DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Banks have retreated somewhat from mortgage servicing in the last six years because they have been the focus of post-crisis financial reforms, even though both banks and nonbanks were underregulated and undercapitalized before the crisis.

Banks have retreated somewhat from mortgage servicing in the last six years because they have been the focus of post-crisis financial reforms, even though both banks and nonbanks were underregulated and undercapitalized before the crisis.

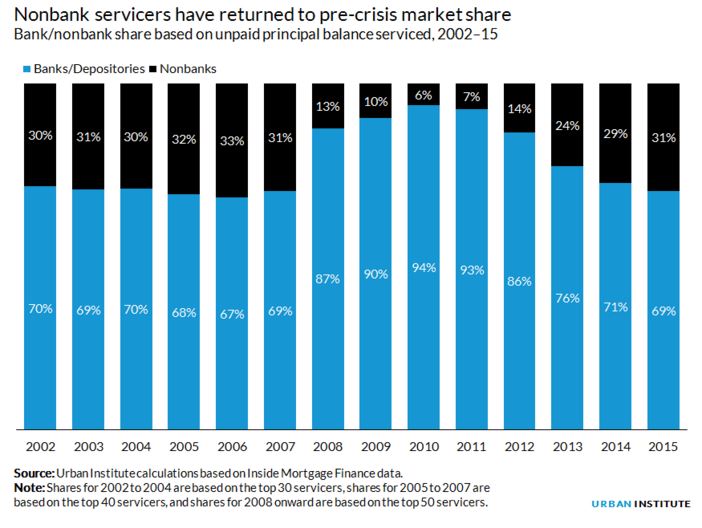

The retreat of banks from mortgage servicing has allowed nonbank institutions have regained their market share in the mortgage servicing space that they lost in the aftermath of the crisis; that share was historically 30 percent, but shrank to 6 percent in 2010 as banks became more involved in mortgage servicing. Nonbank servicers face unique risks that banks do not; their failure is borne by borrowers, government agencies, and taxpayers, which is why the government should raise capital requirements for nonbank servicers to reduce risk to these entities and pass more of it on to the industry, according to a commentary titled “Nonbank Regulation Remains Unfinished Business from the Housing Crisis” by Karan Kaul and Laurie Goodman of the Urban Institute on Friday.

Fannie Mae, Freddie Mac, and Ginnie Mae have all recently increased capital requirements for nonbank servicers, but it’s not enough, according to Kaul and Goodman in a brief on Friday titled “Nonbank Servicer Regulation: New Capital and Liquidity Requirements Don’t Offer Enough Loss Protection.” The requirements may be sufficient for a low-risk and stable interest rate environment, but may not be if interest rates become volatile or if defaults rise, according to Kaul and Goodman.

Among the unique risks nonbank servicers face are, according to the authors:

- Heavy exposure to mortgage servicing rights (MSRs), which is a “highly volatile asset class.” According to analysis from Urban Institute, less than one percent of total assets in banks are comprised of MSRs; for nonbanks, that percentage rises to between 10 and 35 percent for nonbanks.

- MSRs are a hard-to-value asset not actively traded in an open liquid market. Pricing is model dependent and prone to assumptions, therefore creating additional price volatility.

- If delinquencies rise rapidly, the requirement to remit payment to investors can cause significant liquidity crunch

The authors expressed concern of the recent new minimum capital and liquidity requirements issued by the GSEs and Ginnie Mae, namely: the requirements are not risk-based and are left up to the judgment of management; existing regulation relies on ongoing monitoring to detect problems, and while the authors said they support this, financial stress can often set in quickly, which leaves little or no time for remedial action; and when regulators transfer MSRs from an insolvent servicer to a financially stable servicer, they often do so in a panic, thus maximizing the proceeds and finding a buyer quickly often take priority over quality.

“Perhaps most importantly, if there is not enough buyer interest in acquiring a for-sale servicing portfolio, or bid prices are low, Ginnie Mae and the GSEs may have to pay the new servicer to pick up the loans, putting taxpayers at risk,” the authors wrote.

With taxpayers on the hook to bear the losses when nonbank servicers fail, the authors contend that more regulation is needed, namely raising capital requirements for nonbank servicers.

“We urge the GSEs and Ginnie Mae to revisit this topic to strike a healthier balance between nonbank capital requirements and ensuring a well-functioning industry that works for borrowers, investors and taxpayers, in both good times and bad,” Kaul and Goodman wrote.