DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

A combination of factors including rapid inflation, interest rate hikes, high home prices, and increased costs of living are pushing many renters to reconsider their housing options, according to a new report from RentCafe.

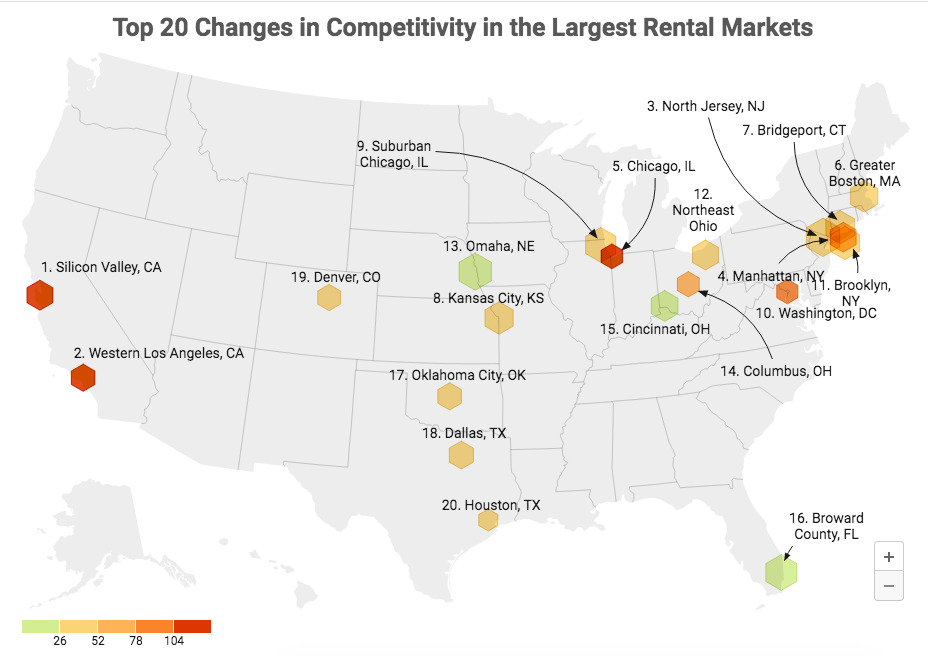

Sunbelt states have long been highly coveted renting spots, particularly during the pandemic. However, the start of 2023 saw a pivot to markets located in the Northeast. As a result, eight of the country’s top 20 hottest renting spots are in the Northeast.

Aspiring homebuyers continue to rent in North Jersey while enjoying a relatively affordable cost of living for the tri-state area. This allows renters to save for down payments until the housing market cools down enough that they can fulfill their dream of owning a home. Accordingly, North Jersey became the hottest renting spot in the country at the beginning of 2023.

But what were the most in-demand renting spots at the start of 2023? To rank the nation’s most competitive rental markets, RentCafe.com analyzed the 134 largest markets in the U.S. where data was available. For this, we looked at the most revealing metrics when it came to competitivity, including:

- the number of days apartments were vacant

- the percentage of apartments that were occupied by renters

- the number of prospective renters competing for an apartment

- the percentage of renters who renewed their leases

- the share of new apartments completed

Then, to see how competitive the rental market was as the year began to unfold, we calculated a Rental Competitivity Index (RCI). At the beginning of 2023, the national RCI score was 60, which indicates a moderately competitive rental market.

The overall housing supply can’t keep up with demand

As the new year began, vacant U.S. apartments were occupied within 38 days, on average, with 8 prospective renters competing for each available apartment amid an occupancy rate of 94.2%. At the same time, 60.7% of apartment dwellers renewed their leases. Plus, with the number of newly opened apartments accounting for an extremely modest 0.43% of the nation’s housing supply, finding a new place to call home can become challenging this time of the year.

By comparison, one year ago, vacant apartments were filled almost one week faster and there were three more people applying for the same rental. This was especially significant because more renters (64.7%) chose to renew their leases and newly built apartments represented only 0.75% of the total apartments in the U.S. These factors then led to 95.6% of apartments being occupied at this time last year.

Unsurprisingly, renters continue to face intense competition in some of last year’s hottest markets in Florida — including Miami, Southwest Florida and Orlando —where a high number of new apartments were completed, but not enough to meet demand.

As a matter of fact, apartment construction dwindled in almost all markets compared to the start of 2022. Looking at the top 20 hottest rental markets in the U.S., only Milwaukee, WI, and Central New Jersey saw the pace of construction pick up as 2023 was starting to unfold.

Almost half of the country’s red-hot rental markets are in the Northeast

North Jersey is the country’s hottest rental market, with an RCI score of 115. Encompassing more laid back, affordable places like Jersey City and Newark, renters here are just across the bridge from the hustle and bustle of Manhattan, so they get to enjoy the best of both worlds.

Plus, in recent years, North Jersey has turned into a desirable location for well-heeled renters looking for nicer apartments, more elbow room and a better work/life balance while still being close to the Big Apple’s attractions. Namely, between 2015 and 2020, high-income households earning more than $150,000 per year increased by 151% in Newark and by 75% in Jersey City.

