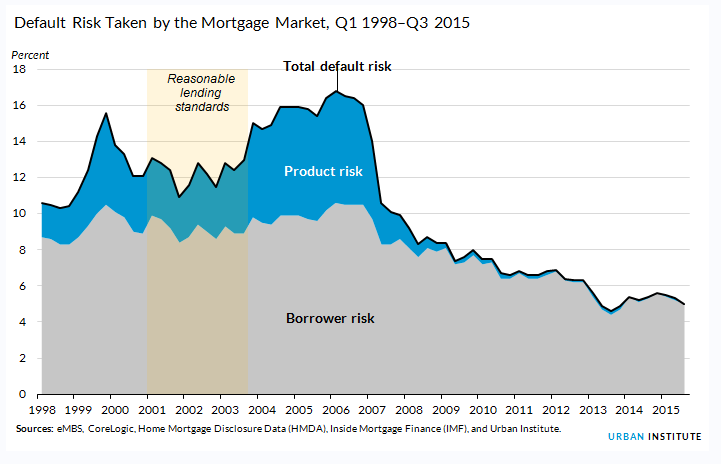

[1]According to the Urban Institute Housing Policy Finance Center’s latest credit availability index (HCAI) [2], which is a measure of the percentage of home purchase loans that are likely to default, home purchase loans became less risky over the third quarter of 2015 as lenders have become less willing to tolerate defaults, continuing a trend from over the last four quarters.

[1]According to the Urban Institute Housing Policy Finance Center’s latest credit availability index (HCAI) [2], which is a measure of the percentage of home purchase loans that are likely to default, home purchase loans became less risky over the third quarter of 2015 as lenders have become less willing to tolerate defaults, continuing a trend from over the last four quarters.

The HCAI dropped from 5.3 in Q2 down to 5.0 in Q3 2015, drawing closer to the record low of 4.6 from the third quarter of 2013. A lower HCAI indicates that lenders have imposed tighter lending standards due to an unwillingness to tolerate defaults, and therefore mortgage credit access is tighter; a higher HCAI indicates that lenders are willing to tolerate more risks and have looser lending standards, thus making mortgage credit more available.

Mortgage credit availability in the GSE channel, which includes Fannie Mae and Freddie Mac, has expanded at a faster rate than the government (FVR) channel recently. Since the second quarter of 2011, when the downward trend of mortgage credit availability in the GSE channel reversed, the total risk taken in that channel has leaped from 1.4 percent to 2.1 percent—an increase of 50 percent.

For the government channel (FVR), comprised of the Federal Housing Administration, the Department of Veterans Affairs, and the Department of Agriculture Rural Development Program, mortgage credit availability has gone in the opposite direction. The risk of default that the government loan channel was willing to take on was reported at 9.8 percent in Q3 2015. While still slightly above its record low of 9.6 set in 2013, the last four quarters have seen a decrease in credit availability in the FVR channel.

[3]The total default risk for the portfolio and private-label securities (PP) channel for Q3 2015, which was reported at 2.4 percent, matching its record low, although this market took much higher product risk than the FVR and GSE channels during the housing bubble.

[3]The total default risk for the portfolio and private-label securities (PP) channel for Q3 2015, which was reported at 2.4 percent, matching its record low, although this market took much higher product risk than the FVR and GSE channels during the housing bubble.

The decline in overall HCAI from Q2 to Q3 from 5.3 to 5.0 means that mortgage credit quality has improved. Two reasons are responsible for this, according to Housing Policy Finance Center senior research associate Wei Li.

“On the supply side, lenders could be taking less default risk than the previous quarter when they originate loans, either through stricter underwriting standards or through offering less risky product,” Li said. “On the demand side, there could be more high-quality borrowers applying for mortgages than low-quality borrowers; or same group of borrowers demand more safe loan products than risky products.”

Overall, researchers determined based on the HCAI that mortgage credit availability is very tight.

“Significant space remains to safely expand the credit box,” the report stated. “If the current default risk was doubled across all channels, risk would still be well within the precrisis standard of 12.5 percent in 2001–03 for the whole mortgage market.”