DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

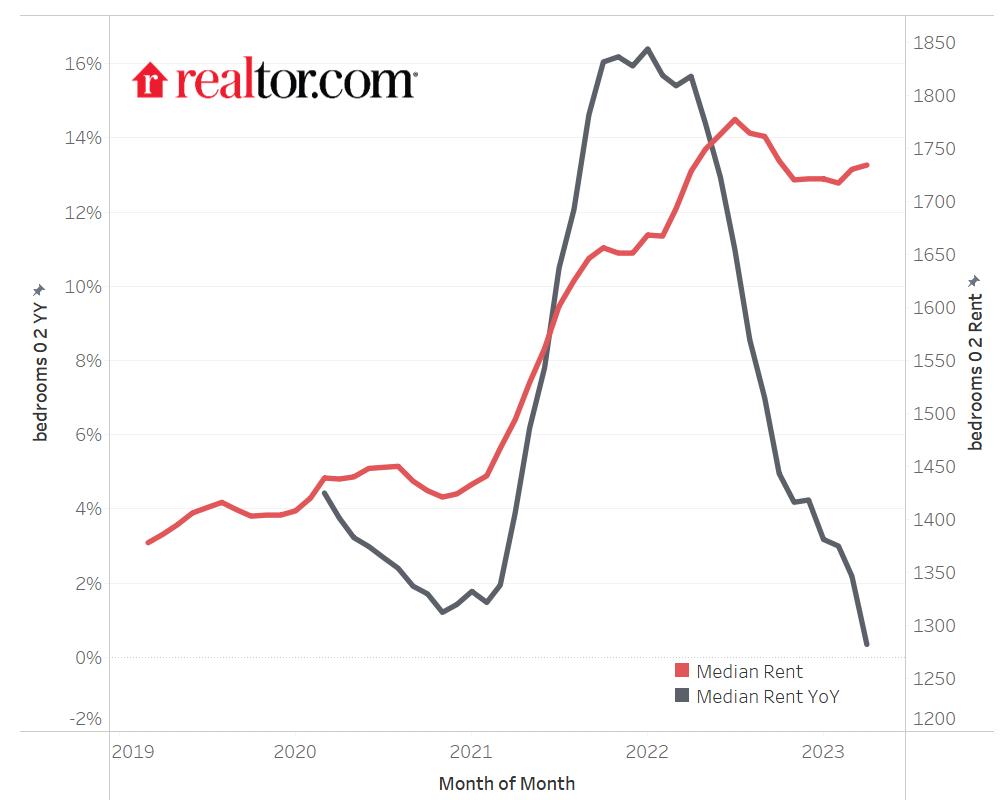

According to the Realtor.com April Rental Report, new data found that the U.S. rental market experienced single-digit growth for the ninth month in a row after 15 months of slowing. Median rent across the top 50 metros was up just 0.3% year-over-year, the lowest growth rate since the onset of the pandemic. The median asking rent was $1,734, up by $4 from last month, but down by $43 from the peak.

"In April, we continued to see rising rent prices and a moderating growth rate. This is promising news for renters, suggesting that the pandemic peaks are behind us, and that the challenging affordability picture may begin to improve," said Realtor.com Chief Economist Danielle Hale. "We've seen record-high new construction occurring in the multi-family space, which is creating more units, helping to reduce competition and in turn helping to ease prices."

Highlights

- April 2023 marks the fifteenth month of slowing rent growth, and ninth month in a row with a single-digit rate of increase for 0-2 bedroom properties (0.3% YoY), the lowest rate since onset of the pandemic.

- The median asking rent in the 50 largest metros increased to $1,734, up by $4 from last month and down $43 from last year’s peak.

