The recent predictions from analysts of a dark year for housing based on tight inventory combined with rapid home price appreciation and slow wage growth may be a little off base, according to Freddie Mac [1]’s March 2016 Monthly Outlook [2] released Thursday.

The recent predictions from analysts of a dark year for housing based on tight inventory combined with rapid home price appreciation and slow wage growth may be a little off base, according to Freddie Mac [1]’s March 2016 Monthly Outlook [2] released Thursday.

Freddie Mac is predicting that housing fundamentals such as home sales, housing starts, and prices will all reach levels not seen since 2006, right in the middle of the housing bubble and two years before the crash.

“Housing markets are poised for their best year in a decade,” Freddie Mac Chief Economist Sean Becketti said. “In our latest forecast, total home sales, housing starts, and house prices will reach their highest levels since 2006. Low mortgage rates, robust job growth, and a gradual increase in housing supply will help drive housing markets forward. Low levels of inventory for-sale and for-rent and declining housing affordability will be major challenges, but on balance the nation's housing markets should sustain their momentum from 2015 into 2016 and 2017.”

The year 2016 will be a robust one for housing for several reasons, according to Freddie Mac. For starters, the 30-year mortgage rate average is expected to attract homebuyers in the spring and subsequently remain below 4 percent for the second half of the year. Slowing home price appreciation is also expected to contribute to greater affordability—whereas home prices rose by 6 percent year-over-year in 2015, that pace is expected to slow down to 4.8 percent for 2016.

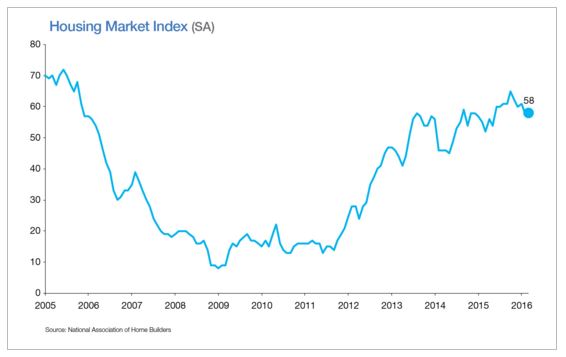

According to Freddie Mac, inventory, which has been cited by many industry analysts as a major hindrance to the housing market going forward is expected to pick up in 2016. Freddie Mac is predicting multi-family and single-family housing starts to increase this year by about 200,000, up to 1.3 million.

The labor force participation rate, which fell to nearly a four-decade low last year, is not expected to increase substantially from its current level, as recent analysis from Goldman Sachs [3] suggests. This could mean good news for wage growth, which took a backward step by declining three cents in February.

“If the labor force participation rate doesn’t increase and job gains maintain their recent pace, then pressures are going to build and wages will rise,” Freddie Mac stated in the report. “So far wage growth has been anemic, barely keeping pace with inflation. But if you look closely at the latest data on average hourly earnings you might convince yourself that we’re at the nascent stages of a gradual increase in wages. Wage growth ultimately will be a key factor for housing markets. If wages and incomes do not start rising, then rising interest rates, home prices, and rents will squeeze households and ultimately slow housing markets.”

“If the labor force participation rate doesn’t increase and job gains maintain their recent pace, then pressures are going to build and wages will rise,” Freddie Mac stated in the report. “So far wage growth has been anemic, barely keeping pace with inflation. But if you look closely at the latest data on average hourly earnings you might convince yourself that we’re at the nascent stages of a gradual increase in wages. Wage growth ultimately will be a key factor for housing markets. If wages and incomes do not start rising, then rising interest rates, home prices, and rents will squeeze households and ultimately slow housing markets.”

The predicted increase in wage growth combined with steady job growth should lead to an increase in household formations, according to Freddie Mac. The household formation rate has still not picked up enough after the Great Recession to match underlying population growth. In 2015, the household formation rate experienced a major dropoff from the first half of the year to the second; it reached 2.2 million on a year-over-year basis during the first half, but by the second half of the year, had declined to a rate of 800,000 per year.

“The drop-off in household formations could be an anomaly due to noisy data, or it could be a symptom of the lack of supply of housing,” Freddie Mac stated in the report. “Total annual housing completions have been running below 1 million for several years, and the vacancy rates are dropping. With low levels of supply there is nowhere for households to be formed. So despite robust job gains household formations haven’t followed yet.”