DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

New research by Knock, a digital homeownership platform, confirmed something that many homebuyers have already discovered: they are being priced-out of the new home market.

New research by Knock, a digital homeownership platform, confirmed something that many homebuyers have already discovered: they are being priced-out of the new home market.

While the uptick in new construction has been viewed as a positive sign for buyers, soaring prices and low inventory have pushed those who can afford it to seek newly or custom-built homes instead of purchasing existing ones. This is occurring even as more builders shift their focus to smaller homes to accommodate the entry-level market.

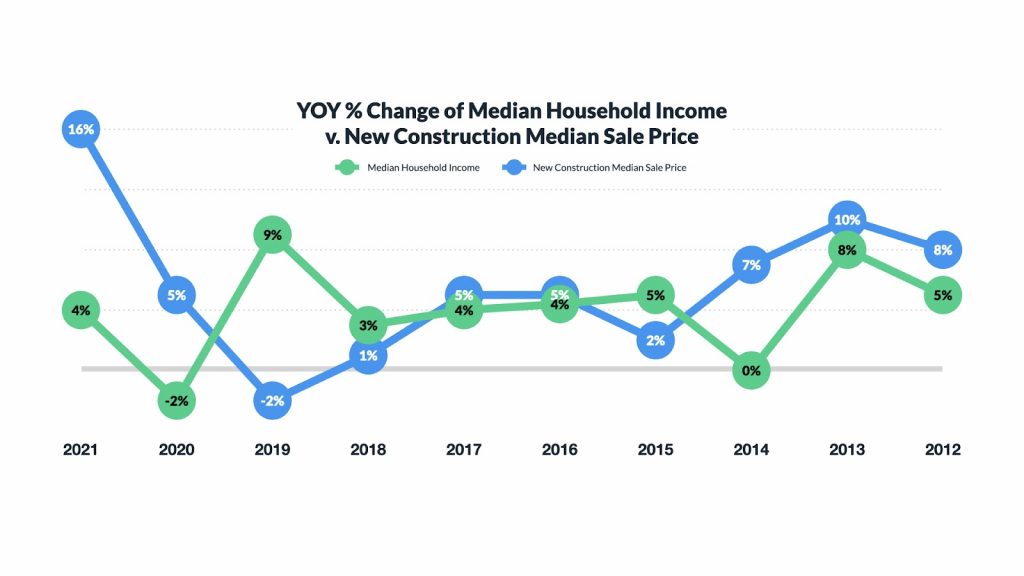

New construction also comes with a typical 20% premium versus existing stock adding additional fuel to the fire of rising home prices, so Knock compared the median household income and the median new home sales price in the nation's largest metropolitan areas with the most active new home markets to determine just how much relief new construction will provide as buyers—especially first-time homebuyers—are grappling with affordability in a highly competitive housing market.

According to Knock, to afford the mortgage on a $390,900 home (the current median price of a new home), a buyer making a 6% down payment (assuming 30 years at an interest rate of 3.04%) would need to earn $80,000 a year, pricing out 60% of Americans as the national median household income is $67,521.

"This analysis highlights how years of building undersupply and the current supply shortages are disproportionately impacting lower income homebuyers looking for alternatives in a housing market where homes are garnering multiple offers and selling for over asking price," said Sean Black, the Co-Founder and CEO of Knock. "Although more new homes are expected to come onto the market in 2022, wages have not kept up with home price growth, keeping new construction out of reach for many, especially first-time buyers who don't have the benefit of equity from a home sale."

In September, Fannie Mae lowered its 2022 new construction expectations from 846,000 units to 789,000 due to supply chain constraints and record home price issues the country is currently facing, which could foreshadow an even longer recovery from years of underbuilding by developers.

The National Association of Realtors found through a survey that 60% of buyers want a new home over an existing one. But this is overshadowed by the struggle many new buyers experience as they save up for a down payment as the average home a first-time buyer purchases is now $299,000.

Based on median household income, the average time it takes to save for a down payment on a new construction home for first-time homebuyers is 15 years.

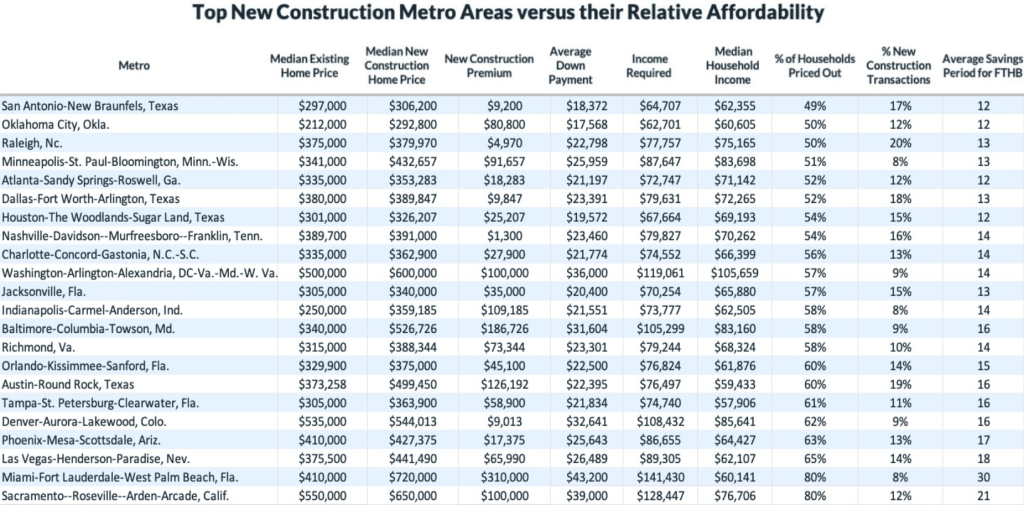

- The areas with the shortest down payment savings time are Houston, Oklahoma City, San Antonio, and Atlanta at just 12 years.

- Those with the longest savings periods include; Miami (30), Sacramento (21), Las Vegas (18), and Phoenix (17).

- In metro areas with below-average levels of new construction transactions, saving’s periods rise significantly. Ranging from 115 years in New York City, to 127 in San Jose, 153 in Los Angeles, and 167 years in San Francisco.

Based on Knock’s analysis, they found the following metro areas at both ends of the affordability spectrum based on required household income for the median new construction mortgage in their area:

- Sacramento (80%), Miami (80%), Las Vegas (65%), Phoenix (63%), and Denver (62%) have the highest percentage of households unable to afford new construction.

- San Antonio (49%), Oklahoma City (50%), Raleigh (50%), Minneapolis (51%), Atlanta (52%), and Dallas (52%) provide the most accessible new construction for homebuyers.

- When comparing the price paid for a new home, the average premium of new construction to existing resale to be $68,454.

- Metro areas showing the smallest premium for new construction to existing homes include Nashville ($1,300), Raleigh ($4,970), Denver ($9,013), San Antonio ($9,200), and Dallas ($9,847).

- Those showing the largest premium between new and existing homes include, Miami ($310,000), Baltimore ($186,726), Austin ($126,192), Indianapolis ($109,185), Washington ($100,000), and Sacramento ($100,000).

“The current supply chain and affordability issues surrounding new construction challenge pre-Covid notions of the relief to the housing market new construction homes bring,” the report concluded. “If new construction homes do not align with the buying power of the average consumer, benefits of this additional inventory are felt disproportionately throughout the country and are attenuating a much smaller portion of the building gap issue than previously thought. Moving forward, we expect to see a push back in median new construction home pricing as the reality of homeownership of the majority becomes simply too far out of reach.

To view a full copy of the research, click here to view it on Knock’s website.