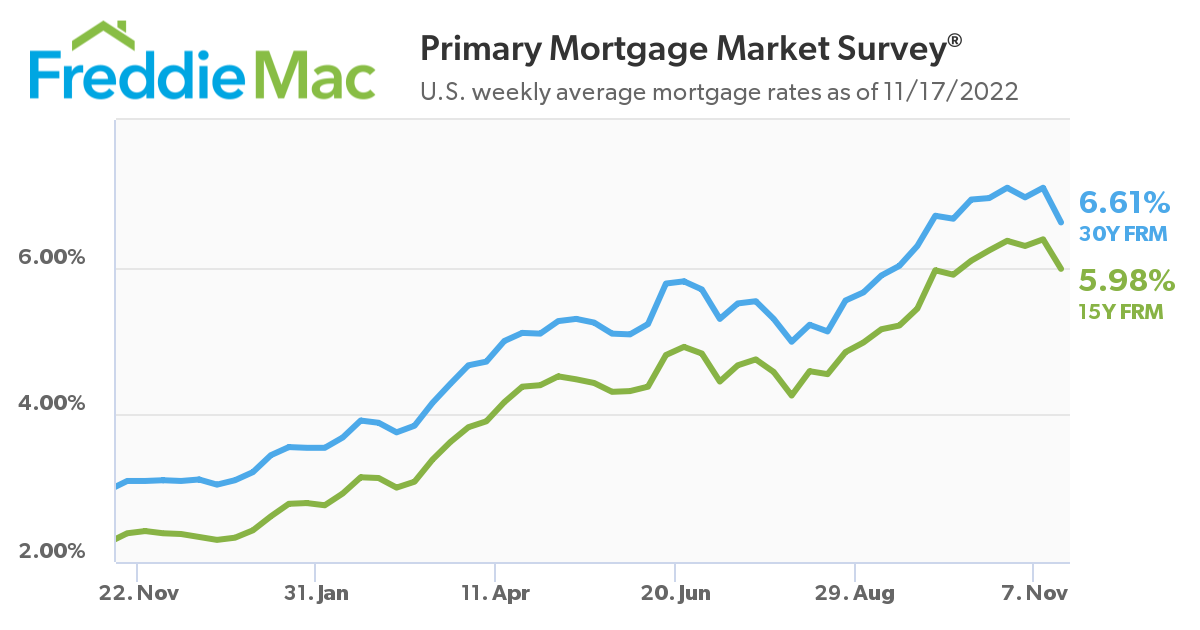

Freddie Mac reports that the 30-year fixed-rate mortgage (FRM) tumbled 47 basis points week-over-week [1], averaging 6.61% for the week ending November 17, 2022, down from last week when it averaged 7.08%. A year ago at this time, the 30-year FRM averaged 3.10%.

Freddie Mac reports that the 30-year fixed-rate mortgage (FRM) tumbled 47 basis points week-over-week [1], averaging 6.61% for the week ending November 17, 2022, down from last week when it averaged 7.08%. A year ago at this time, the 30-year FRM averaged 3.10%.

“Mortgage rates tumbled this week due to incoming data that suggests inflation may have peaked,” said Sam Khater, Freddie Mac’s Chief Economist [2]. “While the decline in mortgage rates is welcome news, there is still a long road ahead for the housing market. Inflation remains elevated, the Federal Reserve is likely to keep interest rates high and consumers will continue to feel the impact.”

Also this week, Freddie Mac reported the 15-year FRM averaging 5.98%, down 40 basis points from last week when it averaged 6.38%. A year ago at this time, the 15-year FRM averaged 2.39%.

The drop in mortgage rates has spurred a rise in mortgage application volume last week as well, as the Mortgage Bankers Association (MBA) reported overall mortgage application volume rose [3] 2.7% week-over-week for the week ending November 11, 2022.

“Application activity, adjusted to account for the Veteran’s Day holiday, increased in response to the drop in rates–driven by a 4% rise in home purchase applications,” added Joel Kan, MBA’s VP and Deputy Chief Economist [4]. “Purchase applications increased for all loan types, and the average purchase loan dipped to its smallest amount since January 2021. Refinance activity remained depressed, down 88% over the year. There is very little refinance incentive with rates so much higher than last year.”

Affordability remains an issue as Redfin reports that the nation’s homebuyers must now earn $107,281 [5] to afford a $2,682 monthly mortgage payment on the typical U.S. home, up 45.6% from $73,668 a year ago. From February 2020 to October 2022, the monthly payment for an American family buying the median-priced home increased by roughly 70%. Affordability challenges are a major reason why home sales have slowed so dramatically over the last few months.

“High rates are making buyers rethink their priorities, as many of them can no longer afford the home they want in the location they want,” said Washington, D.C. Redfin Agent Chelsea Traylor [6]. “If you had a $900,000 budget a few months ago, rising rates mean it’s now around $700,000–and sellers aren’t dropping their prices enough to make up for the change. So buyers are searching further away from the city in more affordable areas or waiting for prices and/or rates to come down before making a move.”