According to University Financial Associates [1] (UFA) mortgage default risk numbers of late are rising, but should still be manageable by lenders and servicers in the grand scheme of things due to the better quality of loans that have been issued since the Great Recession.

According to University Financial Associates [1] (UFA) mortgage default risk numbers of late are rising, but should still be manageable by lenders and servicers in the grand scheme of things due to the better quality of loans that have been issued since the Great Recession.

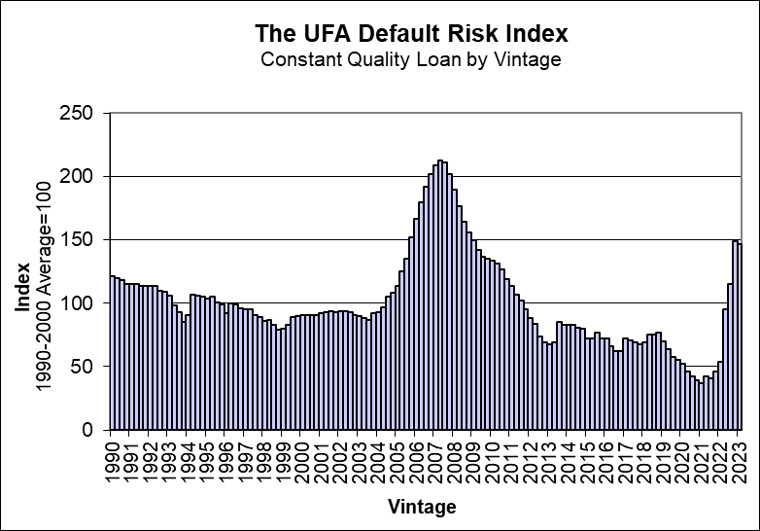

In their latest index report, UFA found the came in at a score of 147 for the first quarter of 2023—lenders and investors should expect defaults on loans originated in the first quarter to be 47% higher than the average of similar loans originated in the 90s due solely to the local and national economic environment. The index was initially benchmarked to 100 in 2003.

“With prices beginning to decline in selected metro areas and many more to follow over the next couple years, mortgage lenders and investors will have to tighten underwriting standards and increase selectivity until house prices bottom,” said Dennis Capozza, who is Professor Emeritus of Finance in the Ross School of Business at the University of Michigan, and a founding principal of UFA. “Mortgages rates have more than doubled in the last year while house prices have increased at double digit rates since the pandemic making home ownership much less affordable.”

“To date delinquencies remain very low. Most homeowners have gained considerable equity as prices have risen and if stressed can sell to realize that equity rather than default,” Capozza continued. “UFA does not expect a ‘nuclear winter for housing’ as some observers are expecting. Current economic conditions are much better positioned than in the Great Recession.”

“Although house prices have risen very fast in response to pandemic driven demand, the excesses of the prior cycle are not present. Permits and stats remain well below the prior peak levels,” Capozza concluded. “Demand remains high with many homeowners needing to adjust housing consumption due to changes arising from the pandemic and technological innovations like work from home.”

Click here [2] to view the report in its entirety.