DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

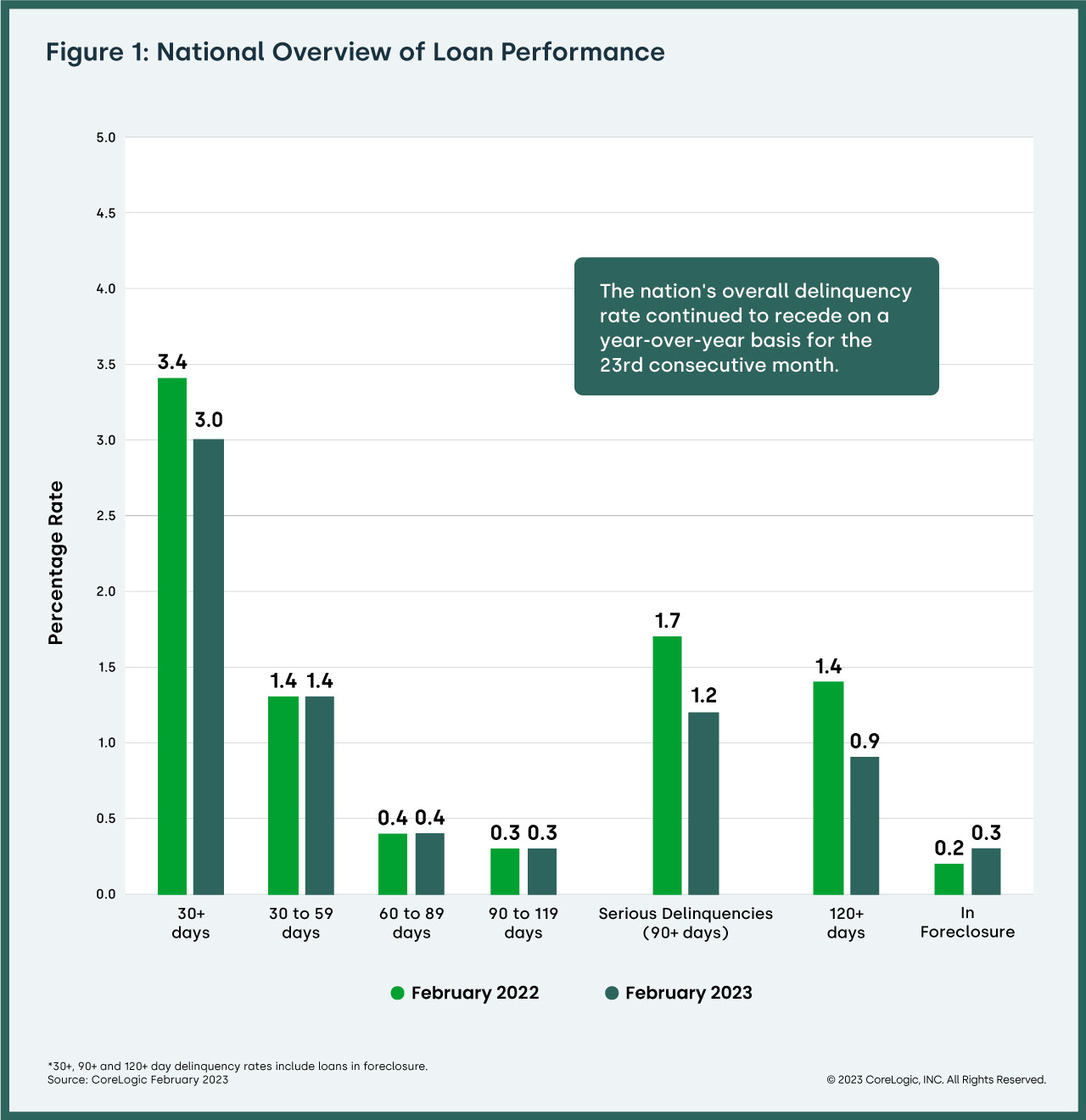

CoreLogic has released its monthly Loan Performance Insights Report for February 2023, which found that 3% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 0.4-percentage point decrease compared with 3.4% in February 2022, and a 0.2-percentage point increase compared with January 2023.

CoreLogic has released its monthly Loan Performance Insights Report for February 2023, which found that 3% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 0.4-percentage point decrease compared with 3.4% in February 2022, and a 0.2-percentage point increase compared with January 2023.

