DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

The national foreclosure inventory is experiencing the fastest rate of decline since 2014, according to the latest Mortgage Monitor presented by Black Knight Financial Services, and what’s more–there is no sign of it slowing down.

“We’ve seen an improvement in both inflow and outflow of foreclosure inventories. In fact, October saw the lowest foreclosure start volume in nearly 12 years – and the lowest first time foreclosure start volume on record, dating back prior to the year 2000,” says Ben Graboske, EVP of Black Knight Data & Analytics. “There has been a corresponding rise in foreclosure completion rates (loans either being sold at foreclosure sale or otherwise liquidated). Sustained home price appreciation rates over the past four plus years, combined with generally tight for-sale inventory, have been key drivers there. Finally, we’ve also seen an increase in the share of active foreclosure loans that are being paid current or re-performing over the past 24 months.”

In addition to foreclosure inventory declining to pre-crisis levels, the report indicates that the national 90+ delinquent inventory is on track to reach pre-crisis norms come late 2017. Black Knight reports that it should fully cross this mark in mid-2018.

“Tighter lending standards post-recession have led to pristine mortgage performance in recent vintages. We’ve now seen default rates ‘over-correct’ and actually fall below long-term norms,” says Graboske. “This has led to historically low new troubled loans rates with about 60 percent of new default activity still coming from loans with nine or more years of seasoning, which continue to default at four times the rate of more recent originations. Additionally, the healthy employment market has enabled many borrowers to remain current on their mortgage payments.”

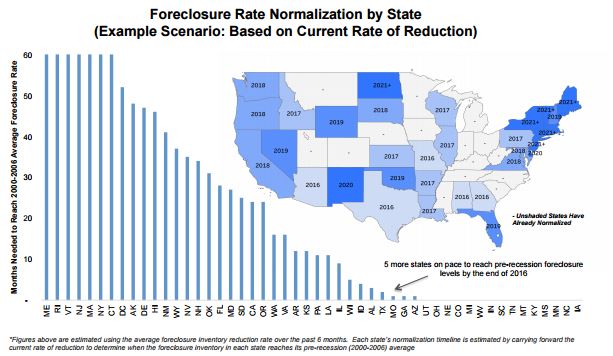

The report has found that 15 states have already hit levels lower than those of pre-crisis, with five more states (Alabama, Texas, Missouri, Georgia, and Arizona) forecasted to hit pre-crisis foreclosure levels by the end of the year.

Despite this good news, Black Knight reports that there are still seven states that are anticipated take five years or more to normalize at their current rates of improvement. These states are clustered in the Northeast.

“Outflow continues to be the main hindrance in the northeastern part of the country, where the bulk of states operate under judicial foreclosure processes,” says Graboske.

According to the report, these states still struggling with improving their foreclosure levels to those of pre-crisis include Maine, Rhode Island, Vermont, New Jersey, Massachusetts, New York, and Connecticut.

“In New York for example – which has the highest remaining active foreclosure inventory in the country – only two percent of active foreclosures are completed on a monthly basis,” adds Graboske. “That’s a third of the national average completion rate of six percent and the lowest of any state in the country. It’s also one of the reasons why the average mortgage in active foreclosure in New York has been delinquent for 4.6 years, as compared the national average of 2.2. In addition to court delays, there are also mandatory mediation programs in some states which, while important, tend to further slow the process.”

To view the full October Mortgage Monitor, click HERE.