DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

The S&P Dow Jones Indices (S&P DJI) has released its latest S&P CoreLogic Case-Shiller Indices for March 2023—which is touted as one of the leading measures of U.S. home prices—which overall found a continuing recovery in housing prices as all of the top 20 metropolitan areas reported month-over-month price increases.

The S&P Dow Jones Indices (S&P DJI) has released its latest S&P CoreLogic Case-Shiller Indices for March 2023—which is touted as one of the leading measures of U.S. home prices—which overall found a continuing recovery in housing prices as all of the top 20 metropolitan areas reported month-over-month price increases.

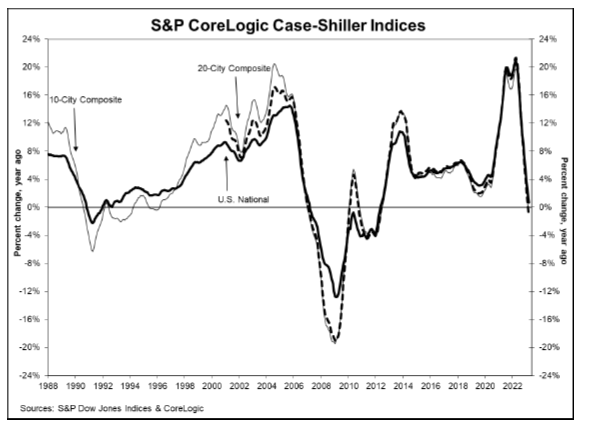

The report, now in its 27th year of publication, found that month-over-month, the National Index posted a 1.3% month-over-month increase in March 2023, while the top-10 and top-20 city composites posted an increase of 1.6% and 1.5%, respectively.

After adjusting the raw numbers seasonally, the National Index posted a month-over-month increase of 0.4% while the 10-city composite gained 0.6% and the 20-city composite posted an increase of 0.5%.

“The modest increases in home prices we saw a month ago accelerated in March 2023,” says Craig J. Lazzara, Managing Director at S&P DJI. “The National Composite rose by 1.3% in March, and now stands only 3.6% below its June 2022 peak. Our 10- and 20-City Composites performed similarly, with March gains of 1.6% and 1.5% respectively. On a trailing 12-month basis, the National Composite is only 0.7% above its level in March 2022, with the 10- and 20-City Composites modestly negative on a year-over-year basis.

“The acceleration we observed nationally was also apparent at a more granular level. Before seasonal adjustment, prices rose in all 20 cities in March (versus in 12 in February), and in all 20 price gains accelerated between February and March. Seasonally adjusted data showed 15 cities with rising prices in March (versus 11 in February), with acceleration in 14 cities.

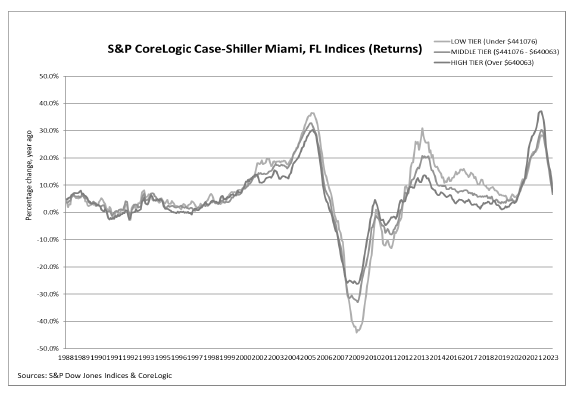

“One of the most interesting aspects of our report continues to lie in its stark regional differences. Miami’s 7.7% year-over-year gain made it the best-performing city for the eighth consecutive month. Tampa (+4.8%) continued in second place, narrowly ahead of bronze medalist Charlotte (+4.7%). The farther west we look, the weaker prices are, with Seattle (-12.4%) now leading San Francisco (-11.2%) at the bottom of the league table. It’s unsurprising that the Southeast (+5.4%) remains the country’s strongest region, while the West (-6.2%) remains the weakest.

