DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

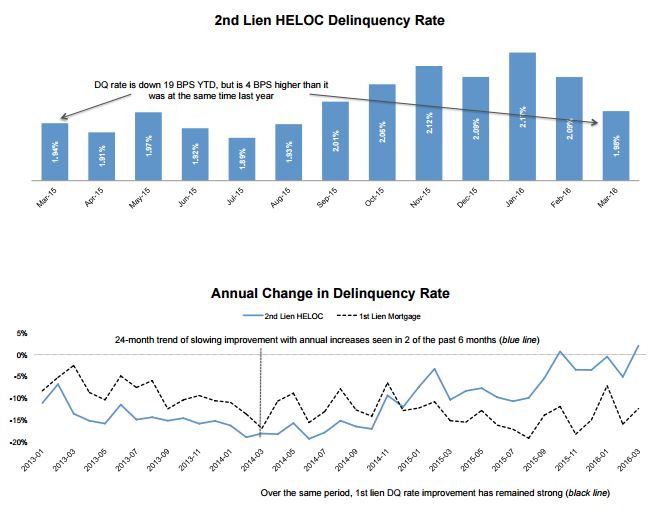

Second-lien home equity lines of credit (HELOCs) have experienced year-over-year delinquency rate increases in two of the past six months, the first such increases in nearly four years (since June 2012), according to data released by Black Knight Financial Services on Monday.

Second-lien home equity lines of credit (HELOCs) have experienced year-over-year delinquency rate increases in two of the past six months, the first such increases in nearly four years (since June 2012), according to data released by Black Knight Financial Services on Monday.

With a few million more HELOCs set to amortize over the next couple of years, there will likely be plenty of refinancing opportunities as homeowners look for a way to handle the higher payments they are facing.

According to the April 2016 Mortgage Monitor, the increases were largely driven by an 87 percent spike in the number of delinquencies among 2005-vintage HELOCs that began amortizing in 2015 at their 10-year end-of-draw period. Heading into 2015, the 2005-vintage HELOCs made up about 17 percent of all active HELOCs in the United States.

“Due to the large volumes in the 2005 vintage, those delinquencies are more noticeably impacting overall year-over-year HELOC delinquency figures, whereas up until six months ago, improved performance of other vintages had been sufficient to mask delinquency rate increases of vintages experiencing draw period expirations,” Black Knight reported.

According to Black Knight, the trend of rising delinquencies among HELOCs is likely to continue in the next couple of years, since HELOCs with a 2006 vintage—totaling about 1.25 million—began amortizing this year and accounted for 17 percent of all active HELOCS. HELOCs with a 2007 vintage currently account for about 18 percent of all active HELOCs.

The delinquency rates among 2006-vintage HELOCs already appears to be increasing, having crept up by 5 basis points over the first quarter of 2016, according to Black Knight.

There is a chance that HELOCs amortizing over the next year or two might take advantage of the low interest rate environment to refinance when they reach the expiration of their 10-year draw periods. The prepayment activity among 2006-vintage HELOCs has been higher in the last 12 months than what the 2005-vintage HELOCs have experienced, and the 2007-vintage HELOCs may similarly benefit from low interest rates, Black Knight reported.

Some 2006-vintage HELOCs may have difficulty refinancing due to larger balances and higher negative equity rates, which equate to larger payment shocks.

Over the past two years, approximately 30 percent of HELOCs reaching the end of their draw period were either paid off or refinanced. Whereas 2005-vintage HELOCs made up 17 percent of all active HELOCs at the beginning of 2015, that percentage shrank to 13 percent by the beginning of 2016.