The House Financial Services Committee’s Subcommittee on Housing and Insurance recently held a hearing, “The Current Mortgage Market: Undermining Housing Affordability with Politics [1],” examining the pricing changes implemented by the Federal Housing Finance Agency (FHFA) and the impact they have had on the mortgage marketplace.

The House Financial Services Committee’s Subcommittee on Housing and Insurance recently held a hearing, “The Current Mortgage Market: Undermining Housing Affordability with Politics [1],” examining the pricing changes implemented by the Federal Housing Finance Agency (FHFA) and the impact they have had on the mortgage marketplace.

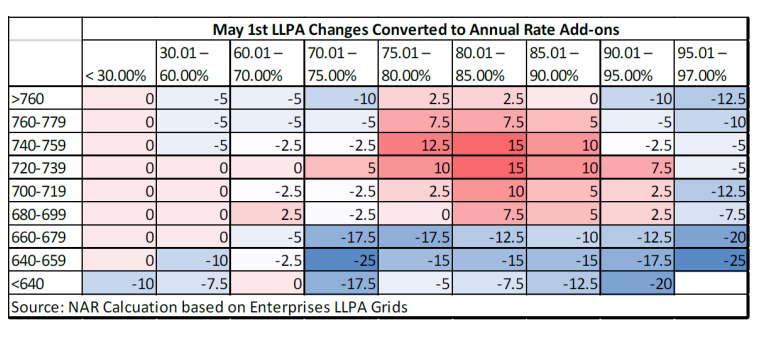

Spotlighted during the hearing were the recent changes to the loan level price adjustment (LLPA) fee structure [2] used by Fannie Mae and Freddie Mac. In general, the changes increased LLPAs for many homebuyers with better credit or who make larger down payments. They also reduced fees for many low credit score borrowers and those with lower down payments.

Industry experts providing testimony included Edward J. DeMarco [3], President of the Housing Policy Council (HPC); Kenny Parcell [4], President of the National Association of Realtors (NAR); Dr. Clifford Rossi [5], Professor-of-the-Practice and Executive-in-Residence at the Robert H. Smith School of Business, University of Maryland; and Janneke Ratcliffe [6], VP, Housing Finance Policy Center for the Urban Institute.

According to FHFA, the statutory charter for each GSE “authorizes it to impose fees and, based on that authority, each [GSE] has historically set fees for the guarantees provided for timely payment of principal and interest on securities issued.” The two G-fees currently assessed include an ongoing fee collected over the life of the loan and a one-time upfront fee when the loan is purchased, the LLPA.

“The average American homebuyer faces more barriers to achieving homeownership than ever before,” noted Parcell during his testimony [4]. “Uncertainty in the U.S. economy, rising inflation, increasing mortgage rates, and lack of affordable inventory continue to devastate buyer confidence. This year, U.S. home purchase mortgage applications dropped to a 28-year-low as rates jumped. First-time homebuyers historically made up around 40% of the market, but that has dropped to 26%, the lowest on record. The best way to build wealth is through real estate.”

LLPAs were first implemented in March 2008 as a response to the financial crisis. As financial conditions worsened in the mortgage market, the GSEs recognized their ongoing G-fees would be insufficient to cover their risks. They needed a mechanism to increase their capital and better mitigate risk as they acquired new loans. LLPAs were introduced to provide more flexibility in pricing to ensure that fees for government-backed loans matched the risk-profile of the borrower.

“The best way to produce sustainable homeownership for traditionally underserved borrowers is not reduced pricing or more lenient underwriting, both of which increase risk and the cost of losses,” said DeMarco during the hearing [3]. “Rather than ignoring the risk or accepting the risk and compensating for it by charging all borrowers more, the government would better serve these borrowers with forms of assistance that lower their risk. This support should take the form of assistance funds or subsidies that help a borrower meet the applicable underwriting standards. For example, funds could be used to create reserve accounts or to provide equity into the transaction, both of which would improve the borrower’s risk profile. Another idea would be to encourage borrowers to shorten the term of their mortgage, which would result in a faster build-up of homeowner equity.”

Unlike G-fees, LLPAs are risk-based fees, meaning they vary by the individual attributes of the loan. This risk-based pricing is essential to LLPAs. It allows the GSEs to protect their balance sheets against unforeseen risks as well as taxpayers against the ultimate costs of borrowers defaulting on their loans. LLPAs are assessed based on various factors, including credit score, loan-to-value (down payment size), loan purpose, occupancy, number of units, and mortgage type.

Risk-based pricing also allows creditworthy borrowers to benefit because, in general, the higher the risk associated with a borrower’s mortgage loan, the higher the LLPAs will be. This encourages responsible borrowing and lending.

“It is important to establish that the recent adjustments to the LLPAs do not compromise the safety and soundness of the GSEs,” said Ratcliffe while delivering her testimony [6]. “All GSE loans today are underwritten according to strict risk criteria and present low risk by historical standards. Indeed, even those falling in the lower right quadrant of the grid, with down payments less than 20% and credit score between 620 and 680, have low projected losses; we estimate less than 1%. Moreover, these loans made up less than 3% of Fannie Mae’s 30-year fixed rate, purchase, single-family owner-occupied mortgages in 2022.”

In 2021, FHFA Director Sandra L. Thompson [7] launched a comprehensive review of the GSEs’ pricing rules. As a result, FHFA announced various changes to the pricing framework, most notably was a new initiative to “recalibrate” the current LLPA pricing structure that affects the majority of GSE loans. These changes took effect on May 1, 2023, and apply to the GSEs’ single-family pricing framework for purchase, rate-term refinance, and cash out refinance loans, with a few limited exceptions.

Click here [8] for more information on the recent House Financial Services Committee Hearing, “The Current Mortgage Market: Undermining Housing Affordability with Politics.”