DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

The Federal Housing Administration (FHA)’s Mutual Mortgage Insurance (MMI) Fund, Home Equity Conversion Mortgage (HECM) program, and the Agency’s mission were the focal points in Principal Deputy Assistant Secretary Edward Golding’s testimony before the House Subcommittee on Housing and Insurance on Thursday.

The Federal Housing Administration (FHA)’s Mutual Mortgage Insurance (MMI) Fund, Home Equity Conversion Mortgage (HECM) program, and the Agency’s mission were the focal points in Principal Deputy Assistant Secretary Edward Golding’s testimony before the House Subcommittee on Housing and Insurance on Thursday.

The hearing, titled “The Future of Housing in America: Examining the Health of the Federal Housing Administration,” was the sixth on the topic in the House Subcommittee on Housing and Industry during the 114th Congress.

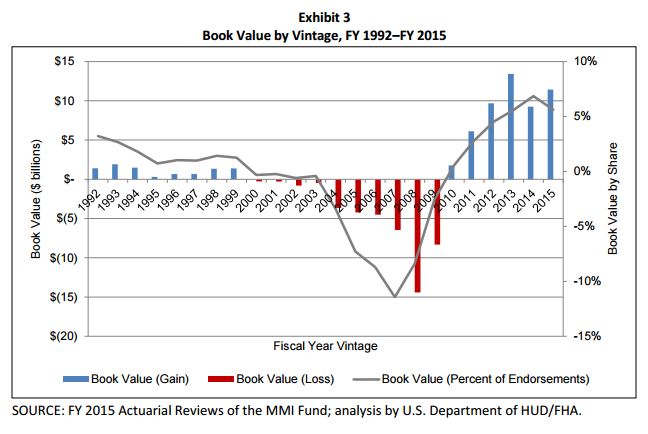

The capital ratio of the MMI Fund sat at 0.41 percent, less than a quarter of its 2 percent minimum required by Congress, for Fiscal Year 2014. For FY 2015, that number shot up to 2.07 percent, even after the FHA took some heat for lowering the MMI premium by 50 basis points in January 2015.

“FHA’s Mutual Mortgage Insurance Fund bore the strain of the Great Recession, falling below its required capital reserve and eventually taking a mandatory appropriation in 2013,” Golding said in his testimony on Thursday. “However, FHA’s focus on risk management, increasing revenue, and program improvements resulted in the ratio returning to 2 percent in 2015. This achievement was the result of FHA’s prudent policy changes, and an ability to work with Congress to pass stabilizing legislation and quickly implement program changes over the course of several years.”

Citing a 14 percent year-over-year spike in building permits and an 11 percent increase in housing starts over-the-year in 2015, along with the recent announcement that the unemployment rate had dipped below 5 percent, Golding said stated that “FHA’s position is strong and continues to improve. FHA remains committed to its mission to address underserved borrowers and mortgage markets.”

Edward Golding

House Subcommittee on Housing an Insurance Chairman Blaine Luetkemeyer (R-Missouri) was skeptical, however. Luetkemeyer claimed that while the FHA’s mission has historically focused on first-time homebuyers and creditworthy low- and moderate-income buyers, “FHA has morphed from a mortgage insurer of last resort to a dominant component of our mortgage finance system by expanding its insurance to higher income borrowers and houses in the upper end of the marketplace.”

Luetkemeyer stated that “FHA has suffered a case of mission creep, and the unfortunate truth is that the lack of sound underwriting and risk management puts both homebuyers and U.S. taxpayers at risk. While the most recent independent actuarial report showed signs of a modestly healthier agency, the bottom line is that FHA is still in a precarious state.”

Golding defended against the assertion that the FHA’s mission had drifted away from its original intention, noting that 82 percent of all FHA purchase originations in FY2015 were to first-time homebuyers (totaling more than 614,000 loans).

“With its low down-payment requirement, FHA has served as a pathway to homeownership for first-time homebuyers,” Golding said. “This has been especially true in recent years, as credit restrictions and higher financing costs have impeded many potential borrowers, including those that would previously have been served by the conventional market.”

The Subcommittee called the FHA’s efforts to solve its fiscal problems by lowering the mortgage insurance premiums “misguided and counterproductive” because they believe it places taxpayers at risk of more bailouts, underprices risk and results in the FHA suffering more losses, and discourages private investor involvement in mortgage finance.

The Subcommittee called the FHA’s efforts to solve its fiscal problems by lowering the mortgage insurance premiums “misguided and counterproductive” because they believe it places taxpayers at risk of more bailouts, underprices risk and results in the FHA suffering more losses, and discourages private investor involvement in mortgage finance.

Golding defended the lowering of the premium, stating that “FHA’s decision to reduce premiums created the opportunity for more than 100,000 families to become homeowners and further bolster our nation’s housing market.”

On the FHA’s HECM portfolio, which was the main driver of pushing the MMI Fund capital ratio above 2 percent, Golding stated that “FHA feels that it has effectively responded to the programmatic issues affecting the loan level performance of HECM. Improvements like the provision of greater lender flexibility to use loss mitigation for eligible borrowers, limiting the amount of money that can be taken from the property, and removing riskier HECM product options, appear to have proven useful in reducing losses to the Fund.”

Click here to read Golding’s full testimony.