“Two months of increasing prices do not a definitive recovery make, but March’s results suggest that the decline in home prices that began in June 2022 may have come to an end,” Lazzara concluded. “That said, the challenges posed by current mortgage rates and the continuing possibility of economic weakness are likely to remain a headwind for housing prices for at least the next several months.”

Realtor.com economic data analyst, Hannah Jones:

“Today’s S&P CoreLogic Case-Shiller Index showed a slight acceleration in national home prices relative to last year though this spring lacks its typical energy due to ongoing inventory and affordability challenges. The national index measured a 0.7% price increase compared to last March, falling from 2.1% year-over-year growth in February, though prices increased 1.3% month-over-month. The 10- and 20-city composite indices show that home prices fell between 0.8 and 1.1% on an annual basis, bucking the national trend. The index tracks prices for January, February and March. The first quarter of 2023 brought stabilizing mortgage rates, which reached a low of 6.09% in early February and a high of 6.73% in early March. Rates remained within this band for the entirety of the first quarter, enabling buyers to plan for their home purchase without having to adjust for significant mortgage rate volatility. However, even as buyers adjusted to the new normal of mortgage rates, home sellers continue to feel ‘locked-in’, hesitant to take on a new mortgage at today’s rates. As a result, many owners are choosing not to list their home for sale, creating a challenging buying environment and heightened competition in many areas."

"Mirroring trends seen in other housing and rental data, observed price increases varied considerably with the fastest growing markets–Miami (+7.7%), Tampa (+4.8%), and Charlotte (+4.7%) –seeing above-average annual growth that far outpaces the declines seen in the slowest markets–Seattle (-12.4%) and San Francisco (-11.2%). Of the 20 cities included in the 20-city composite, 19 saw annual price growth slow in March relative to the previous month.The Southeast continues to see the fastest price growth (+5.4%) while the West sees the largest declines (-6.2%)."

"The future of the housing market hinges on the outcome of current economic uncertainty as mixed signals obscure the future of the economy. Investors are keeping a close eye on debt ceiling negotiations as well as the potential outcome of the upcoming FOMC meeting, both of which have the potential to push interest rates higher. Meanwhile, though still above the target level, inflation is slowing and the unemployment rate is at its lowest level since the summer of 1969. Easing inflation, a strong job market and cooling home price growth offer some optimism to home shoppers who have been plagued with high costs over the last few years."

"The housing market is somewhat gridlocked as still-high housing costs and low inventory levels mean buyers face budget challenges as well as competition for the limited fresh listings on the market, leading to upward pressure on prices. As a result, pending home sales leveled off in April, demonstrating both constrained buyer demand and limited available home supply. However, recently stabilized mortgage rates and slowed listing price growth have granted some welcomed breathing room. Additionally, buyers have increasingly turned towards new construction to find what they are looking for when confronted with dwindling existing home supply. The housing market is likely to remain relatively tense until either home prices or mortgage rates fall enough to bring balance via both buyer and seller activity. "

Though the national housing market is far from balanced, many local markets have seen softened prices and climbing inventory, a sign that balance is on the way locally. On the other hand, many low-priced markets, such as those featured in April’s Hottest Markets, continue to see relatively high demand and price growth as buyers flock to areas that are still in the realm of possibility for homeownership.”

CoreLogic Chief Economist Selma Hepp also commented on the latest S&P DJI report:

“The CoreLogic S&P Case-Shiller Index squeezed a 0.7% year-over-year increase in March. But, monthly gains, up 1.3% from February, are almost double the increase seen between the two months and suggest housing market competition heated up again in early spring particularly in West Coast markets where most of housing slowdown occurred in second half of 2022. Strongest monthly gains were in San Francisco and San Diego. In addition, higher priced homes are once again leading the monthly gains in prices after months of relatively larger weakness following the housing slowdown,” said Hepp.