DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

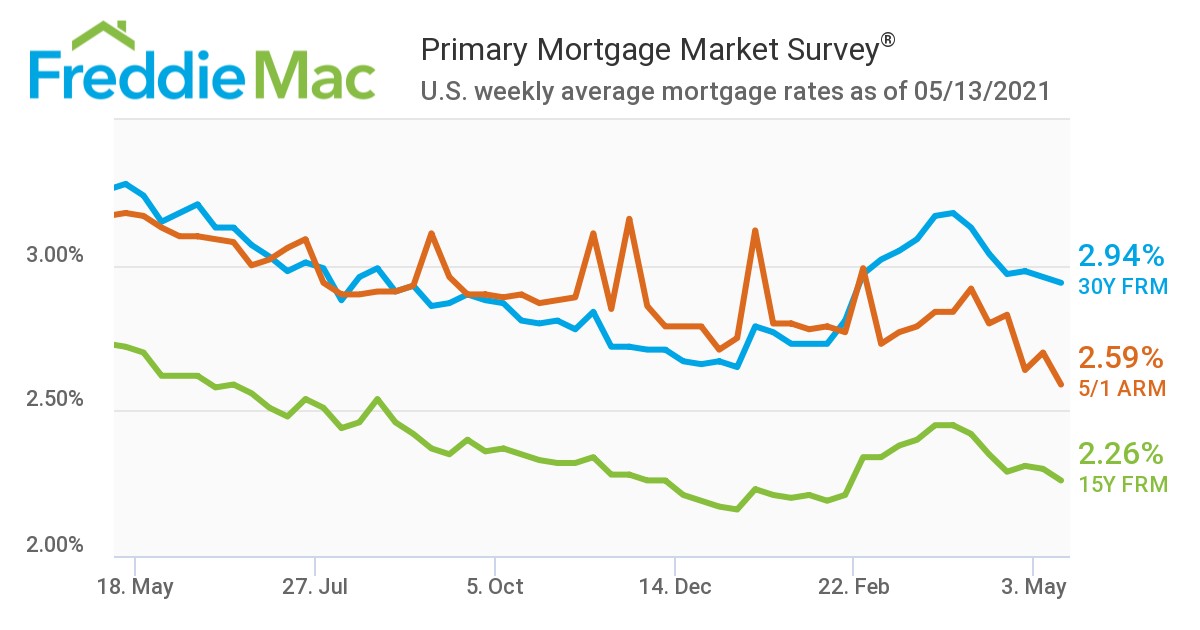

Mortgage rates continued to drop this week, as Freddie Mac’s latest Primary Mortgage Market Survey (PMMS) found rates at 2.94%, marking the fourth consecutive week of declines. Last week, rates were at the 2.96% mark, and a year ago at this time, the 30-year fixed-rate mortgage (FRM) averaged 3.28%.

Mortgage rates continued to drop this week, as Freddie Mac’s latest Primary Mortgage Market Survey (PMMS) found rates at 2.94%, marking the fourth consecutive week of declines. Last week, rates were at the 2.96% mark, and a year ago at this time, the 30-year fixed-rate mortgage (FRM) averaged 3.28%.

“Since the most recent peak in April, mortgage rates have declined nearly a quarter of a percent and have remained under 3% for the past month,” said Sam Khater, Freddie Mac’s Chief Economist. “Low rates offer homeowners an opportunity to lower their monthly payment by refinancing and our most recent research shows that many borrowers, especially Black and Hispanic borrowers, who could benefit from refinancing still aren’t pursuing the option.”

According to the Mortgage Bankers Association (MBA), the refi share of activity increased to 61.3% of total mortgage applications, up from 61% the previous week. That marked a 3% week-over-week rise in refis, but 12% lower than the same week one year ago.

Freddie Mac also reported that the 15-year FRM averaged 2.26%, with an average 0.6 point, down from last week when it averaged 2.30%. A year ago at this time, the 15-year FRM averaged 2.72%. The five-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 2.59%, with an average 0.3 point, down from last week when it averaged 2.70%. A year ago at this time, the five-year ARM averaged 3.18%.

“Additionally, the low mortgage rate environment has been a boon to the housing market, but may not last long as consumer inflation has accelerated at its fastest pace in more than 12 years and may lead to higher mortgage rates in the summer,” said Khater.

The uptick on consumer sentiment can be attributed to a dip in unemployment claims, as the U.S. Department of Labor reported that initial unemployment claims for the week dropped to 473,000, a decrease of 34,000 over last week’s level, marking the lowest level for initial claims since March 14, 2020 when it was 256,000.

“The Bureau of Labor Statistics reported that the American economy added 266,000 jobs in the month of April, and the unemployment rate was 6.1%, up marginally from 6.0% in March,” said U.S. Secretary of Labor Marty Walsh. “Labor force participation is at its highest point since last August and the number of people expressing hesitancy about returning to work due to the coronavirus is at its lowest point in the pandemic. These figures underscore how the American Rescue Plan puts us on the path to recovery. It’s increased the speed and access of vaccinations, it’s bringing needed relief to families, it’s enabling daycare centers and schools to reopen, and it’s supporting small businesses. It’s going to take time and effort to heal this economy.”