DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

The risk on Agency first-time buyer mortgages is rising while the disparity in risk between Agency first-time buyers and repeat buyers is growing wider, according to the AEI International Center on Housing Risk’s First-Time Buyer Mortgage Risk Index (FBMRI) for January 2016 released Monday.

The risk on Agency first-time buyer mortgages is rising while the disparity in risk between Agency first-time buyers and repeat buyers is growing wider, according to the AEI International Center on Housing Risk’s First-Time Buyer Mortgage Risk Index (FBMRI) for January 2016 released Monday.

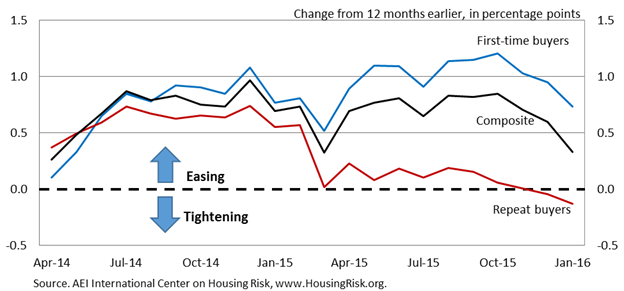

The Agency FBMRI provides an estimate of the share of Agency first-time buyer mortgages that would default if the economy were to suffer adverse conditions similar to those during the 2007 and 2008 financial crisis. In January 2016, the FBMRI increased over-the-year by 0.7 percentage points up to 15.7 percent and is 6 percentage points higher than the Agency risk index for repeat buyers. The gap between the two continues to grow wider, according to AEI.

More than half (54 percent) of first-time buyer loans in January were high risk, meaning they had an MRI higher than 12 percent. That share jumped by 2 percentage points over-the-year, up from 52 percent in January 2015.

Risk layering is largely responsible for the higher risk for first-time buyer mortgages, according to AEI. In January, 70 percent of first-time buyer mortgages had a combined LTV ratio of 95 percent or higher and 97 percent of the mortgages had a 30-year term. The combination of a low down payment and slow amortization assures that these first-time buyers will have little equity for many years, barring substantial home price appreciation.

“The gap between first-time buyer and repeat buyer mortgage risk levels now stands at 5.92 percentage points compared to 4.91 and 4.64 percentage points in December 2014 and 2013 respectively,” said Edward Pinto, codirector of the AEI International Center on Housing Risk. “In a seller’s market, risk layering artificially pushes up prices, particularly for entry-level buyers; the result is a wealth transfer from buyers to sellers of these homes.”

Another contributor to riskier first-time buyer mortgages is the fact that one-fifth of first-time buyers had a credit score lower than 660, which is the traditional definition of subprime mortgages. Also, one-fourth of first-time buyers had total DTI ratios higher than 43 percent, which is the limit set by the Qualified Mortgage rule.

Mortgages taken out by repeat buyers were less risky because a much smaller share of repeat buyers had a CLTV higher than 95 percent, and a smaller share of repeat buyers had a FICO score lower than 660.

Mortgages taken out by repeat buyers were less risky because a much smaller share of repeat buyers had a CLTV higher than 95 percent, and a smaller share of repeat buyers had a FICO score lower than 660.

The Agency First-Time Buyer Share Index (FBMSI), which measures the percentage of primary owner-occupied home purchase mortgages with a government guarantee, increased by only 0.1 percentage points over the year in January, from 56.0 percent to 56.1 percent. AEI attributes this largely to delayed closings brought on by the TRID rule, which went into effect on October 3, 2015.

“On a year-over-year basis, the first-time buyer share increased only modestly in January, with the rise likely suppressed by the implementation of TRID,” Pinto said. “Once this impact abates we expect the housing market, particularly at the entry-level, to exhibit strong demand, in combination with shortness of supply, which will continue to drive home prices up faster than incomes and inflation.”