HouseCanary, Inc. [1] has released its December Market Pulse Report [2], showing that activity in terms of net new listings placed on the market is up 5% versus December 2022.

With the Federal Reserve keeping rates steady in December and mortgage rates dropping slightly, affordability has marginally improved. As a result, the market saw the first signs of positive activity in terms of both net new listings and properties under contract. Cooling inflation and anticipated rate cuts this year signal that further positive momentum is to come. However, given that inventory remains at historically low levels, sales growth is expected to be gradual and modest.

“The slight increase in December listings indicates the impact of lower mortgage rates is beginning to trickle down into the market, which comes as an optimistic sign as we head into the new year," said Jeremy Sicklick, Co-Founder and CEO of HouseCanary. "With that said, any market turns are likely to be slow. The mortgage rate lock-in effect is going to keep many would-be sellers who secured pre-pandemic mortgage rates of sub-5% with little incentive to move, meaning low inventory will be a continuing trend. As we enter the year ahead, promising signs that the Federal Reserve will cut rates persist, which will provide at least some relief for homebuyers looking to purchase in 2024.”

Key Takeaways:

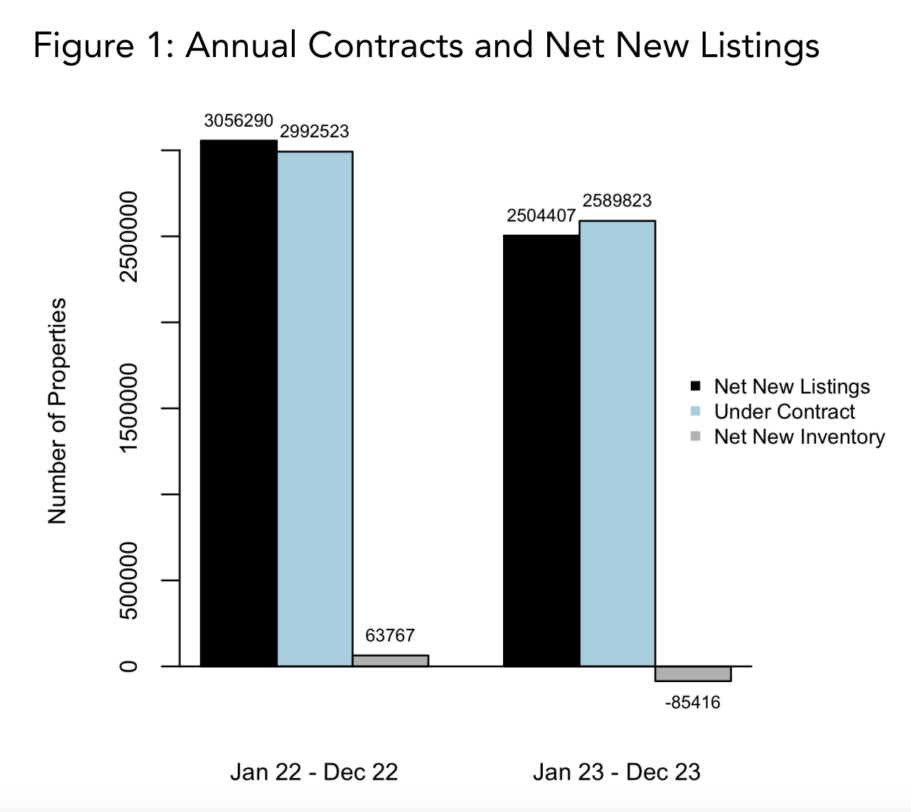

- Over the last 52 weeks, 2,504,407 net new listings were placed on the market, and 2,589,823 properties went under contract. This represents a decrease of 18.1% and 13.5%, respectively, versus 2022.

