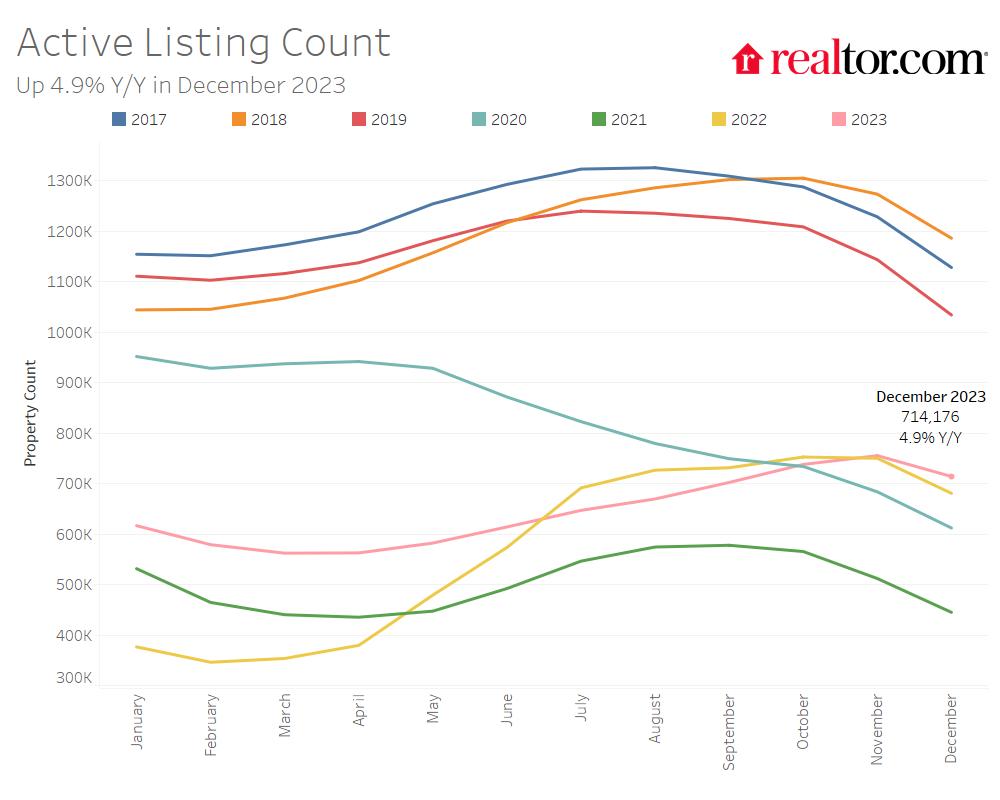

According to Realtor.com's [1]December Monthly Housing Trends Report, home shoppers are experiencing broader housing options and a larger number of unsold homes on the market for the first time since last May.

While the report found that mortgage rates have been on a downward trend since the beginning of November, Realtor.com experts anticipate a "positive impact" on home-selling sentiment and the strong possibility that additional listings will enter the market in 2024.

Key Findings from the December Monthly Housing Trends Report:

- The number of homes actively for sale was notably higher compared to last year, growing by 4.9%.

- The total number of unsold homes, including homes that are under contract, increased by 3.6% compared to last year.

