DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

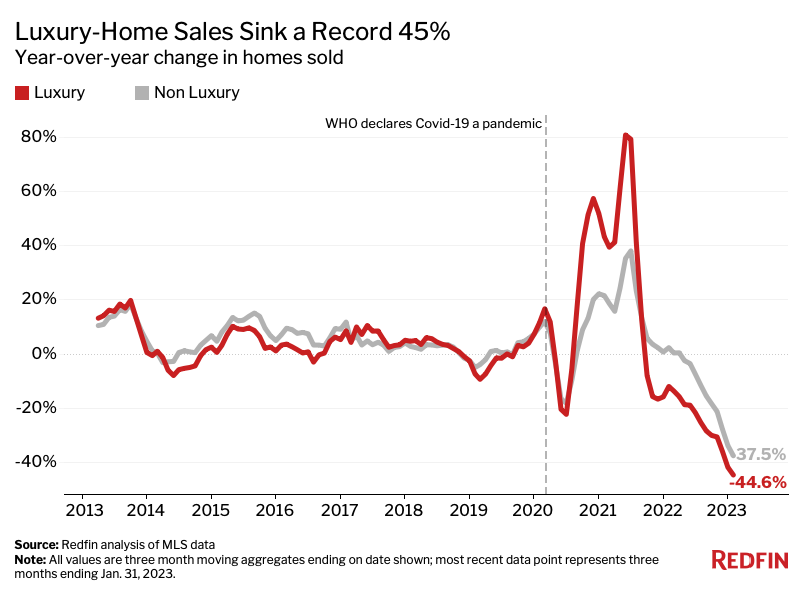

Based on the definition that a “luxury” home is a home in the top 5% of homes based on market value, Redfin has found that the sale of these high value homes declined by a record 44.6% to its second lowest level on record during the three-month period ending January 31, 2023.

Based on the definition that a “luxury” home is a home in the top 5% of homes based on market value, Redfin has found that the sale of these high value homes declined by a record 44.6% to its second lowest level on record during the three-month period ending January 31, 2023.

This number also surpassed the record 37.5% drop in sales of non-luxury homes over the same period with statistics dating back to 2012.

According to Redfin, the housing market has cooled significantly over the last year due to elevated mortgage rates, persistently high home prices, ongoing inflation and a shaky economy, but the luxury market has fallen relatively quickly because:

- People tend to purchase fewer expensive goods during times of economic uncertainty.

- Luxury home sales grew faster than non luxury sales during the pandemic, so they now have more room to fall (see chart above).

- A higher mortgage rate makes homebuying more expensive for nearly everyone, but it can add tens of thousands of dollars to the price tag on a luxury home, giving high-end buyers sticker shock.

- Wealthy homebuyers often have a lot of money in the stock market, which had a turbulent start to 2023 following its worst year since 2008.

- Many wealthy Americans are choosing to invest in assets other than real estate because elevated mortgage rates and softening housing prices have cast a shadow over prospective real estate returns.

“Uncertainty is the main factor driving the luxury-market slowdown in Los Angeles,” said Alin Glogovicean, a local Redfin Premier real estate agent. “If you’re investing millions in a property, you want to make sure it will hold its value. Most luxury buyers and sellers are thinking, ‘Let’s just wait and see what happens to the market. When it stabilizes, we’ll be ready to go.’ Everyone is kind of at a standstill.”

“The silver lining for the luxury buyers who are still in the market is that competition is sparse and jumbo loans now often have lower mortgage rates than other loan types, in part because there’s less risk that high-end buyers will default on their mortgages,” said Redfin Economics Research Lead Chen Zhao. “Wealthy house hunters are also frequently offered additional rate discounts from their banks as a perk for storing substantial funds there.”

Zhao continued: “Luxury homebuyers should still shop around for the best mortgage rate possible. Research shows that when rates are high, so is the variance in rates between lenders. That’s why it’s smart to request quotes from several lenders and then ask your favorite lender to match the lowest rate.”

The median sale price of luxury homes rose 9% year over year to $1.09 million during the three months ending Jan. 31. While that’s roughly half the year-over-year gain of a year earlier, luxury prices remain near the all-time high of $1.1 million reached in spring 2022.

However, supply is just shy of its all-time low, which occurred about this time last year.

Click here to view Redfin’s research in its entirety.