For this reason, finding an apartment for rent in this popular part of New Jersey is no easy task these days. Here, the severe shortage of housing (newly opened apartments accounted for only 0.27% at the beginning of the year) and an influx of newcomers —mostly transplants from gateway cities— pushed North Jersey’s occupancy rate to a high 96.6%.

As if the lack of new apartments weren’t enough of a hassle for would-be renters, 72.2% of apartment dwellers in North Jersey also chose to renew their leases, thereby putting even more pressure on the rental market. As a result, at the beginning of the year, it took 34 days for the average vacant apartment in North Jersey to become occupied, with 12 prospective renters competing for the same available unit.

Competition builds up in undersupplied renter hubs on the East Coast, including Brooklyn, NY and Boston

Speaking of the lack of new apartments, Brooklyn, NY, (RCI score 86) is an interesting example. Coming in 14th in our ranking, this desirable borough of New York City has been consistently welcoming transplants from all around the country, including many renters priced out of Manhattan. These newcomers —along with the existing renters— are willing to compete for the limited number of apartments here just to get to live in the Big Apple, even with its high cost of living.

But, despite the fact that 2022 was a record year for new apartments built throughout New York City, housing in Brooklyn is far from meeting the pent-up demand: The number of newly opened apartments added just 0.3% to what was available on the market — and it wasn't enough to lower the occupancy rate. On top of that, more than two-thirds of Brooklynites renewed their leases. So, the average vacant apartment in Brooklyn attracts about 9 prospective renters and gets filled within 43 days.

Claiming 19th place (RCI score 76), Boston paints a similar picture when it comes to renting. After more than two and a half years of escaping the city’s crammed apartments and high cost of living, softening pandemic restrictions allowed workers to return to the office and students to go back to in-person classes at Boston’s many colleges and universities. Combined with high home prices and very few newly built apartments, this added even more pressure on The Hub’s housing scene. That said, 95.3% of all apartments for rent in Boston were occupied at the start of 2023, especially as 60.9% of renters chose not to move. Consequently, a vacant unit in Boston is typically occupied within 38 days, with 10 renters competing to secure a lease.

On the other side of the country, Orange County and San Diego are neck and neck for the hottest rental market in California. Their RCI scores of 89 and 87, respectively, reflect occupancy rates of just above 96%. That's because zero apartments were opened recently in these markets and because more than half of apartment dwellers renewed their leases in both markets. So, vacant apartments in Orange County are filled after 39 days, with 11 people applying for each available unit. Similarly, the competition is slightly tighter in San Diego, where 13 prospects fight for each available unit and vacant rentals are occupied faster (after 34 days, on average).

Florida’s well-known hotspots for renting haven’t lost their appeal

Year after year, waves of people flock to Florida —a trend that has only grown stronger since early 2020 when record-high numbers of newcomers headed to the Sunshine State seeking a combination of a laid-back lifestyle and a lower cost of living. That said, it’s no surprise that many Florida locations that were red-hot in our previous rankings remain very competitive at the start of 2023.

To that end —and with an RCI score of 112— the nation’s second most competitive rental market is Miami, FL. Boasting a record-high occupancy of 97.1% (as well as a high lease renewal rate of 70.9%), the Magic City continues to attract Gen Z and Millennial workers seeking all the benefits Florida has to offer, including the friendly business climate and the absence of income tax.

On average, vacant apartments in Miami are filled within 33 days, with 20 would-be renters competing to secure a lease —the highest number of prospective renters per vacant unit in our overall ranking. That’s despite the 1.24% increase in new apartments at the start of 2023. Simply put, there are still not enough rentals in Miami to accommodate all of the apartment seekers.

Silicon Valley, Manhattan see spectacular shifts in competitivity since one year ago

When analyzing competitivity at the start of 2023, several shifts stood out on a year-over-year comparison. For example, Silicon Valley’s competitivity score grew by a staggering 46 points since the start of 2022 —from a modest 22 to a robust 68— placing it 27th in our overall ranking. Notably, the area’s impressive rise in popularity was mostly fueled by high home prices and a lack of new apartments as remote workers slowly return to tech-driven California cities like Palo Alto, Menlo Park, Cupertino, Sunnyvale and Mountain View. To top it all off, significantly fewer apartments opened throughout Silicon Valley compared to one year prior (due to a 2.1% drop in new construction year-over-year). Therefore, an average of 11 prospective renters competed for each vacant apartment, which was occupied within 35 days.

Next, Western Los Angeles County’s RCI score grew from 26 to 55 year-over-year as the area continued to struggle with a housing shortage (despite an 0.8% uptick in the total number of apartments) on top of the high cost of living. Granted, California’s hottest markets in the last couple of years —Orange County and East Los Angeles— remain competitive, although it takes longer for apartments to fill.

Likewise, Manhattan gained 27 competitivity points since the start of 2022, kickstarting 2023 with an RCI score of 67. With almost two-thirds of renters renewing their leases —largely due to the longstanding shortage of apartments combined with rising mortgage rates, as well as the tenant eviction rules initiated in 2019— Manhattan’s occupancy rate increased by 0.4% year-over-year to a strong 94.8%. This then led to more renters competing for one vacant apartment, although apartments remain vacant for longer periods of time.

To read the full report, including more charts, data and methodology, click here.