DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Closing out 2022’s housing market potential data, the year ended on a two-month upswing, increasing 3% over November. Despite this increase, housing market potential remained down 17% compared with year-end data from December 2021.

Closing out 2022’s housing market potential data, the year ended on a two-month upswing, increasing 3% over November. Despite this increase, housing market potential remained down 17% compared with year-end data from December 2021.

This news comes by way of Mark Fleming, the Chief Economist for First American Financial Corporation and Leader of the Decision Sciences team, who overall found that the 17% drop in potential from 2021 is the equivalent to 1,065,000 sales that did not happen.

“The steep annual decline in market potential was largely a result of higher mortgage rates, which prevent both buyers and sellers from jumping into the market,” said Fleming. “While rates remain significantly higher compared with one year ago, they have retreated for two consecutive months, improving affordability. However, although lower mortgage rates have helped improve affordability, housing supply remains limited, and you can’t buy what’s not for sale.”

Compared to November 2022, the average 30-year fixed rate mortgage dropped 0.5%, boosting home-buying power by $16,000, equivalent to an increase of 87,000 home sales. Year-over-year, home-buying power is down $141,000 based on current figures.

Mortgage applications, which are a leading indicator of home sales, have also increased over the last two months as mortgage rates have softened.

“From a financial perspective, the decision to buy a home comes down to a payment-to-paycheck calculation, and lower rates may help to reduce the mortgage payment while higher incomes can increase one’s monthly paycheck,” Fleming said.

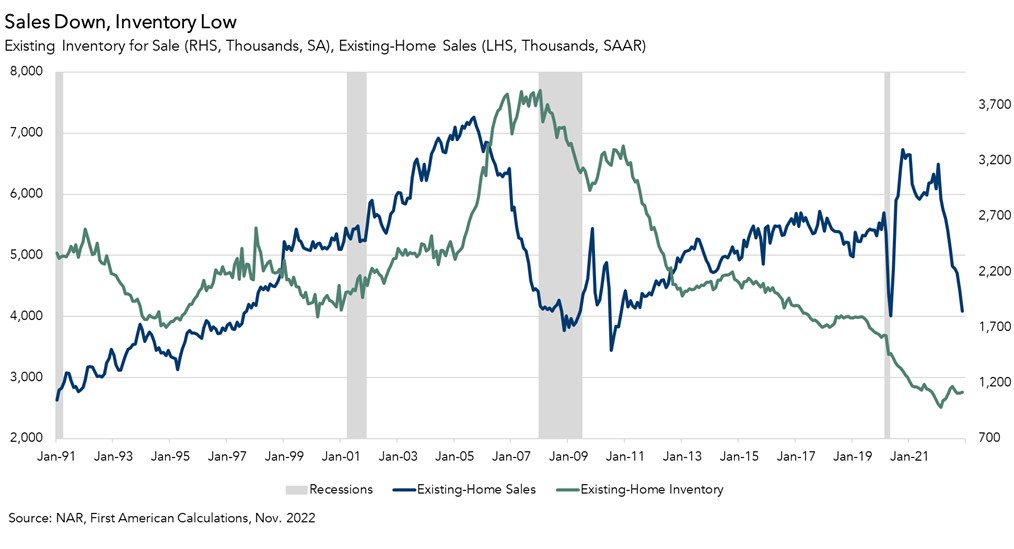

The markets limiting reagent seems to inventory, which is still down historically, and buyers' fear of not finding something to buy. As of the third quarter of 2022, 93% of outstanding mortgages have a rate at or below 6%, leaving existing homeowners in a position where it would cost more to borrow the same amount of money they owe on their current mortgage, preventing them from listing their home for sale and adding supply to the market.

As a result of these dynamics, the average length of time that homeowners remain in their home reached a historic high of 10.62 years in December, reducing housing market potential by 9,600 sales compared to the previous month.

“While existing-home inventory remains limited, the silver lining for home buyers is that new-home inventory is on the rise, and a new home at the right price is a pretty good substitute,” said Fleming. “The National Association of Home Builders reported that nearly two-thirds of builders were offering incentives, including mortgage rate buydowns, paying points for buyers and price reductions, which could entice potential home buyers.”

The good news is that new-home inventory is on the rise, as is usual to see in the spring season, which will continue to prop up sales numbers.

Click here to see Fleming’s thoughts in their entirety.