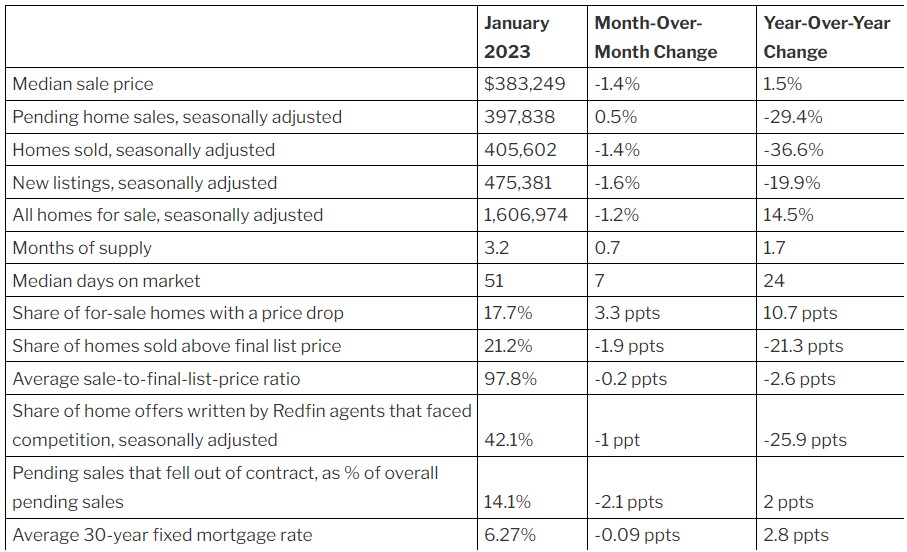

January’s Housing Market Tracker, as published by Redfin [1], suggests that any recovery the housing market may have found over the month was hampered by still-high real estate prices and depressed inventory levels as pending home sales rose by 0.5% from December 2022.

January’s Housing Market Tracker, as published by Redfin [1], suggests that any recovery the housing market may have found over the month was hampered by still-high real estate prices and depressed inventory levels as pending home sales rose by 0.5% from December 2022.

That compares with December's month-over-month increase of 1.4%, which was the first gain in 14 months. On a yearly basis, pending sales declined for the second month in a row—to 29.4% in January from 32.5% in December and a record 35.5% drop in November.

“A dip in mortgage rates brought some buyers off the bench in January, but the housing-market recovery was tempered by still-high housing costs and a limited number of homes being listed for sale,” said Redfin Deputy Chief Economist Taylor Marr [2]. “There were fewer new listings in January than at any point on record, with the exception of the start of the pandemic. That hampered demand because it meant that many of the buyers who were still in the market had a tough time finding a home that met their needs. The shortage of homes for sale also buoyed home prices.”

Marr continued: “The housing market took two steps forward in December and January, but has taken one step back in February. Mortgage rates crept back up this month, which is prompting more buyers and sellers to back off.”

Purchase applications have also fallen to their lowest level since 1995 after comments from the Federal Reserve cemented expectations that they will raise the nominal interest rate at their next meeting to further combat inflation, which has been a thorn in the side of the economy for some time now.

The average 30-year-fixed mortgage rate is now 6.5%, up from an average of 6.27% in January and 3.89% a year ago. That has caused the typical homebuyer’s monthly payment to rise more than $500 year over year.

In addition, closed home sales fell 1.4% from December 2022 and have nosedived by 36.6% year-over-year. The large drop in closed sales is partly due to the fact that many of the home purchases that closed in January went under contract in the fall, when mortgage rates hit a 20-year high.

Due to the “lock-in” effect where homeowners with low interest rates stay put instead of moving in fear of higher rates, new listings fell in January by 1.6% from December and 19.9% year-over-year. While this number is an improvement from December’s 25.3% year-over-year decline, listings still remain scarce. There were fewer new listings in January than any other month on record aside from April 2020, when the onset of the pandemic froze the housing market. About 85% of mortgage holders have a rate far below today’s level of roughly 6%.

The median sale price of U.S. homes was $383,249 in January, down 1.4% from December and 11.5% below the May all-time high. Still, prices were up 1.5% from a year earlier, in part because low supply kept prices afloat.

“Nice homes that are priced fairly are selling, but homes that are overpriced or poorly maintained are lingering on the market,” said Shay Stein [3], a Redfin real estate agent in the Las Vegas area. “A lot of sellers who don’t get the price they had hoped for are taking their homes off the market. Many of them have a rock-bottom mortgage rate and figure they can wait to sell.” 30-

Finally, the typical home in January was on the market for 51 days, the highest level since right the pandemic hit in February 2020. This number is up from 27 days a year ago. Bidding wars were also less common during the month as 42.1% of properties sold by Redfin, a number which is down 43.1% a month earlier and from 68% a year ago.

Click here [4] to view Redfin’s data in its entirety.