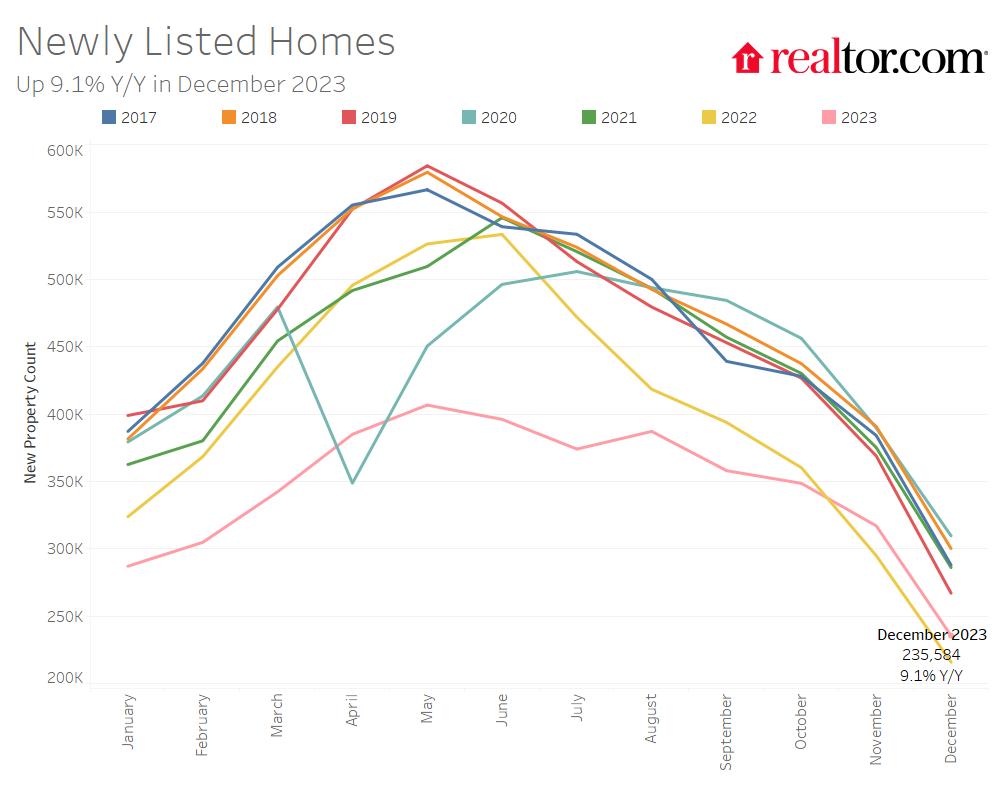

- Home sellers were more active this December, with 9.1% more newly listed homes compared to last year.

- The median price of homes for sale this December remained relatively stable compared to the same time last year, growing by 1.2%.

- Homes spent 61 days on the market, which is four days shorter than last year and about two weeks shorter than before the COVID-19 pandemic.

While homebuyers typically avoid big moves during the December holiday season—unless they absolutely must sell or buy—this results in different real estate activity than what is experienced during the peak summer season.

Although the market is still not where it was pre-pandemic and active inventory sits 34.3% below typical 2017–2019 levels, in December 2023, home sellers were active, with 9.1% more newly listed homes compared to last year.

The month-over-month change between November and December experienced a decline in inventory that has historically hovered between 6.8% and 13.2%. This year, there was a more modest 5.5% decrease, indicating a significantly smaller than typical drop for this time of year.

"Across the U.S., we're seeing improvements in inventory levels, especially in the South, which experienced a 7.7% increase in active listings year-over-year," said Danielle Hale, Chief Economist at Realtor.com. "While the uptick in December inventory levels is encouraging, it is important to note that two-thirds of outstanding mortgages in the U.S. have a rate under 4% and more than 90% have a rate less than 6%."

Listing Prices Remain "Relatively Stable" Compared to Last Year

The national median list price declined seasonally, to $410,000 from $420,000 in November, and the median list price remained relatively stable compared to the same time last year, growing by 1.2%, according to the report. Listing prices have since been buoyed by scarce inventory, and while new home sales have been increasing, construction activity isn’t elevated enough to fully bridge the low inventory gap.

While the median listing price has remained relatively stable relative to last year, higher mortgage rates compared to last December increased the monthly cost of financing 80% of the typical home by roughly $123 (+6.1%) compared to a year ago. This increased the required household income to purchase the median-priced home by $4,900 to $85,664, before accounting for the cost of tax and insurance.

"We are optimistic that inventory levels are moving in a positive direction, but the number of homes on the market is still low relative to pre-pandemic levels," said Hale. "Some sellers are clearly motivated already, but other households may hold out for lower rates before selling or moving to new homes."

To read the full report, including more data, charts, and methodology, click here [1].