The payment shock facing homeowners who originated a Home Equity Lines of Credit (HELOCs) between 2004 and 2007, known as legacy HELOCs shock once they reach the end of their 10-year draw period might not be as big a problem as originally thought, according to a white paper titled “Home Equity Lending Landscape [1]” issued by CoreLogic [2] on Monday.

The payment shock facing homeowners who originated a Home Equity Lines of Credit (HELOCs) between 2004 and 2007, known as legacy HELOCs shock once they reach the end of their 10-year draw period might not be as big a problem as originally thought, according to a white paper titled “Home Equity Lending Landscape [1]” issued by CoreLogic [2] on Monday.

The mortgage industry originated approximately 12.2 million HELOCs during the three-year-period between 2004 and 2007, often with loose underwriting standards. Some in the industry have expressed concern [3] that a large number of borrowers with legacy HELOCs will default because they cannot handle the payment shock that awaits them when they reach their end-of-draw period, which is the point at which borrowers must start repaying their balances with fully amortized payments (as opposed to interest-only) and cannot borrow funds from their lines of credit any longer.

Many of the riskiest legacy HELOCs issued during those housing bubble years have defaulted and gone into foreclosure, but millions of those HELOCs remain active, according to CoreLogic.

About 39 percent of the 4.1 million residential homes that had negative equity, or were “underwater,” as of Q3 2015 had both first and second liens (computing to about 1.6 million properties). The average mortgage balance on those properties was $307,000, and they were underwater by an average amount of about $83,000. By comparison, borrowers with only first liens were underwater by an average of about $58,000, CoreLogic reported.

Despite warnings that the HELOCs reaching the end-of-draw period could potentially result in another round of losses, the problem may be under control.

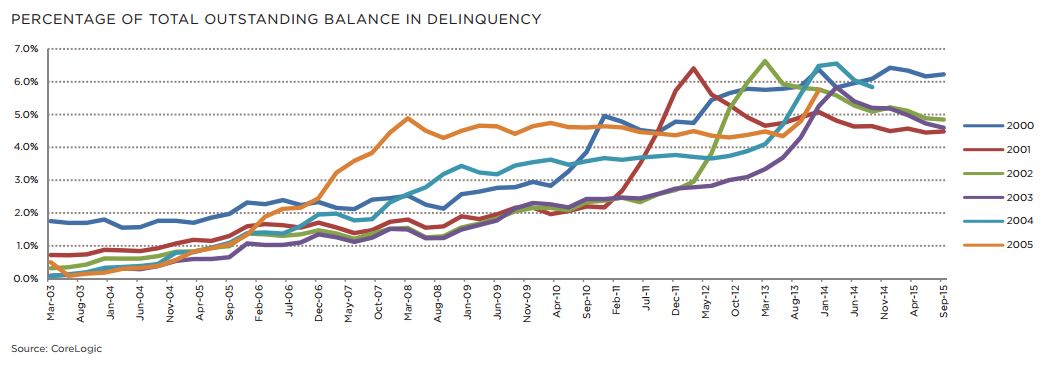

“While there has been some increase in late payments and delinquencies tied to conversions, so far the problem appears to be manageable,” the white paper stated. “The average monthly delinquency rate (30+ days overdue) for HELOCs was 2.0 percent in 2015 through November—the lowest level in eight years.”

Many lenders have been proactive about offering legacy HELOC borrowers options to refinance that will allow them to continue the interest-only payments, and many older HELOCs have been extinguished by first mortgage refinances that incorporated the outstanding HELOC debt, according to CoreLogic.

“As a result, the number of active legacy HELOCs has significantly declined,” CoreLogic stated in the paper. “Having said that, the smaller cohort of active legacy HELOCs that haven’t been refinanced because of equity, credit, or income issues will be very susceptible to default in the event of a payment shock.”

Click here [1] to see the complete white paper.