Freddie Mac on Thursday announced the sale [1] via auction of 487 deeply delinquent non-performing loans (NPLs) serviced by JPMorgan Chase from its single-family residential mortgage investment portfolio.

Freddie Mac on Thursday announced the sale [1] via auction of 487 deeply delinquent non-performing loans (NPLs) serviced by JPMorgan Chase from its single-family residential mortgage investment portfolio.

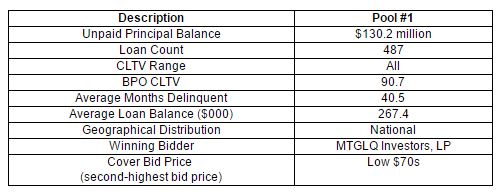

The pool of NPLs is geographically diverse and contains approximately $130 million in aggregate unpaid principal balance (UPB). The loans are about three and a half years delinquent on average, according to Freddie Mac.

Freddie Mac stated regarding the loans sold that “Given the deep delinquency status of the loans, the borrowers have likely been evaluated previously for or are already in various stages of loss mitigation, including modification or other alternatives to foreclosure, or are in foreclosure.”

The transaction is expected to settle in August 2016. Freddie Mac began marketing the transaction to potential bidders on May 11, including minority- and women-owned businesses, non-profits, neighborhood advocacy funds, and private investors, according to Freddie Mac.

Approximately 27 percent of the aggregate pool balance is comprised of loans that were modified and subsequently became delinquent; the LTV ratio of the loans in the pool is 91 percent, based on BPO, according to Freddie Mac.

A breakdown of the loan sale is included below:

Including the latest sale, Freddie Mac has sold approximately $4.3 billion worth of NPLs since the first pilot sale in 2014.

The FHFA recently announced [2] that it would bring more transparency to the NPL sales of Fannie Mae and Freddie Mac by making more data on the sales public, including information on trends such as borrower outcomes at the individual pool level. In March 2015, the FHFA announced enhanced guidelines for its NPL sales, which include applying a “waterfall of loss mitigation options” before resorting to foreclosure.

“These requirements have been in effect for about one year, and we are now in the process of evaluating the results to assess outcomes and to determine whether further adjustments should be made,” FHFA Director Mel Watt said. “Consistent with what FHFA has adopted as our standard practice, we will be transparent about these results and will provide details on any changes that result from our review.”