DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

CoreLogic has released its monthly Loan Performance Insights Report for October 2021, showing nationwide mortgage rates and the effects of delinquency.

CoreLogic has released its monthly Loan Performance Insights Report for October 2021, showing nationwide mortgage rates and the effects of delinquency.

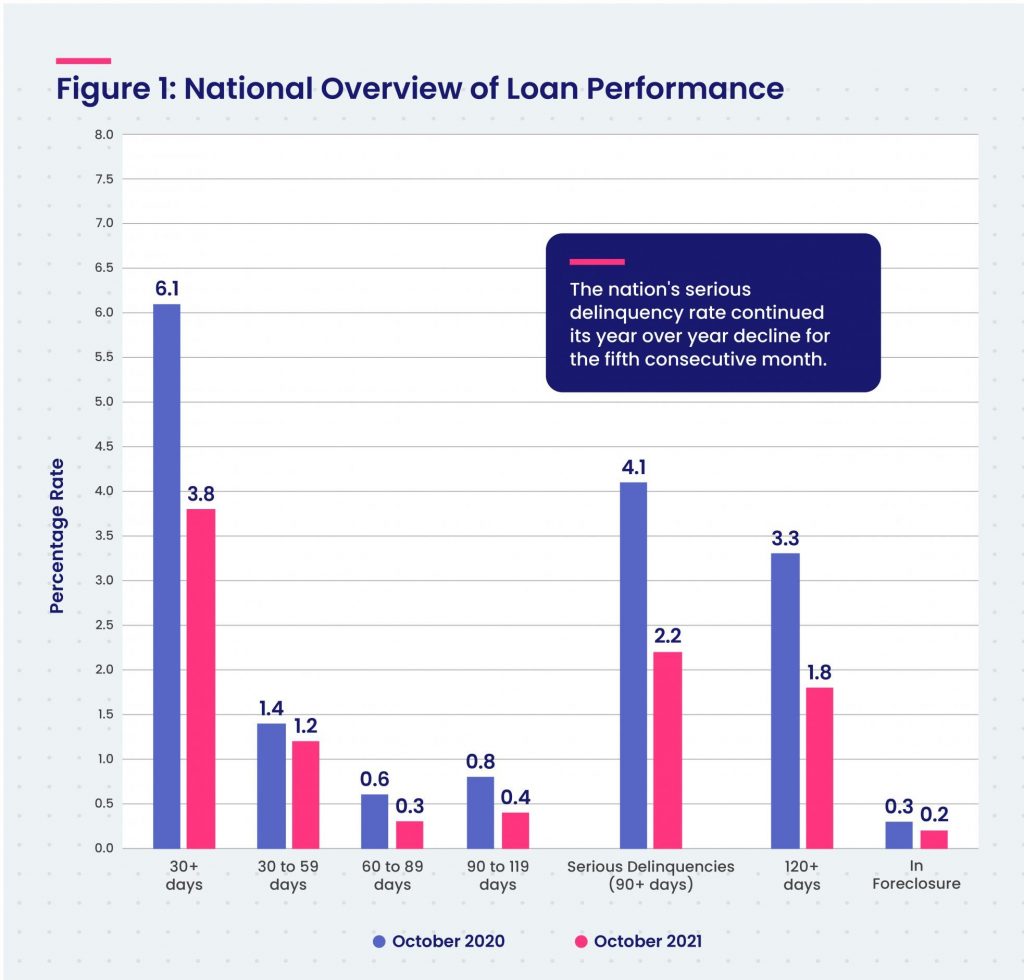

The solutions provider examines all stages of delinquency, as shown in the full report. In October 2021, the U.S. delinquency and transition rates, and their year-over-year changes, were, according to the report:

- Early-stage Delinquencies (30 to 59 days past due): 1.2%, down from 1.4% in October 2020.

- Adverse Delinquency (60 to 89 days past due): 0.3%, down from 0.6% in October 2020.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 2.2%, down from 4.1% in October 2020.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.2%, down from 0.3% in October 2020. This remains the lowest foreclosure rate recorded since 1999.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.7%, down from 0.8% in October 2020.

For the month of October, 3.8% of all mortgages in the U.S. were in some stage of delinquency, representing a 2.3% point decrease compared to October 2020, where it was 6.1%.

For the month of October, 3.8% of all mortgages in the U.S. were in some stage of delinquency, representing a 2.3% point decrease compared to October 2020, where it was 6.1%.

“Economic recovery and loan modification have helped reduce the number of loans that were in serious delinquency by just over one million from the August 2021 peak,” said Dr. Frank Nothaft, Chief Economist at CoreLogic. “Nonetheless, there were about one-half million more loans in serious delinquency in October than at the start of the pandemic in March 2020.”

After over a year of trying conditions for borrowers, unemployment rates mark an improvement as data from the Bureau of Labor Statistics shows that by October 2021 an estimated 82% of the jobs lost in March and April 2020 were recovered, which translates to roughly 18.2 million Americans back at work. The combination of significant job market improvement, home equity increases, and federal assistance programs have helped overall delinquency rates decline to 3.8%, which is close to the October 2019 rate of 3.7%.

“Improving economic security and the benefits of disciplined underwriting practices over the past decade are helping reduce or avoid mortgage delinquencies,” said Frank Martell, President and CEO of CoreLogic. “We expect to see delinquency trend down over the balance of this year as the economy continues to rebound from the pandemic, employment grows and high levels of fiscal and monetary stimulus continues.”

In October 2021, all states logged year-over-year declines in their overall delinquency rate. The states with the largest declines were: Nevada, Hawaii, and Florida, all down 3.5 percentage points.

All except two U.S. metros posted at least a small annual decrease in their overall delinquency rate. The two areas with annual increases in October 2021 were Louisiana cities Houma-Thibodaux, up 3.4 percentage points, and Hammond, up 0.2 percentage points.

The next CoreLogic Loan Performance Insights Report will be released on February 8, 2022, featuring data for November 2021. For more housing trends and data, visit the CoreLogic Intelligence Blog here.