Due primarily to an upward revision in recent consumer spending data and bank failures in March, Fannie Mae's Economic and Strategic Research (ESR) Group [1] now forecasts stronger Q1 GDP growth but maintains its prediction that overall economic momentum is fatigued, according to the ESR Group's latest monthly commentary [2].

While mass panic following bank failures in March continue to subside, the banking turmoil occurred during an already-tightening credit cycle. The ESR Group now believes the incremental tightening in credit conditions from the financial fallout will contribute to a modest recession beginning in the second half of 2023.

"The economic slowdown has resumed – whether the end result is a modest recession or simply a soft landing remains unanswered – although we continue to expect the former, as we have since April of last year, when we first made our 2023 recession call," said Doug Duncan, Senior VP and Chief Economist, Fannie Mae. "The greater-than-expected resilience of the housing sector to the affordability pressures of higher home prices and mortgages rates is central to our expectation that the recession will be modest."

Key Takeaways:

- The Conference Board Leading Economic Index (LEI) declined 1.2% in March to 108.4. The index’s rate of decline is quickening as it fell 4.5 percent for the six-month period ending in March, compared to 3.5 percent the six months prior.

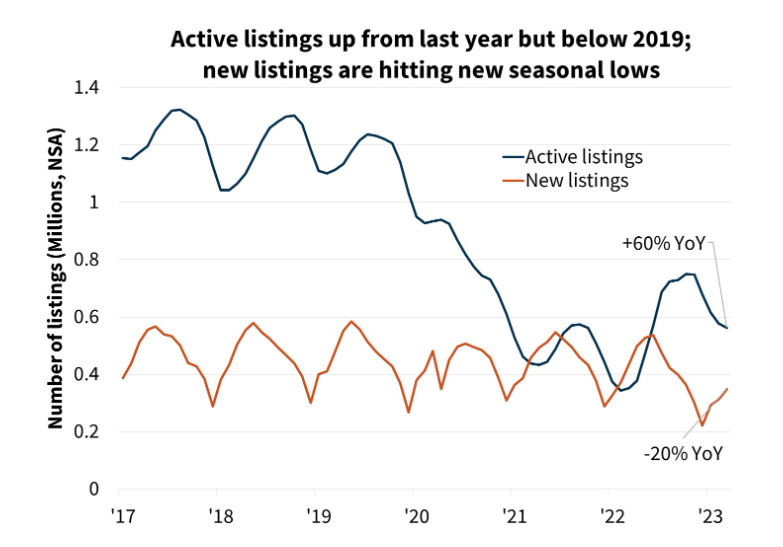

- Existing home sales declined 2.4% in March to a seasonally adjusted annualized rate (SAAR) of 4.44 million, according to the National Association of REALTORS [3]. For Q1, sales averaged an annualized pace of 4.33 million, an improvement of 3.2% compared to Q4 2022. In March, the inventory of homes for sales rose 1.0% to 980,000. The months’ supply was flat at 2.6, and the median sales price of existing homes declined 0.9% compared to a year ago.

- Housing starts declined 0.8% to a SAAR of 1.42 million in March, according to the Census Bureau. Single-family starts rose 2.7% to a SAAR of 861,000, while multifamily starts declined 5.9% (following gains of 9.4 and 16.2% in January and February, respectively) to a SAAR of 559,000. Single-family permits increased 4.1% to a SAAR of 818,000, continuing a trend of starts outpacing permits, though the two series have converged modestly over the past two months. Multifamily permits fell 22.1% to a still-strong SAAR of 595,000.

- The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index increased 1 point to 45 in April, its fourth consecutive monthly gain but the smallest increase in that period. The index for single-family sales in the present rose 2 points to 51, its first reading above 50 since September 2022, and the index for single-family sales in the next six months was up 3 points to 50.

Forecast Impact:

The further decline of the Leading Economic Index (LEI) in March remains supportive of Fannie Mae's call for a modest recession in the second half of 2023. With the initial bank panic subsiding and the small uptick in the economic coincident index, current indications are that the economy is not in a recession.

Existing home sales were approximately in line with Fannie Mae's Q1 expectations. The increase in the sales pace from the end of 2022 to the beginning of 2023 illustrates that homebuying demand remains resilient and was surprisingly responsive to small dips in mortgage rates. This resiliency is also reflected in the single-family starts report, which came in moderately above our forecast.

The supply of existing homes remains constrained both because of a decade of underbuilding following the Great Financial Crisis and, more recently, the “lock-in effect” discouraging current homeowners from listing their homes for sale due to not wanting to give up their low mortgage rates. As such, in light of an extremely limited supply of existing homes for sale, many homebuyers are turning to new homes. Still, with the generally more indicative single-family permits series continuing to trend below starts and our forecast for a modest recession beginning in the second half of this year, we expect further pullback in both new and existing home sales activity, though the new home market will likely continue to outperform relative to the existing market.

While housing demand and home prices have proved more resilient than previously anticipated, the ESR Group expects sales activity to remain subdued because of the persistently low inventory of homes for sale – particularly among existing homes. According to the ESR Group, this is due in large part to the "lock-in effect," in which existing homeowners are disincentivized from listing their homes and potentially giving up their lower mortgage rate. Still, strong demand for housing remains supportive of home prices; although the ESR Group notes significant regional variation in actual and expected home price movements.

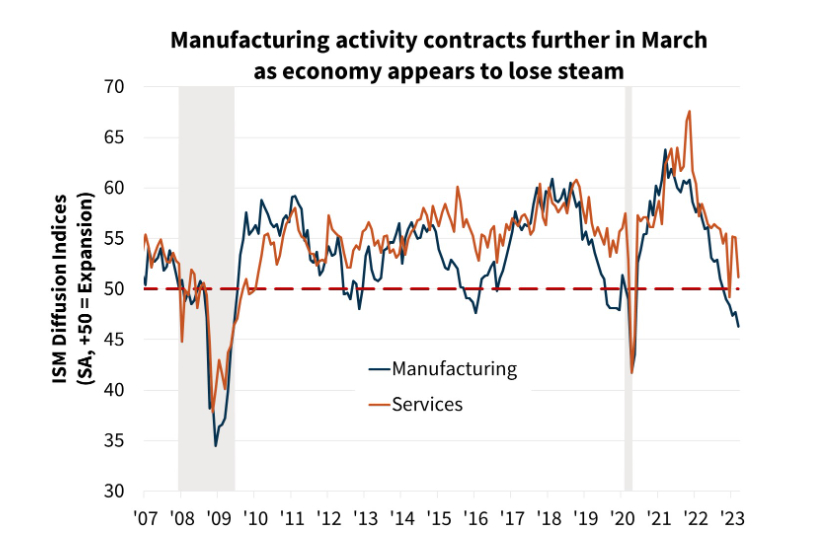

"In our view, while it would be premature to expect no further difficulties in the banking sector other than credit tightening, we're maintaining our baseline expectation of a modest recession, as we see signs of a weakening employment market, slowing retail sales, and declining manufacturing activity," said Duncan. "However, the rapid response of hopeful homeowners to periodic declines in mortgage rates, even from the currently higher rates, gives us additional confidence in our use of the word 'modest.'"

To read the full report, including more data, charts and methodology, click here [2].