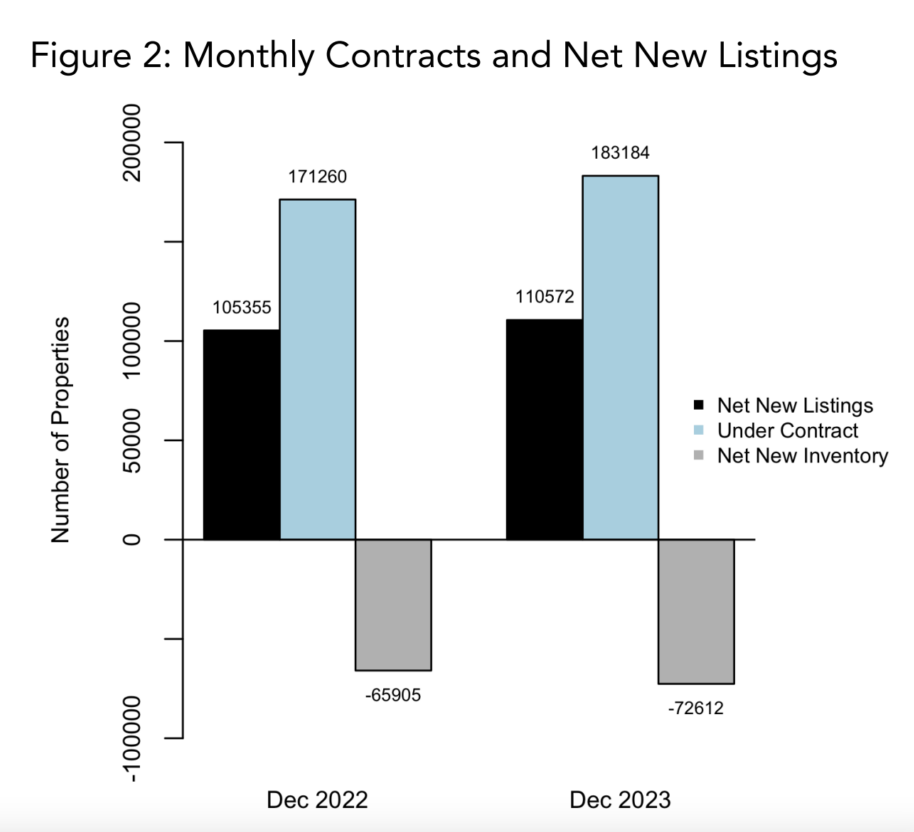

- For the month of December 2023, 110,572 net new listings were placed on the market, and 183,184 properties went under contract. This represents an increase of 5.0% and 7.0%, respectively, versus December 2022.

- The increase in net new listings was driven by a 0.8% decrease in new listing volume that was offset by a larger 9.5% decrease in removals compared to December 2022.

- Median days on market is at 51 days. This is down 5.6% from where it was one year prior, at 54 days on market.

- The median price of all single-family listings in the US was $424,729, and the median closed price was $394,223. On a year-over-year basis, the median price of all single-family listings is up 3.1%, and the median price of closed listings is up 5.6%.

- Month-over-month, the median price of single-family listings is down 1.2%, and the median price of closed listings is down 0.5%.

Contract Volume and Net New Listing Volume

Over the last 52 weeks, 2,504,407 net new listings were placed on the market, and 2,589,823 properties went under contract. This represents a decrease of 18.1% and 13.5%, respectively. For the month of December 2023, 110,572 net new listings were placed on the market, and 183,184 properties went under contract. This represents an increase of 5.0% and 7.0%, respectively, versus December 2022.

The increase in net new listings was driven by a 0.8% decrease in new listing volume that was offset by a larger 9.5% decrease in removals compared to December 2022.

The interest rate shock is having the biggest impact on net new listing volume which remains sharply down year-over-year. Contract volume is also down year-over-year, but not as much. Net new listing and contract volume are trending at multi-year seasonal lows. Total inventory is up 12.1% from the same period in 2022, and up 24.5% from 2021. Inventory remains very low from a historical perspective.

Contract Volume and Net New Listing Volume by Price Tier

- Contract volume in December 2023 is up across all price tiers compared to December 2022.

- Net new listing volume in December 2023 is down for the two lower price tiers and up for the three price tiers above $400k compared to December 2022.

- The total volume of listings going into contract over the last 52 weeks are down across all price bins compared to the year prior.

- The total volume of net new listings over the last 52 weeks are down across all price bins compared to the year prior.

Single Family Price Activity

The median price of all single-family listings in the US was $424,729 and the median closed price was $394,223. On a year-over-year basis, the median price of all single-family listings is up 3.1% and the median price of closed listings is up 5.6%. Month-over-month, the median price of single-family listings is down 1.2% and the median price of closed listings is down 0.5%.

The median price-per-sqft of all listed single-family homes in the US sits at $222.3 and the median closed price-per-sqft was $220.8. On a year-over-year basis, the median price-per-sqft of all listed single-family homes is up 2.7% and the median price-per-sqft of closed listings is up 6.6%. Month-over-month, the median price-per-sqft of all listed single-family homes is down 1.3% and the median price-per-sqft of closed listings is down 1.0%.

The sale-to-list-price ratio stands at 97.9% which is well above the lowest value observed in January 2023. Price cuts are down 6.4% compared to the same time last year.

The median price of all single-family rental listings in the US was $2,531. On a year-over-year basis, the median price of all single-family rental listings is up 3.1%. Month-over-month, the median price of single-family rental listings is down 0.3%. Total single family rental inventory is up 31.3% from the same period in 2022, and up 141.1% from 2021.

To read the full report, including more data, charts, and methodology, click here [2].