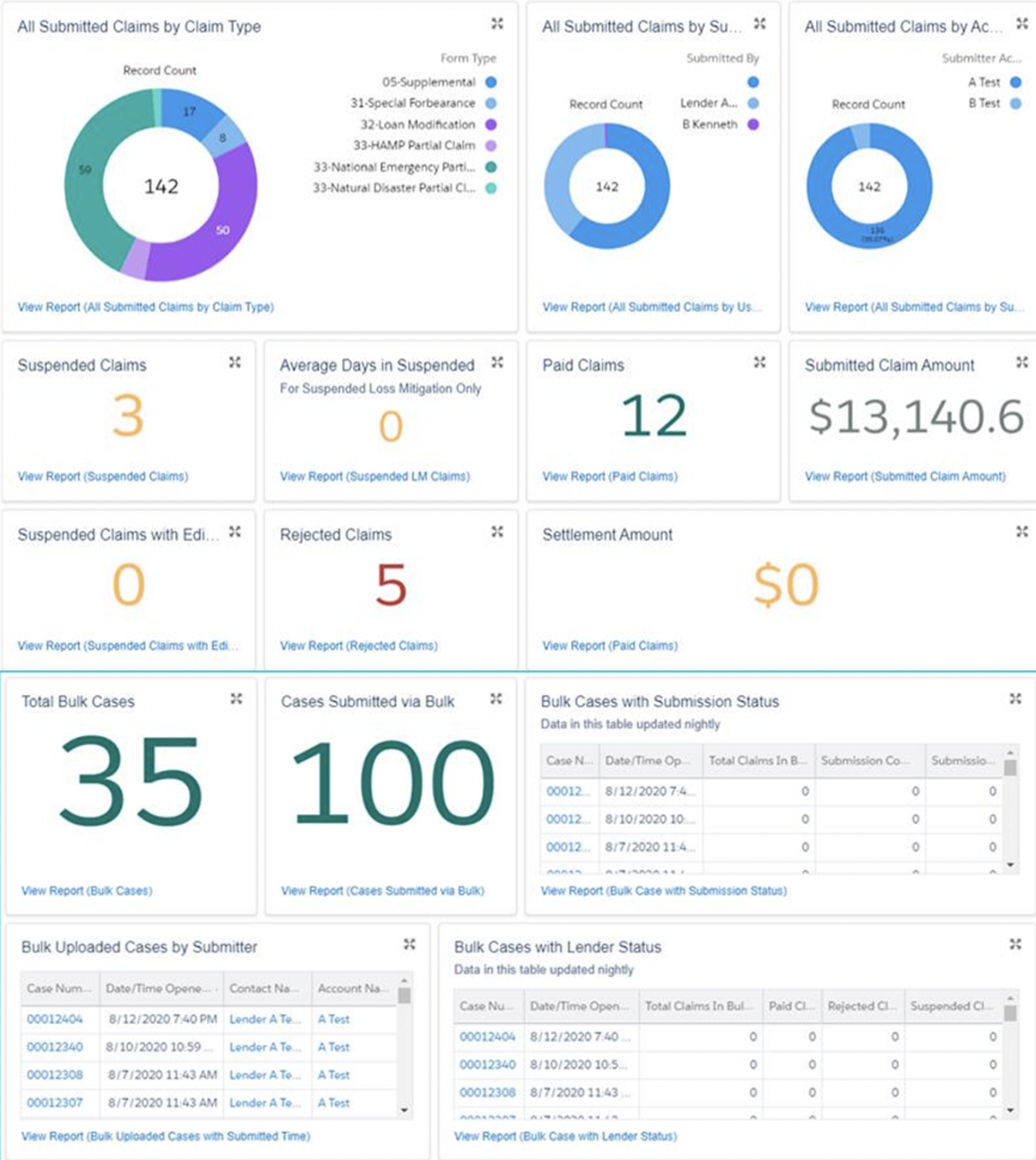

Late last year, after many months of hard work, FHA stood up the new platform and began the journey of transforming the IT infrastructure, first by introducing a claims “module” for the electronic submission of “supplemental” claims, claims submitted after an initial claim is filed. Previously a laborious, paper-intensive, manual process, these claims can now be transmitted directly to HUD electronically, and in bulk, via FHA Catalyst.

