DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

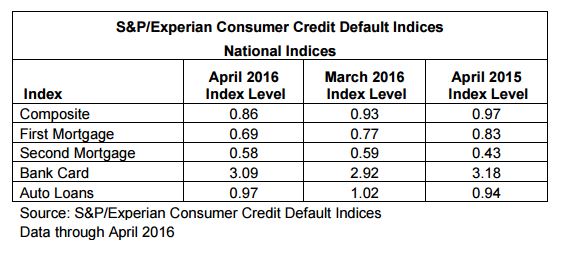

Data shows that consumers have become increasingly more careful with their debt, as the composite consumer credit default index dropped to a new post-recession low in April, according to the April 2016 S&P/Experian Consumer Credit Default Indices (SPICE Indices) released on Tuesday.

Data shows that consumers have become increasingly more careful with their debt, as the composite consumer credit default index dropped to a new post-recession low in April, according to the April 2016 S&P/Experian Consumer Credit Default Indices (SPICE Indices) released on Tuesday.

Out of the four indices that comprise the composite consumer credit default index—first mortgage, second mortgage, auto loans, and bank cards—the only one that increased over-the-month in April was bank cards. The first mortgage default rate tumbled by 8 basis points over-the-month and by 14 basis points over-the-year down to 0.69 percent.

With consumers watching their debts more closely since the beginning of the crisis, they are also spending less of their disposable income on their mortgage debt—and saving at rates higher than during the years immediately before the crisis.

“Since the financial crisis, consumers are paying more attention to their debts, particularly longer term financial commitments such as homes and autos,” said David M. Blitzer, Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices. “The Mortgage Debt Service Ratio—the percentage of disposable income going to service mortgage debt—is at its lowest point since 1980. The Total Debt Service Ratio, which includes loans with scheduled payments, is close to a record low. The savings rate is now at about 5 percent of disposable income, slightly higher than its level in 2004-2006.”

April was the second month in a row in which all indices except bank cards declined over-the-month; in March, the bank card default rate skyrocketed by 36 basis points, then leaped by another 17 basis points in April up to 3.09 percent.

April was the second month in a row in which all indices except bank cards declined over-the-month; in March, the bank card default rate skyrocketed by 36 basis points, then leaped by another 17 basis points in April up to 3.09 percent.

The second mortgage default rate ticked down by 1 basis point over-the-month from 0.59 percent down to 0.58 percent from March to April but was up by 15 basis points over-the-year in April.

“In contrast to the low default rates on mortgages and auto loans, bank cards recently showed increased default rates,” Blitzer said. “The longer term post-crisis decline in the bank card default rate leveled off in 2014. Since then, it has been in a range of 2.5 percent to 3.2 percent. Bank card, auto, and mortgage default rates are all lower than their pre-financial crisis levels. However, the bank card rate is more volatile than the others and more sensitive to consumer spending trends. Whether the default pattern for bank cards stabilizes remains to be seen.”