DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

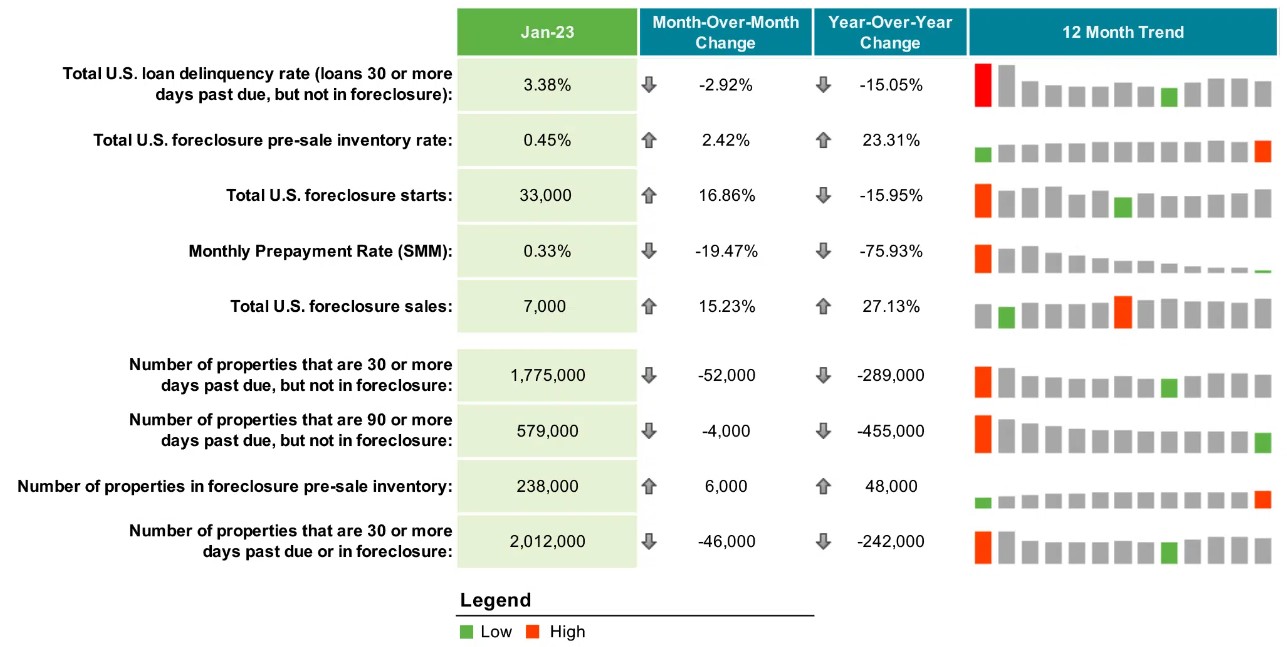

Due to a better-than-expected jobs market, loan performance data in January 2023 showed a 10 basis point decrease in the national delinquency rate from December 2022 and 15.1% year-over-year.

Due to a better-than-expected jobs market, loan performance data in January 2023 showed a 10 basis point decrease in the national delinquency rate from December 2022 and 15.1% year-over-year.

In addition, foreclosure starts saw another month of increases, but still remain 37% below pre-pandemic levels. Active foreclosures are up 20% since January 2022, but they too remain nearly 20% below pre-pandemic levels.

This data comes from Black Knight Inc. as part of their “first look” at January’s month-end loan performance report which covers 60% of active mortgages across the country.

As mentioned earlier, delinquencies were down across the board falling to 3.38% of homeowners' month-over-month, and down 15.1% year-over-year.

The number of borrowers 30-days late decreased by 46,000 (-4.8%), while 60-day delinquencies also ticked down slightly. Serious delinquencies, or those 90+ days past due, continued to improve nationally (-4,000), with such inventories declining in a large majority (44) of states. Florida—still dealing with the aftermath of Hurricane Ian—saw another 1.7K loans fall into serious delinquency.

But for the fourth month, foreclosure starts rose 17% to 33,000 loans, but even this number is down 37% below pre-pandemic levels. Foreclosure was started on 5.6% of serious delinquencies in January, some 48% below January 2020’s start rate. Active foreclosure inventory rose by 2.5% in the month, and is now up 48K or 20% since January 2022, but remains nearly 20% below pre-pandemic levels. A total of 7K foreclosures were completed nationally in January, up 15.2% from the month prior, but remain nearly 50% below early 2020 levels.

“Given the fundamental changes we’ve seen in the market’s makeup—even before the pandemic—and as the industry and wider economy move ahead into an uncertain future, this additional visibility couldn’t come at a more important time,” said Ben Graboske, President of Black Knight Data & Analytics. “Our role as a public provider of objective and unvarnished housing and mortgage market data and analysis is something we take very seriously. We’ve been through enough boom-and-bust cycles in the mortgage industry to understand just how critical this role is—to our industry, as well to the public, the media and the wider American economy.”