The important point is that, rolling into 2020, the platform on which the claims module was placed was built to be agile and adaptable to needs within a fast-moving, digital world.

The FHA and OCIO team were humming along when the COVID-19 pandemic arrived on our shores. Undeterred, the team persevered and didn’t miss a beat, rolling out new improvements in record time.

When HUD Homeownership Centers around the country moved to telework in March, the platform was swiftly adapted, in a matter of days, for Electronic Document Delivery (EDD). EDD digitizes what were previously hard-copy loan origination case binders from lenders without the authority to endorse FHA loans, so they can submit them electronically for approval. This improvement alone will save the industry an estimated $200 million per year in administrative fees associated with paper document submission.

At hundreds of pages each, the binders would have been piling up at Homeownership Centers around the country during the pandemic, but instead can now be processed by FHA staff from their remote locations. To protect borrowers and the integrity of the system, the deployment included completion of mandated cybersecurity assessments and authorizations.

FHA Catalyst will be ready to receive all COVID-19 national emergency-related claims, which FHA can expect in large numbers – —potentially to the tune of hundreds of thousands – —avoiding an unthinkable amount of paper and inefficiency.

Late this summer, FHA began direct integration with lenders and appraisal management companies so that the platform can now accept electronic receipt of appraisals directly from their outside systems, while providing real -time feedback on appraisal data requirements.

By early fall, the FHA system will be fully evolved to accept all additional claim types, and soon after, the full submission of loan applications and endorsements. Meanwhile, the platform is already providing both FHA and Ginnie Mae greater data visualization and analytics to monitor COVID-19 forbearance and default impacts along with HUD CARES Act grants. A new, customizable “dashboard” for FHA lenders is now available to improve both efficiency and transparency.

To top it off, the transformation being undertaken within FHA has provided the foundation for information technology modernization across all of HUD. Originally focused on FHA Single -Family programs, FHA Catalyst’s development and delivery methodology has provided a model to be emulated by other program offices.

Piloting Toward Success

Beginning in February, a pilot program on FHA Catalyst that utilizes “robotic process automation” capability has been monitoring the expiration of contracts in FHA’s Multifamily program, which supports millions of subsidized renters. This “bot” is performing an oversight function that is vital during any crisis, a lesson we learned in early 2019 during a government shutdown. Since then, we have built a governance structure and security authorization process with 31 of these “bots,” which could potentially save agency 60,000 hours annually.

The EDD Module on FHA Catalyst can also now accept Multifamily Housing applications and HUD’s Public and Indian Housing Office of Native American Program “Section 184/184A” case binder applications.

In the end, HUD stands to realize significant cost savings and reduce time-to-market by leveraging the functionality of FHA Catalyst across its vast program areas, while decommissioning costly legacy systems and 3rd third-party licensed software.

FHA modernization has been a monumental change in the way the agency portends to do business moving forward. It is, again, a generational shift, perhaps multigenerational if the flexibility of the platform holds for years to come.

To be clear, there is still a long way to go in this process. Much of the FHA IT infrastructure still sits on two mainframe computers, which curtails real-time processing and access. The system that insures new FHA loans is 45 years old, while the other two core systems which manage the active insurance portfolio and disburse claims are both 37 years old. Seventeen official sub-systems support these three main components, and countless unofficial “shadow IT” systems support their integration.

As all of this is being phased out rapidly, FHA is phasing in the ability to respond effectively, provide efficient access and service to our partners, and analyze data in order to enhance the availability of FHA products while protecting taxpayers exponentially. HUD’s newly- confirmed Assistant Secretary for Housing and Federal Housing Commissioner, Dana Wade, is committed to the completing this transformation and maintaining the rapid pace of these historic improvements to FHA’s business.

It is fair to say, were it not for the timely investment that allowed FHA to begin deployment late last year, COVID-19 would have exposed an inadequate system, nearly incapable of responding to the rapid turn in economic events and the urgent need for more digital solutions.

Instead, HUD and FHA have made a bold, giant leap forward into the modern world. The investments have made an enormous difference, are paying enormous dividends to American taxpayers, and the future is looking even brighter.