DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

As anyone who has bought a home knows, a mortgage payment has many different components that pay many different things—and these costs can be easily ignored, looked over, or just flat-out misunderstood by even the savviest buyers.

As anyone who has bought a home knows, a mortgage payment has many different components that pay many different things—and these costs can be easily ignored, looked over, or just flat-out misunderstood by even the savviest buyers.

Fannie Mae has released new research with the goal of revealing these costs, and through analysis, attempt to pull back the curtain to provide insights into the drivers of affordability—or the lack thereof.

This research is unique in the fact that it uses first-lien data directly from the Government Sponsored Enterprises (GSEs, Fannie Mae and Freddie Mac) and does not aggregate data from second-hand or self-reported sources. This information was then distilled down to show the exact user, mortgage, closing, and other homeownership costs to illustrate homeownership expenses during a typical ownership cycle.

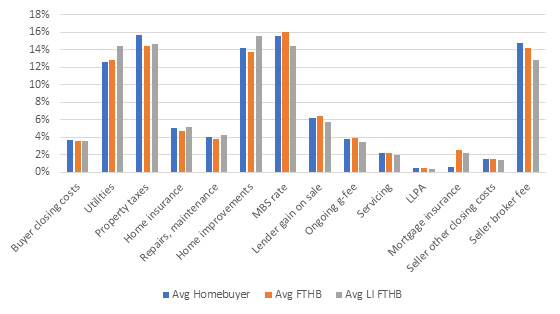

As a whole, the largest contributors to housing costs are surprisingly non-mortgage costs, which equaled roughly half of total borrower expenditures over the ownership period—these include utilities, property taxes, and home improvement, and maintenance expenses.

Transaction costs on either side of the purchase and sale of a home account for roughly 20% of total costs, with broker fees being the largest component of that.

Surprisingly, actual mortgage costs account for about 30% of the total cost of homeownership over the course of a typical mortgage, which the study pegged at seven years. These costs break down to monies paid to investors of mortgage-backed securities and the lender “gain-on-sale” or the one-time fee charged by the originator of the mortgage.

Guaranty fees charged by the GSEs account for about 4% of total costs, while private mortgage insurance ranges from 1-3%.

“While each homeowner’s total cost is different, of course, examining broad categories of homeowners and analyzing their costs, we believe, could provide insights into the drivers of housing affordability—or lack thereof,” said Jaclene Begley, an economist for Fannie Mae and author of the report. “The mechanics of mortgage costs may be difficult to understand in their particulars, but how those costs translate into actual consumer costs, and how those costs compare with other elements of total housing costs, paints a far more useful picture."

To do this Fannie Mae, using their own internal closing data, placed borrowers into one of three categories: all home purchasers, first-time homebuyers (FTHB), and low-income first-time homebuyers (LIFTHB).

In general, the average homebuyer is older, has a higher income, and purchases a more expensive home than FTHBs and LIFTHBs. In contrast, a low-income buyer has less than half the income of the average buyer and has the smallest average purchase price.

The findings were as follows:

- The report found that the average buyer is aged 42-years-old, has a monthly income of $9,377, and purchases a house at a price of $318,281 at a loan-to-value rate of 83%.

- The average FTHB is aged 36-years-old, has a monthly income of $7,453, and purchases a house at a price of $291,139 at a loan-to-value rate of 89%.

- The average LIFTHB is aged 35-years-old, has a monthly income of $4,161, and purchases a house at a price of $222,243, at a loan-to-value rate of 89%.

- For all three categories of borrowers, when broken down, most of the payments go toward five categories: utilities (12-14%); property taxes (14-16%); home improvements (14-16%); MBS rate (14-16%); and seller broker fees (12-15%).

“The takeaway? Borrowing is a big piece of the cost of owning a home, but that cost often is overshadowed by utilities, property taxes, home repairs, and one-time fees paid to various parties to buy and sell a home,” Begley concluded. "Why did we do this analysis? Because housing affordability is and will continue to be a matter of profound concern to homeowners and those who wish to own a home.

“Understanding the total cost picture can not only provide consumers better information to make decisions, but it can also offer mortgage and housing industry participants, housing advocates, and policymakers better tools as they seek to find ways to drive down the cost of homeownership—particularly for those eager to become first-time homeowners.”