DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

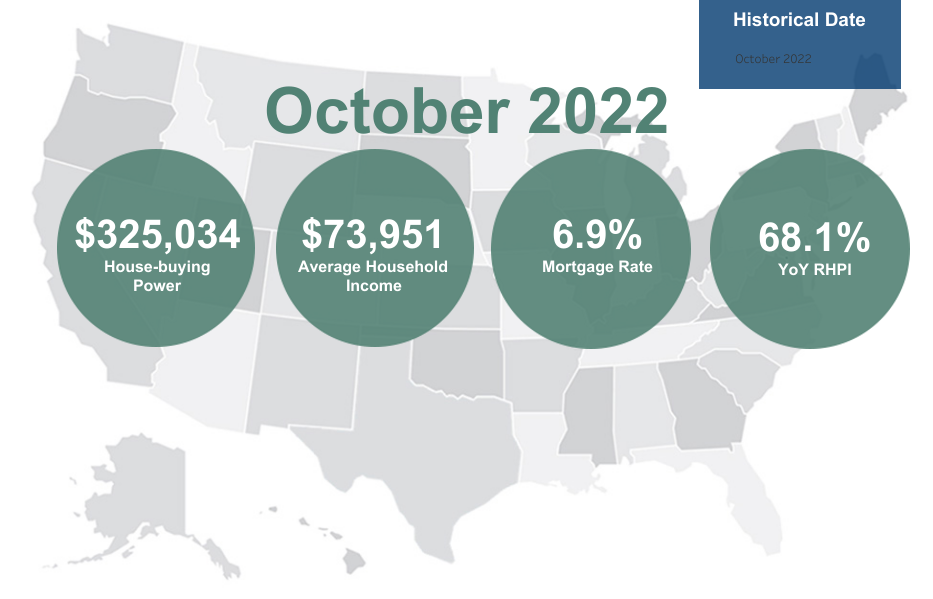

First American Financial Corporation has released the October 2022 First American Real House Price Index (RHPI), measuring the price changes of single-family properties throughout the U.S. adjusted for the impact of income and interest rate changes on consumer house-buying power over time at national, state and metropolitan area levels.

First American Financial Corporation has released the October 2022 First American Real House Price Index (RHPI), measuring the price changes of single-family properties throughout the U.S. adjusted for the impact of income and interest rate changes on consumer house-buying power over time at national, state and metropolitan area levels.

First American found that real house prices increased 8.7% month-over-month between September 2022 and October 2022. Year-over-year, real house prices increased 68.1% between the 12-month span of October 2021 and October 2022.

“Affordability continued to suffer in October 2022, as the RHPI jumped up by 68% on an annual basis. This rapid annual decline in affordability was driven by a 12% annual increase in nominal house prices and a 3.8-percentage point increase in the average 30-year, fixed mortgage rate compared with one year ago,” said Mark Fleming, Chief Economist at First American. “Even though household income increased 3.4% since October 2021, and contributed positively to consumer house-buying power, it was not enough to offset the affordability loss from the dramatic surge in mortgage rates and fast-rising nominal prices.”

Consumer house-buying power, defined as how much one can buy based on changes in income and interest rates, decreased 7.5% between September 2022 and October 2022, and decreased 33.3 percent year over year.

“As affordability wanes and prompts buyers to pull back from the market, nominal house price appreciation has slowed. Nationally, annual nominal house price growth peaked in March at nearly 21%, but has since decelerated by more than eight percentage points to 12% in October,” said Fleming. “Does waning house price appreciation signal that we may be past the worst of the affordability crash and affordability may be poised to rebound in 2023?”

As the U.S. economic landscape continues to stabilize amid Fed rate hikes, the nationwide median household income has increased 3.4% since October 2021, and 78% since January 2000.

“The labor market continued to impress in October, as rising wages resulted in higher household income,” said Fleming. “Annual hourly wage growth increased by 4.9% compared with a year earlier, job growth is steady, and the unemployment rate remains low. The rise in wage growth contributed to a 3.4% year-over-year increase in median household income. Compared with October 2021, the rise in household income alone increased consumer house-buying power by approximately $16,000. But the labor market faces growing uncertainty, as the Federal Reserve continues to tighten monetary policy to curtail demand and slow inflation. Next year, it will be increasingly difficult for the Fed to fight inflation so intensely without broader impacts to employment. For now, the labor market continues to face a labor shortage, which puts upward pressure on wages and, therefore, household income. The labor shortage will likely wane in 2023, meaning the pace of wage growth will likely slow as well.”

After six consecutive weeks of decline, 2022 ended with the 30-year fixed-rate mortgage (FRM) bounding back upward last week to close out the year, as Freddie Mac’s latest Primary Mortgage Market Survey (PMMS) found the 30-year FRM up week-over-week, rising 15 basis points to 6.42%.

“Mortgage rates more than doubled in October compared with one year ago,” added Fleming. “The spike in mortgage rates from 3.07% last October to 6.9% this October reduced house-buying power by nearly $178,000, holding income constant. Partially offset by gains from household income, the net effect on house-buying power was a decline of approximately $162,000 compared with October 2021. Looking ahead to 2023, an average of industry forecasts indicates that mortgage rates are expected to end next year at approximately 6%, as inflation is expected to recede, which may provide a modest boost to consumer house-buying power at the end of 2023 compared with this year.”

According to First American, real house prices were 49.5% more expensive in October than in January 2000. Unadjusted house prices are now 55.6% above the housing boom peak in 2006, while real, house-buying power-adjusted house prices are 5.5% above their 2006 housing boom peak.

“American author John Naisbitt once said, ‘the most reliable way to forecast the future is to try and understand the present.’ It’s true that economic forecasting is a humbling experience, but understanding the dynamics in the housing market today provides some insight into what may occur next year,” said Fleming. “If mortgage rates fall to 6% by the end of 2023 as the industry average predicts, household incomes remain flat on an annual basis due to a narrowing labor supply-demand gap and slowing labor market, and nominal house prices decline by 0.3% annually as the industry forecasts, then affordability as measured by the RHPI will improve by 9% by the end of next year compared with October 2022. A more affordable housing market will be welcome news for buyers currently sitting on the sidelines. Given the large loss of affordability buyers experienced this year, a possible improvement next year will be a welcome relief for potential buyers.”

Regionally, the five states reporting the greatest year-over-year increase in the RHPI included:

- Florida (+86.3%)

- Georgia (+74.4%)

- Alabama (+72.6%)

- New Hampshire (+72.1%)

- Alaska (+71.9%)

There were no states with a year-over-year decrease in the RHPI.

Among the Core Based Statistical Areas (CBSAs) tracked by First American, the five markets with the greatest year-over-year increase in the RHPI included:

- Miami (+92.8%)

- Tampa, Florida (+81.4%)

- Indianapolis (+79.4%)

- Jacksonville, Florida (+77.1%)

- Nashville, Tennessee (+75.9%)

Among the Core Based Statistical Areas (CBSAs) tracked by First American, there were no markets with a year-over-year decrease in the RHPI.