DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Appraisals can be a stressful process for any buying or selling a home and there are many reasons why an appraisal would be undervalued or overvalued. Water intrusion, cracks in foundations, or termites are all things that can tank an appraisal, but what if your race comes into play?

Appraisals can be a stressful process for any buying or selling a home and there are many reasons why an appraisal would be undervalued or overvalued. Water intrusion, cracks in foundations, or termites are all things that can tank an appraisal, but what if your race comes into play?

A recent analysis from Fannie Mae found that, of a sample size of 2 million borrowers, there were discrepancies in appraisal values received by Black and white borrowers who were in the process of refinancing their homes.

In order to close this racial disparity gap, Fannie Mae, and their industry partners, are “taking concrete actions” to make sure that appraisals are more fair going forward.

The method for pinpointing the value for a residential property has not changed much in decades, but the winds of change, which were only encouraged by COVID-19, have allowed for alternative methods of appraisal that may weed out bias risk that may be intentional or unintentional.

Jake Williamson, the SVP of Single-Family Collateral Risk Management for Fannie Mae, authored a report called “The Journey to a More Efficient and fair Home Valuation Process” which outlines some of the ways in which the industry can pivot to alternative methods of appraisals, such as appraisal waivers when refinancing a home.

“As an alternative, Fannie Mae offers appraisal waivers on some mortgage loans sold to us when we have enough information to feel confident in the property value estimate,” said Williamson. “Over the years, we've enhanced waiver offerings based on improvements in data digitization, analytical techniques, and data sources. But it has been ‘all or nothing’—the full traditional approach or no appraisal—with no in-between options.”

Williamson goes on to say that this “binary” approach to appraisals no longer fits today’s market and is “not consistent with how other mortgage risks are managed.”

“A far better approach is a spectrum of options to establish a property's market value, with the option matching the risk of the collateral and loan transaction,” Williamson said. “The spectrum balances traditional appraisals with appraisal alternatives. Options range from use of automated valuation models to validate the estimated property value, to collection of updated property data to confirm the model value, to alternative-scope approaches like desktop appraisals and hybrids, to a traditional appraisal.”

New ways of working support fair and impartial appraisals

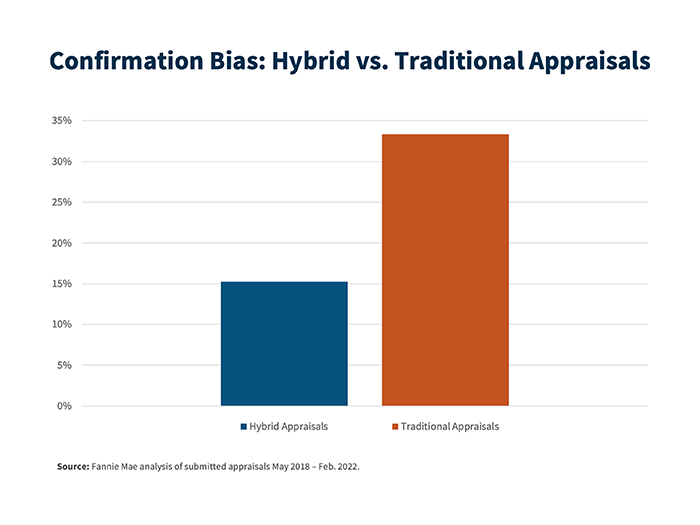

A traditional appraisal is reliant on human observations that can be skewed, consciously or unconsciously. Alternative-scope appraisals rely more heavily on objective data due to an arms-length process that separates the individual from the appraiser.

Appraisers can perform desktop appraisals using data from various parties such as real estate agents and public records, while hybrid appraisals use a neutral third party to visit the property and digitally submit their findings to an appraiser. Either choice reduces contact between borrowers and appraisers, lowering the likelihood that bias will affect the valuation of the property.

Alternative-scope appraisals, made possible by the magic of computers, are a powerful tool for “driving more factual, objective, accurate, and reproducible home valuations.”

Appraisal waivers saved mortgage borrowers $2 billion in two years

One way Fannie Mae is closing the appraisal disparity gap is by offering appraisal waivers. The waivers, which come through an automated underwriting system, are issued due to the GSE’s confidence in the estimated property value that was submitted by the lender and is consistent with expectations in the current market.

The waivers, which are mostly offered to refinances, can also be offered in rare cases to purchases, especially when borrowers are able to put down a large down payment.

Modern appraisal methods save time

Fannie Mae has been working with lenders, appraisers, and technology firms to test new and innovative ways to conduct appraisals for years now. In their tests, the right combination of lenders, borrowers, and vendors can save an average of five days by using an alternative appraisal method compared to a conventional one.

Modern appraisal methods are helping to fill the appraiser gap

Alternative appraisals are also providing relief to an aging appraiser workforce which is creating a shortage in many areas—especially rural ones.

Digital desktop appraisals allow appraisers to be more efficient, cutting out travel and inspection time.

Empowering appraisers

Even as more-and-more parts of the homebuying process go digital, even with increased reliance on automated valuation models and use of property data collectors, appraisers remain essential to the mortgage origination process. This is why Fannie Mae continues to invest in the Appraiser Diversity Initiative to find the next generation of appraisers.

“Improving the valuation process is changing the way appraisers work and empowering them with more career opportunities,” Williamson concluded. “Instead of spending much of their time scheduling appointments and driving to properties to collect information, appraisers can devote more time to doing what they are trained to do: analyze property data and form an expert opinion of value.”

“They can potentially increase their earnings by completing more appraisal reports in less time. And increasingly, appraisers can choose to work from home, accessing multiple online data sources along with property information collected or facilitated by other parties using technology such as 3-D scans, virtual inspection technology, and purpose-built mobile applications. Trained appraisers will also continue to have career opportunities supporting appraisal technology, such as helping to build and maintain property data collection mobile apps.”

While there is no clear-cut path to weeding out the bias in appraisals, but as with any journey targeting continuous improvement, it will take time. But hopefully the results will be worth the effort.