“Despite a small monthly increase in the share of mortgage payments that were one month late in February, early-stage delinquencies remained unchanged year-over-year,” said Molly Boesel, Principal Economist at CoreLogic. “February’s early-stage delinquency rate was historically low and primarily driven by a strong job market. However, the possibility of a recession that would raise the U.S. unemployment rate could slightly erode the current strong mortgage performance situation in the coming months.”

In February 2023, the U.S. delinquency and transition rates and their year-over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 4%, unchanged from February 2022 and up from 1.3% in January 2023.

- Adverse Delinquency (60 to 89 days past due): 4%, unchanged from February 2022.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 2%, down from 1.7% in February 2022 and a high of 4.3% in August 2020.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 3%, up from 0.2% in February 2022.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 7%, down from 0.8% in February 2022.

The national mortgage delinquency rate has barely changed year over year since the spring of 2022, indicating a fairly stable economy in which most borrowers are able to pay their mortgages on time. The U.S. foreclosure rate has held steady at 0.3% for a year. And while the unemployment rate remained near a pre-pandemic low in March, it is possible that mortgage delinquency rates could begin to creep up later this year, as the impact of recent job losses begin to affect the numbers several months later.

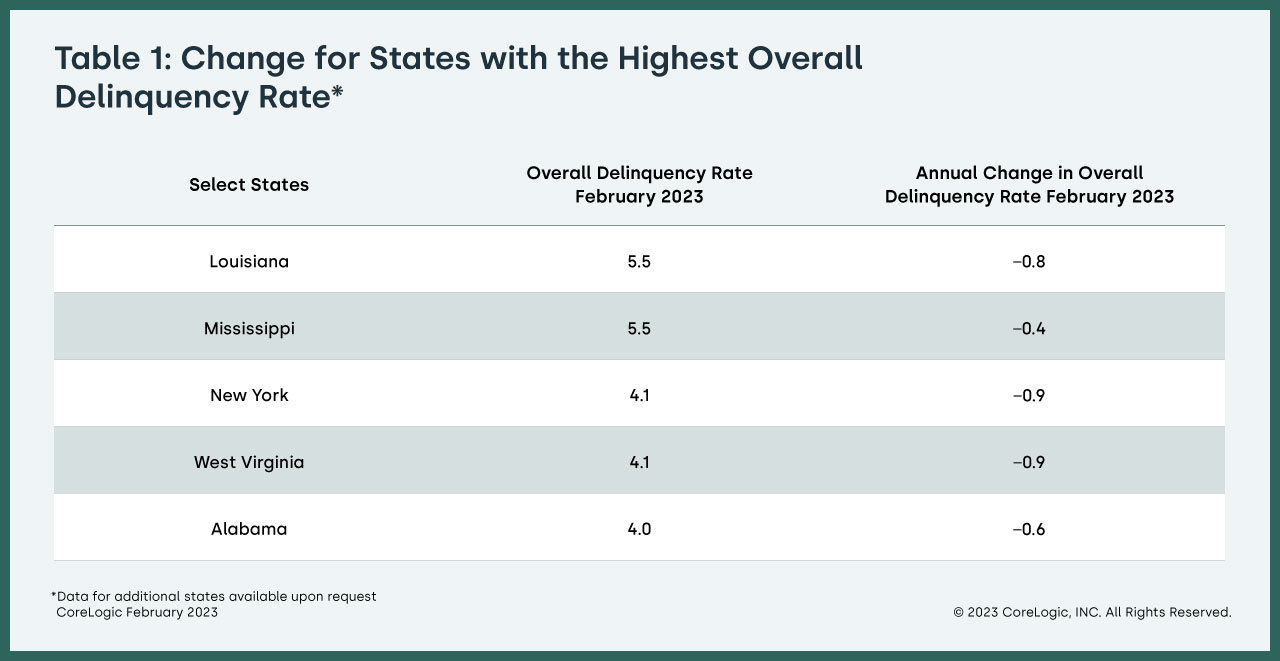

CoreLogic reported that no state posted an annual increase in overall delinquency rates in February. The states with the largest declines were New York and West Virginia (both down by 0.9-percentage points). The other states' annual delinquency rates dropped between 0.8- and 0.1-percentage points.