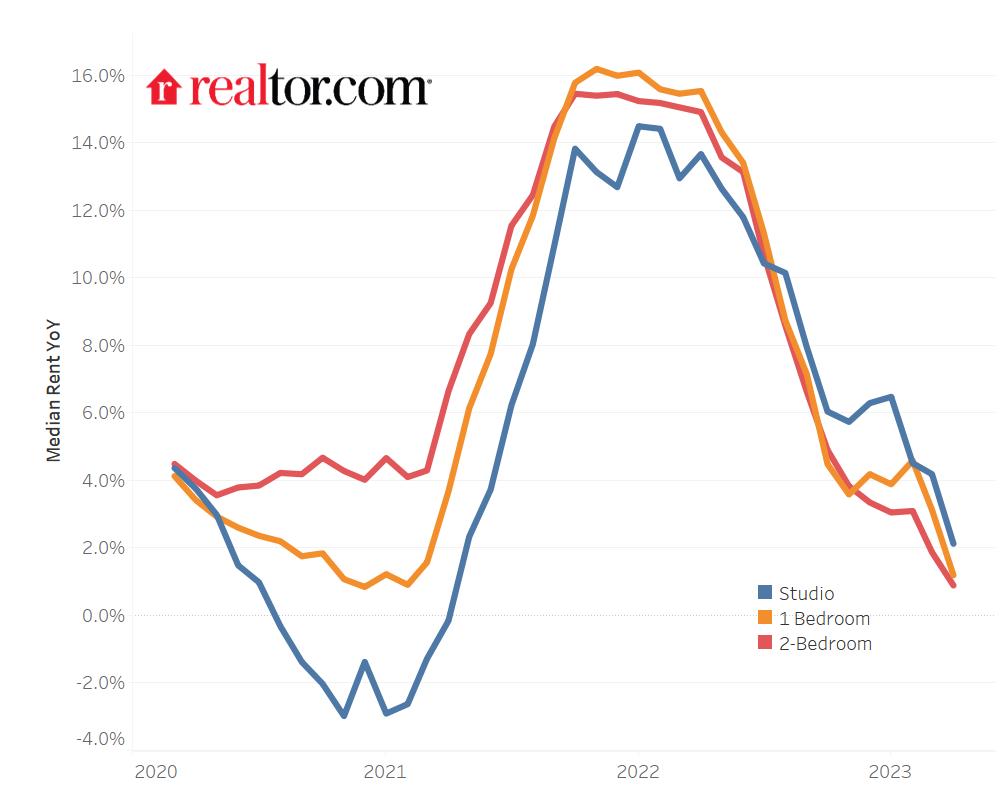

- Rent has been growing faster in smaller units. Rent by size: Studio: $1,444, up 2.1% ($30) year-over-year; 1-bed: $1,618, up 1.2% ($19) year-over-year; 2-bed: $1,936, up 0.9% ($17) year-over-year.

- Rents in the Midwest continue to increase faster (4.9% YoY), while rents in the West (-2.6% YoY) and Sunbelt market (-2.5%) were lower than a year ago.

- As rent increases were more pronounced for new renters, many existing tenants chose to avoid higher costs by renewing their leases, resulting in lower renter mobility and a stickier CPI shelter index.

Affordability improves, but prices are still high

One major factor contributing to lower rent prices is a significant increase in multi-family construction. This has helped the vacancy rate reach its highest level (6.4% in Q1 2023) in two years. As more new rental properties are added to the market, the vacancy rate could inch back toward the norms we saw in 2013-2019 (about 7.2%) and would improve affordability for renters. Despite more available rentals and slowing rent growth, average rent still costs $348 (25.1%) more than it would have at this time in 2019.

Save money by staying put

Renters who renew their lease tend to pay less than those who sign a new lease. A 2022 survey from Avail, a Realtor.com business, found that renters signing a new lease reported a price increase of nearly 27% – about double what people who have been in their rental for 1-2 years experienced (13%). To avoid paying this premium, renters are renewing leases at record-high levels, contributing to a stickier CPI Shelter Index.

"Realtor.com monthly data is based on median asking rents rather than survey responses, which are used in the CPI Index, so CPI data lags behind what we're seeing. The data suggest that easing in the cost of shelter is ahead in future CPI reports. While this could take until 2024 to play out significantly, it will be welcome news for renters and for overall inflation," said Hale.

