DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Investors with property loans issued before the housing crisis continue to see fewer defaults than those for owner-occupied properties, according to a report titled, "Lower Default Rates Offset Higher

Investors with property loans issued before the housing crisis continue to see fewer defaults than those for owner-occupied properties, according to a report titled, "Lower Default Rates Offset Higher

Liquidation Losses in Pre-Crisis Investor-Property

Loans" from Moody’s Investors Service.

The credit ratings agency released research Tuesday that suggested the rates would persist well into 2017.

“This trend will likely continue as long as the economy is growing and rental demand remains strong,” the report said. “[I]f the economy slows, investor loans will default at higher rates than owner-occupied loans with similar borrower characteristics, as they did during the 2007-09 economic downturn.”

Moody’s researchers chalked up the high rental demand to historically low rates of homeownership, steady household formations, and lingering consequences from the foreclosures and bankruptcies of the Great Recession.

The report said that several factors contribute to the continuing strong rental demand, such as:

- A historically low homeownership rate of just above 60 percent, a result of tight lending standards

- A steadily growing rate of household formation

- Adverse credit events (foreclosure, short sale, or bankruptcy) during crisis years that are still affecting the credit of many would-be buyers

Rental demand is essential to stability, with borrowers in financial trouble often resorting to renting out their properties to supplement income.

Rental demand is essential to stability, with borrowers in financial trouble often resorting to renting out their properties to supplement income.

“Owner-occupied loans experienced lower default rates during the 2007-09 downturn because owner-occupied borrowers had stronger incentives to keep current on their mortgages,” the researchers added.

They said that investors were also “more willing to walk away from their mortgages, especially if their rental income became insufficient to cover their mortgage payments.”

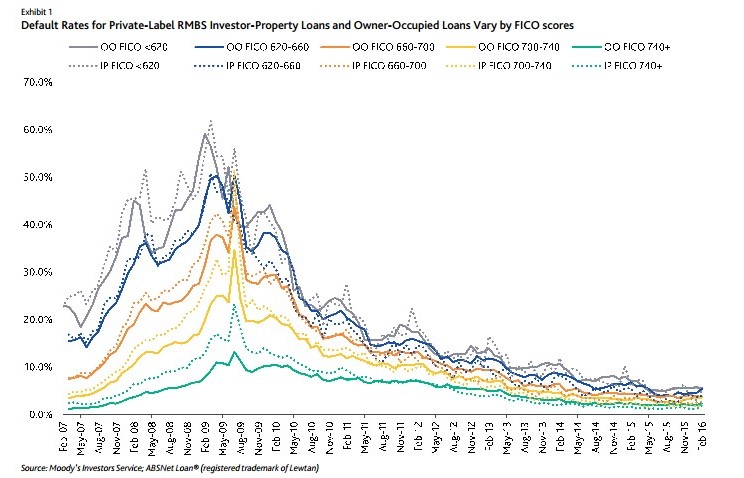

Even so, the losses for pre-crisis investor loans and owner-occupied property loans came to about the same, according to the researchers. This was because the severity and modification rates for defaults in investor loans surpassed those for owner-occupied property loans.

Default rates also tended to rise or fall in accordance with FICO scores.

Investor property loans with scores less than 620 had a higher probability of defaulting than those with scores on the upper end, although these rates have come down significantly from their historic highs over the last half decade and stabilized in February.

Click here to view the full report.