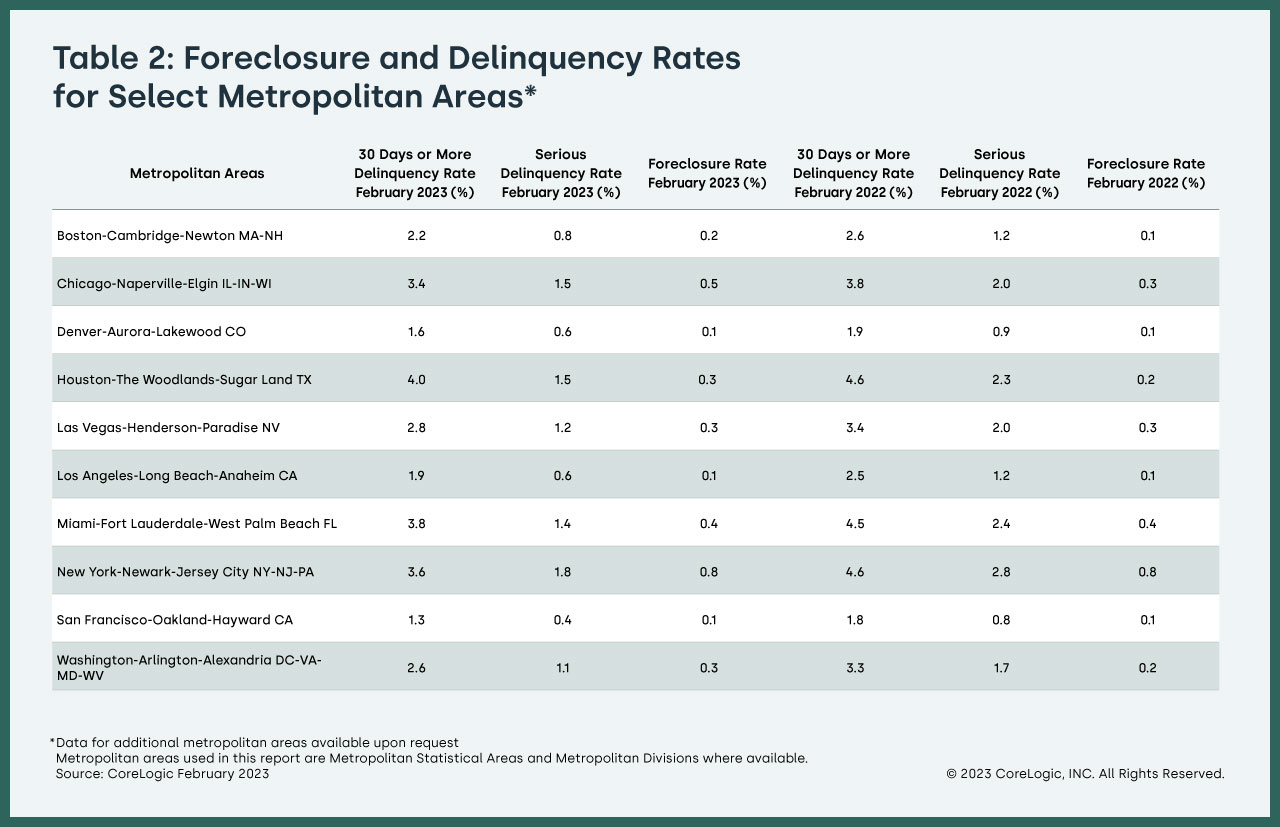

In February, 18 U.S. metro areas posted an increase in overall delinquency rates. The top two areas for mortgage delinquency gains year over year were Cape Coral-Fort Myers, Florida, and Punta Gorda, Florida (both up by 1.7-percentage points).

All but four U.S. metro areas posted at least a small annual decrease in serious delinquency rates (defined as 90 days or more late on a mortgage payment) in February. The metros that saw serious delinquencies increase were Cape Coral-Fort Myers, Florida; and Punta, Gorda, Florida (both up by 1.3-percentage points). North Port-Sarasota-Bradenton, Florida; and Bloomsburg-Berwick, Pennsylvania followed (both up by 0.1 percentage point).

Mortgage Bankers Association (MBA) VP and Deputy Chief Economist Joel Kan noted that a recession may be on the horizon according to the association.

“Continuing growth in the economy, coupled with a strong job market and inflation that is still too high–the first quarter PCE index showed 4% growth, double the Fed’s target–will likely lead the Fed to raise the Fed Funds Rate one more time at its next meeting, even as credit conditions tighten due to challenges and uncertainty in the banking sector. They are expected to then hold the funds rate at this higher level at least through the end of 2023. We forecast a short recession in the coming quarters, as these tighter financial conditions exert a drag on consumer and business activity through tighter lending conditions and higher rates. This will cause the unemployment rate to rise and gradually lower inflation closer to the Fed’s 2% target by the end of 2024.”