Smaller units experience faster growth

In April 2023, the rent growth of two bedroom units increased just 0.9%, marking the slowest growth rate since the onset of the pandemic. Nevertheless, April is the fourth straight month that we saw positive rent gains in two-bedroom units on a monthly basis, a possible return to typical trends that have been absent amid the upheaval of the pandemic and subsequent recovery. The median rent for two bedrooms was $1,936 nationally, $17 (0.9%) higher than the same time last year but still $32 lower than the July 2022 peak. Even though rent for larger units had the smallest gains relative to last year, larger unit rents had the highest growth rate over the past four years, up by $430 (28.6%).

Rent growth for one-bedroom units went up and down on a year-over-year basis in recent months, sliding to 1.2% in April 2023. The median rent was $1,618, at the same level as last month but still $34 less than the July 2022 peak. Nevertheless, the median one-bedroom rent is still up by $19 (1.2%) compared to the previous year and $327 (25.3%) higher since April 2019.

In April, rent growth in studios dipped to 2.1%. As renters sought affordability, studio rents grew faster than larger 2-bedroom units over the last nine months. The median rent of studios was $1,444, down by $1 compared to last month. Nevertheless, it is up by $30 (2.1%) year-over-year and $243 (20.2%) higher than four years ago–a significant jump that is only slightly smaller than that seen in larger units.

Rents in Western Coastal Metros Cooling Faster Than Their Northeast Peers

The recent wave of job cuts in the tech industry has likely impacted the rental demand in large metros on the west coast. In April 2023, the median rent in the West was 2.6% lower than a year ago. Specifically, rents in Seattle, WA (-0.2%) saw the first year-over-year declines in nearly 2 years, and rents in San Diego, CA (-1.0%) saw the first decline in over 2.5 years. Although San Jose, CA (3.2%) appears to be an outlier in March, its growth rate was only one sixth of what it was a year ago (19%), and it is more likely to continue to trend downwards in the coming months. In contrast, rents in populous northeastern metros such as New York, NY (8.0%), Boston, MA (4.2%), and Washington D.C (4.9%) continued to experience faster growth.

The latest rental vacancy rate aligns findings in the rental trends. In the first quarter of 2023, the rental vacancy rate in Western markets remained the same as it was 12 months ago (4.6%). However, the rate in the Northeast decreased from 6.5% to 4.4% between the first quarters of 2022 and 2023, indicating a more competitive market condition in the Northeast.

Rents in Sun Belt Markets Declined

In April 2023, the median asking-rent for 0-2 bedroom rental properties across Sun Belt metros was 2.5% lower than one year ago. The top 5 metros experiencing the most significant year-over-year rent declines are all clustered in the Sun Belt regions: Riverside, CA (-10.9%), Las Vegas, NV (-5.7%), Phoenix, AZ (-5.2%), Austin, TX (-4.8%), and Tampa, FL (-4.1%).

In 2023Q1, the rental vacancy rate in the sun belt markets increased to 7.1%, 1 percentage point higher than 12 months ago and 0.7 percentage points higher than the national average, suggesting the rental market has been softening.

Rents in Midwest Markets Continue to See Faster Growth

On the flip side, rents in Midwest metros continued to see faster rent growth. In April 2023, the median rent growth rate was 4.9%. As the Midwest markets tend to have greater affordability, the stronger growth in these markets likely results from this benefit even as it may reduce existing affordability. Among the top 10 metros experiencing the fastest year-over-year growth, six of them are located in the Midwest: Cincinnati, OH (9.9%), Detroit, MI (8.9%), Columbus, OH (8.4%), Indianapolis, IN (8.1%), Milwaukee, WI (6.8%), and St. Louis, MO (5.7%).

The other four metros are New York, NY (8.0%), Pittsburgh, PA (7.1%), Oklahoma City, OK (7.0%) and Louisville/Jefferson, KY-IN (6.0%). In addition, in 2023Q1, the rental vacancy rate in the Midwest was 6.6%, 0.8 percentage points higher than 12 months ago and 0.2 percentage points higher than the national average. Specifically, the rate was increased most in Minneapolis, MN, rising from 5.3% in 2022 Q1 to 10.1% in 2023Q1.

To read the full report, including more data, charts and methodology, click here.