DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Last year, the House Financial Services Committee held a series of hearings to examine the impact of Dodd-Frank on Americans during the fifth anniversary of the highly controversial Wall Street Reform legislation.

Last year, the House Financial Services Committee held a series of hearings to examine the impact of Dodd-Frank on Americans during the fifth anniversary of the highly controversial Wall Street Reform legislation.

The Committee has long held that the massive 2,300-page Dodd-Frank Act has brought on heavy compliance burdens that make it tougher on community banks and credit unions to offer the same level of service to customers that they had prior to the existence of the law. In addition, the Committee says it is tougher for creditworthy Americans to buy a home than it was prior to Dodd-Frank; indeed, they estimate that one in five borrowers who purchased a home with a mortgage in 2010 would not qualify under Dodd-Frank’s current underwriting rules.

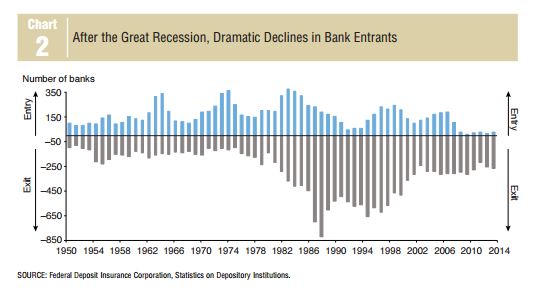

As more evidence that the effects of Dodd-Frank have been more harmful than helpful to businesses on Main Street, the Committee presented two recently-published reports this week: One from the Federal Reserve Bank of Dallas and a non-partisan study from the Government Accountability Office (GAO).

The Dallas Fed report concluded that many community financial institutions may be “too small to succeed” in the era of the “regulatory onslaught” brought on by Dodd-Frank. The report pointed out that community banks, despite seeing a decline in market share down to about 19 percent of $15.9 trillion in total assets, still hold about 55 percent of small business loans and 75 percent of agricultural loans.

“Notwithstanding the benefits community banks bring to the economy, practically no new banks have entered the market since 2008,” the Dallas Fed stated in the report.

The report also spoke of the increasing compliance burden for banks, saying that “the playing field is becoming more uneven.”

“Banks of all sizes and complexities have to hire compliance personnel to properly align their institutions with these new regulations,” the Dallas Fed stated. “But for smaller institutions, the compliance burden is likely greater.”

“Banks of all sizes and complexities have to hire compliance personnel to properly align their institutions with these new regulations,” the Dallas Fed stated. “But for smaller institutions, the compliance burden is likely greater.”

The nonpartisan GAO’s report also indicated an “increased compliance burden” to community banks and credit unions, and that burden has “begun to adversely affect some lending activities,” such as mortgage lending to customers who would not typically be served by the larger banks. Not only that, but the GAO stated that “The full impact of the Dodd-Frank Act remains uncertain because many of its rules have yet to be implemented and insufficient time has passed to evaluate others.”

The Credit Union National Association (CUNA) issued a statement on the GAO's report, saying “It is our hope that Congress will thoroughly investigate the costs of regulatory burden as the full picture unfolds and more regulatory requirements become effective.”

The House Financial Services Committee stated in its release that it is working to try to reverse the adverse effects of Dodd-Frank on Main Street.

“In 2015, 28 Committee bills were signed into law, including six dealing with Dodd-Frank,” the Committee reported. “In 2016, we’ll be working to present proposals laying out a better vision for financial reform—bold ideas that promote more opportunities for low and moderate-income Americans, protect taxpayers from future Wall Street bailouts, and empower families and individuals to achieve financial independence.”