Repayment rates generally improved for all types of loans in the first quarter, with about five percent of outstanding debt in some form of delinquency, according to the Federal Reserve Bank of New York's Quarterly Report on Household Debt and Credit [1].

Repayment rates generally improved for all types of loans in the first quarter, with about five percent of outstanding debt in some form of delinquency, according to the Federal Reserve Bank of New York's Quarterly Report on Household Debt and Credit [1].

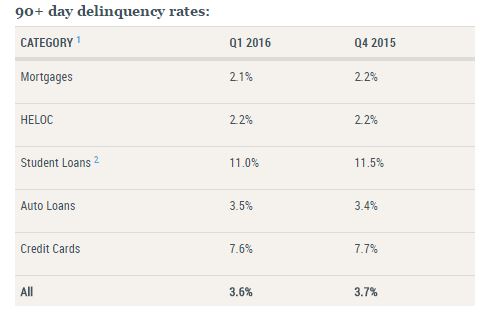

According to the New York Fed, the decline in overall delinquencies in Q1 was largely due to continuing improvement in the number of mortgage delinquencies, despite a slight uptick in the share of mortgages that were 90 days delinquent from the previous quarter (from 2.1 percent up to 2.2 percent).

“Delinquency rates and the overall quality of outstanding debt continue to improve," said Wilbert van der Klaauw, SVP at the New York Fed. "The proportion of overall debt that becomes newly delinquent has been on a steady downward trend and is at its lowest level since our series began in 1999. This improvement is in large part driven by mortgages.”

Fewer consumers filed for bankruptcy in Q1; about 207,000 consumers added a bankruptcy notation to their credit report during the quarter, which was a decline of 19 percent from the same quarter in 2015.

With the continued improvements in mortgage delinquencies came an increase in the amount of overall household debt, by $136 billion over-the-quarter and by $401 billion over-the-year up to $12.25 trillion. About two-thirds of overall debt was mortgage debt, which totaled $8.37 trillion in Q1, a four-and-a-half year high—and an increase of $120 billion over-the-quarter and $198 billion over-the-year.

A rise in median credit score of newly originated mortgages could mean that fewer of these loans will default down the road. Approximately 58 percent of all new mortgage dollars went to borrowers with credit scores of higher than 760, according to the New York Fed. According to the AEI International Center on Housing Risk, the median credit score for all individuals with a score is 713.